The Congressional Budget Office released their score of the Senate’s Better Care Reconciliation Act (BCRA). It does not include the Cruz amendment. There is not a whole lot of difference since the last score as there are not many large changes on the coverage side.

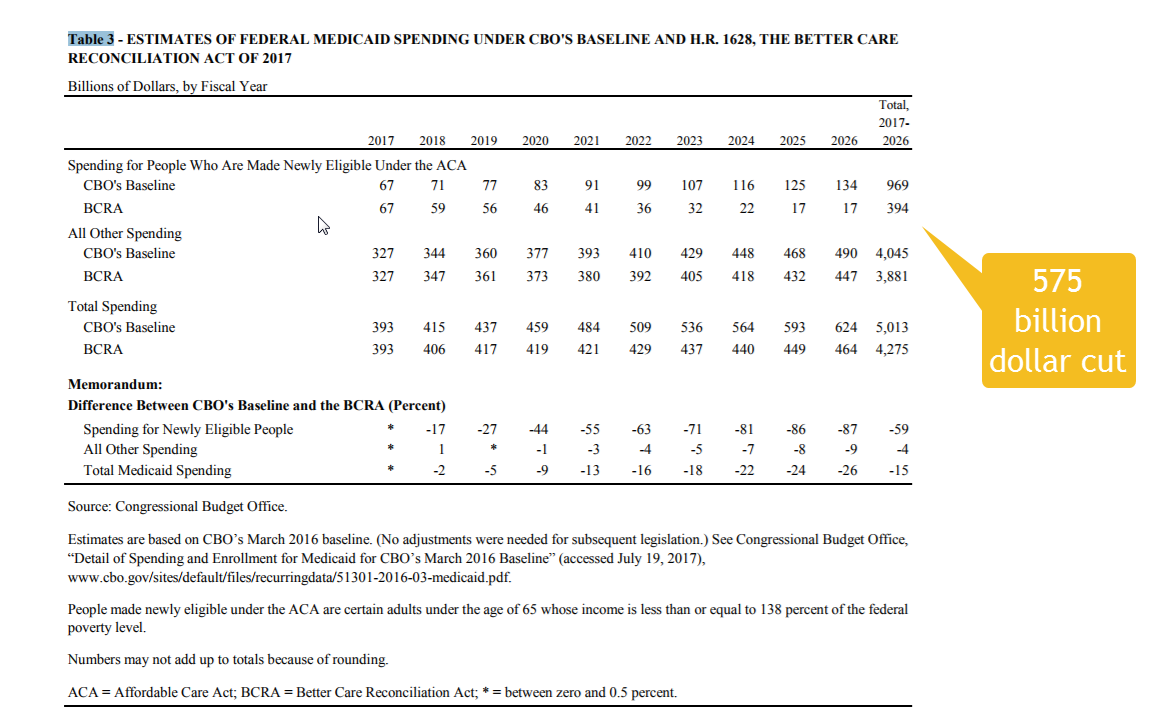

I just want to pull out a few things. The most important thing to pull out is Table 3 regarding Medicaid:

The largest savings would come from a reduction in total federal spending for Medicaid resulting both from provisions affecting health insurance coverage and from other provisions. By 2026, spending for that program would be reduced by 26 percent (see Table 3, at the end of this document).3

It is a $575 billion dollar cut to Medicaid. Throwing inadequate opioid specific money or allowing for a $200 billion dollar back door CSR funding stream won’t do anything remotely sufficient to address the people who lose coverage because of these cuts.

THe next nugget is a repetition of the basic point that the value proposition of super high deductibles is absolutely atrocious for lower income individuals:

Because this legislation would change the benchmark plan (in part, by repealing the current-law federal subsidies to reduce cost-sharing payments), the average share of the cost of medical services paid by the plan would fall—for the 40-year-old with income at 175 percent of the FPL in 2026, from 87 percent to 58 percent—and his or her

payments in the form of cost sharing would rise. And the person’s net premiums would be higher under the legislation than under current law for plans of comparable actuarial value. Those changes, CBO and JCT estimate, would contribute significantly to a decrease in the number of lower-income people with coverage through the nongroup market under this legislation, compared with the number under current law.

The baseline deductible in 2026 is a mind busting $13,000. This matters a lot for the people who are losing Medicaid. The deductibles are an absurdist joke.

a single policyholder purchasing an illustrative benchmark plan (with an actuarial value of 58 percent) in 2026, the deductible for medical and drug expenses combined would be roughly $13,000, the agencies estimate… Under this legislation, in 2026, that deductible would exceed the annual income of $11,400 for someone with income at 75 percent of the FPL. For people whose income was at 175 percent of the FPL ($26,500) and 375 percent of the FPL ($56,800), the deductible would constitute about a half and a quarter of their income, respectively.

Finally, the CBO notes a clear mechanical problem that can not be fixed without 60 votes:

The limit on out-of-pocket spending in 2026 is projected to be $10,900. (Under current regulations, the limit on out-of-pocket spending is defined by a formula based on projections of national health expenditures.) Therefore, plans with an actuarial value of 58 percent and a deductible of $13,000 would exceed that limit and would not comply with the law unless the formula used to calculate the limit was adjusted. CBO and JCT estimate that a plan with a deductible equal to the limit on out-of-pocket spending in 2026 would have an actuarial value of 62 percent. A person enrolled in such a plan would pay for all health care costs (except for preventive care) until the deductible was met and none thereafter until the end of the year.

The benchmark plan can’t be built.

Oops