Name this actor and the 1970s horror film in which he stars below:

God lord, that movie is a giant slab of Velveeta. No more hints! Open thread!

Come for the politics, stay for the snark.

Name this actor and the 1970s horror film in which he stars below:

God lord, that movie is a giant slab of Velveeta. No more hints! Open thread!

A poll, albeit a Fox News one, has the race for Alabama Senate tied. You can give to the Democrat Doug Jones below.

You know something is happening here but you don’t know what it isPost + Comments (167)

the Hanoi Hilton was nice and all but it didn't have as good an omelet chef as the Hai Phong Hyatt pic.twitter.com/E5m28dBvTI

— Kilgore Trout (@KT_So_It_Goes) October 16, 2017

.

Imagine you were an idiot, and imagine you were a Trump voter. But I repeat myself!

.

Apart from [all the facepalms], what’s on the agenda for the evening?

Tuesday Evening Open Thread: Why the Election Was Close Enough to StealPost + Comments (166)

It seems that Senators Alexander (R-TN) and Murray (D-WA) have most of an agreement together on appropriating CSR funds and tweaking elements of the ACA.

One of the tweaks is expanding access to Catastrophic plans. Catastrophic plans can not currently receive premium subsidies. I had been scratching my head on this for a couple of days as Catastrophic plans are currently sold to people under 30 or have a hardship exemption. It has a similar to Bronze actuarial value. A standard Catastrophic plan has $7,150 deductible with 3 PCP visits covered before the deductible has to be paid.

This is a risk adjustment play to lower premiums.

Rebecca Stob, a health insurance actuary who wrestles with risk adjustment every day lays out the mechanical implications:

Rates use same index rate but there is an additional discount based on the "eligibility criteria" of Catastrophic plan

— rebeccastob (@rebeccastob) October 17, 2017

Right now in the ACA there are two distinct risk adjustment pools. The catastrophic pool shifts money between catastrophic insurers. The money is mostly covering healthy and young people. The other risk adjustment pool is the Metal pool. Bronze, Silver, Gold and Platinum buyers are all shifting money amongst the plans. Typically Bronze plans will send a significant proportion of total premiums into the risk adjustment pool while Gold and Platinum plans will be net recipients of risk adjustment funds.

IF the Catastrophic concession is to open up Catastrophic plans to all ages and includes APTC subsidies while not integrating Catastrophic into the common risk adjustment pool, we get a quasi-split risk pool. Very few people will buy Bronze plans as Catastrophic will be cheaper as the Catastrophic plans won’t be sending money to the Silver-Gold-Platinum plans while Bronze plans have to cover their own medical costs plus kick money into risk adjustment outflows. Few Bronze buyers means the Silver-Gold-Platinum plans all get more expensive as they will be receiving far less risk adjustment money coming from Bronze plans.

The Catastrophic pool will still be fairly healthy as the $7,150 deductible is scary to anyone with a chronic condition but premiums will be low as the pool just needs to cover their own costs without funding risk adjustment outflows to cover sick people in Silver-Gold-Platinum.

From a distributional point of view, this is good for healthy subsidized and non-subsidized buyers, no significant change for subsidized CSR buyers, slightly worse off for subsidized Gold and Platinum buyers as the relative price spreads will increase, and bad for non-subsidized metal buyers. It might be a net improvement for non-subsidized but very high cost buyers with severe medical conditions as they were always guaranteed to hit the Out of Pocket Max in any scheme but premiums might drop enough.

Update 1 If I had to vote on this legislation, based on the reporting of the past couple of hours, and with the proviso that I actually need to see the text, I would be a yes with at most modest grumbling.

We bitch about the Beltway media a lot around here, and God knows they deserve it. But sometimes, talking heads say something worth hearing. Such was the case on AC 360 last night, when the panel was discussing Trump’s shameless, infuriating lies about how President Obama and other predecessors interacted with the families of soldiers killed in action.

In the clip below, Ryan Lizza of the New Yorker (at left in the screen grab) wonders why Trump “makes shit up” and “lies all the time.” The melon-headed butt-munch seated at right who’s failing to hide his chinlessness behind a goatee — co-panelist and former Trump flack Jason Miller — lamely tries to defend Trump’s staggering and unprecedented mendaciousness. But Lizza is having none of it, repeatedly calling Trump out for lying constantly.

Lizza is getting high-fives all over the Twitters for it, but IMO, the real hero of the clip is Tara Setmayer, who comes in at the 1:40 mark and drops the following truth bomb about why Trump is such a lying piece of shit (transcribed below the clip for those who can’t / don’t want to watch the video):

Ryan Lizza on Trump claiming Obama didn’t contact families of fallen troops: "Why does the (President) lie so much?" https://t.co/hbUaa5NcHq

— Anderson Cooper 360° (@AC360) October 17, 2017

SETMAYER: Because he’s done this his entire career and never been held accountable for it. Now he’s in front of the entire world, where he has people who will actually hold him accountable for the things he says, and he does not know how to process that, because its not in his character to do so. He’s been a liar his entire life! He’s a BS artist! And when he gets backed into a corner, then his default is to lie, make something up, deflect and divert, and when people call him on it, he says “fake news.”

Exactly right, and well said, Ms. Setmayer.

Yesterday, MAK in comments raised a very good and pragmatic implicit question; WHAT THE HELL DOES THIS MEAN TO ME AND MY FAMILY

Does this mean that the September payment covered the rest of the year? Because I’ve been looking (apparently in all the wrong places) for an answer to this simple question: when do the subsidies end?

We receive a substantial subsidy which makes our family policy affordable. If the subsidy goes away, so does our insurance. So perhaps a better question, in my case, is: when does my insurance end?

ETA: We’re in Pennsylvania, fwiw.

Everything that I have been writing about regarding CSR is happening behind the scenes. It will have future in front of the scene implications, but let’s keep things simple.

1) If you currently have an ACA plan, the CSR drama has no immediate impact on whether or not you are covered today, tomorrow or next month.

2) If you have an ACA plan with premium tax credits helping you pay the monthly premium, the CSR drama has no immediate impact on whether or not you are covered today, tomorrow or next month.

3) If you have an ACA Silver plan with premium tax credits and CSR assistance, the CSR drama has no immediate impact on whether or not you are covered today, tomorrow or next month.

So what about 2018?

1) If you qualify for premium tax credits, those will be paid normally.

2) If you qualify for CSR and choose to buy a Silver plan, you still will get the extra reductions in out of pocket expenses.

There will be strange things happening in relative pricing as we saw when we looked at Pennsylvania’s pricing this morning, but everything is going to function normally once you choose a plan for 2018.

This is a really good, pragmatic question.

Open thread for insurance questions!

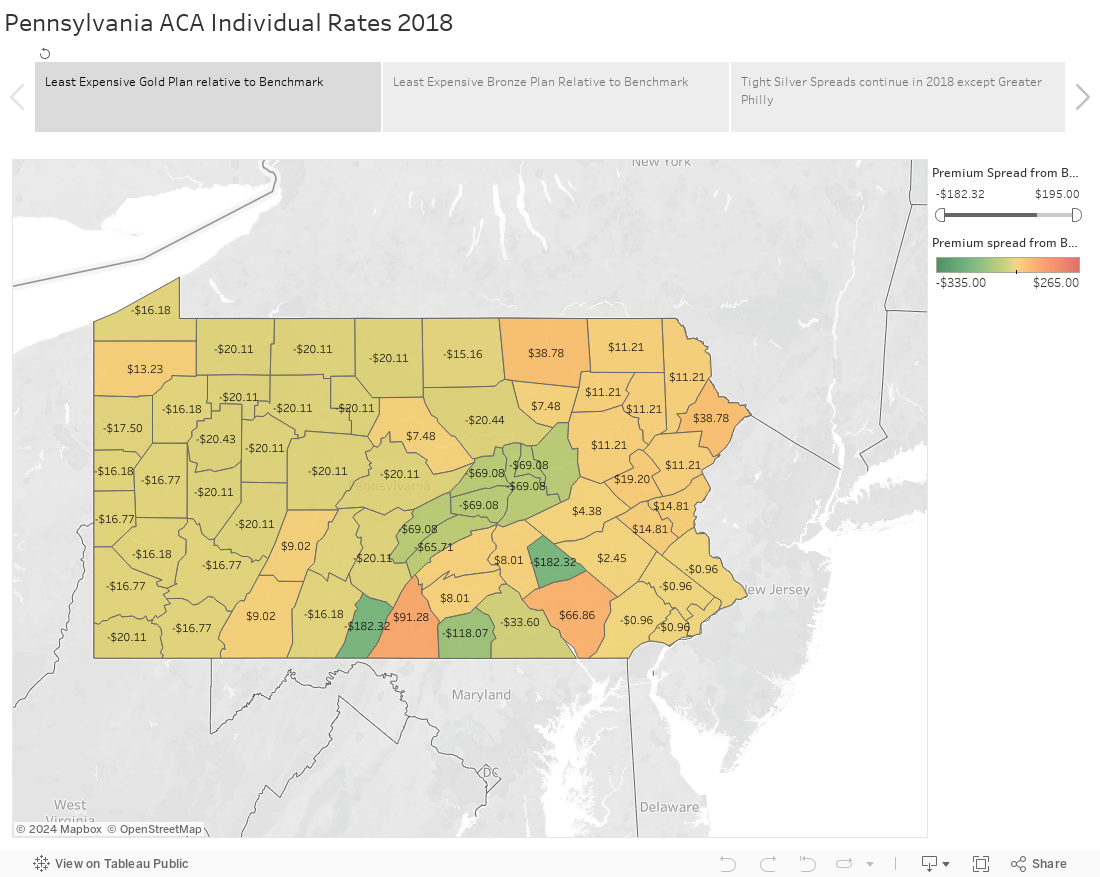

Pennsylvania released their 2018 ACA rates on Monday afternoon. Their data is here (XLSM file) and the press release is here. They are explicitly Silver Switching the entire state to accommodate the CSR cut-off.

Because cost-sharing reductions are only available on silver plans, rate increases necessitated by the non-payment of these cost-reductions will be limited to silver plans. On-exchange bronze, gold, and platinum plans and off-exchange silver plans will not be impacted by these disproportionate increases.

Premium subsidies are calculated based on the cost of silver plans in each rating area, and subsidies increase in connection with rate increases. Because rates are rising on silver plans due to cost-sharing reduction non-payment, premium subsidies may be generous enough to allow an individual who qualifies to purchase a gold-level plan that has more favorable cost-sharing at a lower price than previous years.

Acting Commissioner Altman strongly encouraged individuals who do not qualify for premium subsidies to consider off-exchange options. The department worked with each of Pennsylvania’s five marketplace health insurers to ensure they would offer an off-exchange only option that is not impacted by the disproportionate rate increases for on-exchange silver plans. Off-exchange plans must be purchased directly through one of Pennsylvania’s five marketplace insurers or through an agent or broker licensed by the department to sell on behalf of these companies.

This is a really good short explainer of how people should shop in 2018. If you make more than 400% FPL, don’t even look at the exchanges. Use a broker or go direct to the websites of the insurers in your county and buy directly from them. If you make between 200% and 400% FPL, take a very hard look at Gold plans. In most counties, there will be at least one Gold plan that is less expensive than the Benchmark Silver plan.

Below is a Tableau that has most of the details of the entire Pennsylvania insurance market. My data is here as a .txt file. I started with the state data, stripped out the small group plan-county combinations. After that, I identified the APTC eligible plans. From there, I flagged the county level benchmark. I then calculated the distance from each plan-county combination from the benchmark plan for that county. A negative number means that Plan X is cheaper than the benchmark. All premiums are based on a 21 year old non-smoker who does not receive a subsidy. As people get older and families get larger, the spreads between Plan X and the benchmark will increase by a fixed ratio.

I have a few observations below the fold.