The president and first lady serving food at a Friendsgiving at Norfolk Naval Station pic.twitter.com/SkuWWntjCU

— Sophie Hills (@sophiemhills) November 19, 2023

Some *very* happy Midwestern Thanksgiving gatherings…

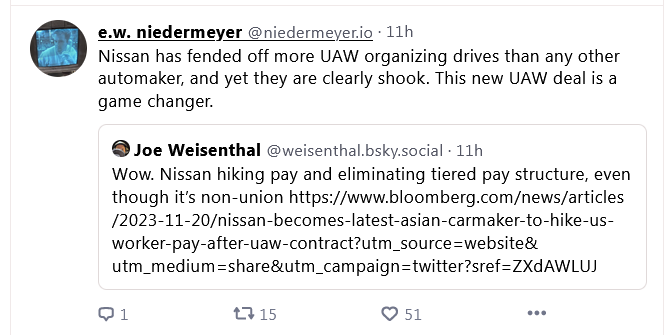

“The United Auto Workers confirmed that members at General Motors Co., Ford Motor Co. and Stellantis NV have ratified record four-and-a-half-year agreements, securing wage increases, investment commitments and more for 146,000 members”https://t.co/RYoLHvM3gD

— philip lewis (@Phil_Lewis_) November 20, 2023

Tuesday Morning Open Thread: T-Day CountdownPost + Comments (200)