Last night, Congressman Neal (D-MA) released the chairman’s draft of the House Ways and Means Committee version of the reconciliation bill for COVID. It is about 200 pages. There are less than ten pages that requires my professional attention. The meat of the health policy is on p.84 of Subtitle G.

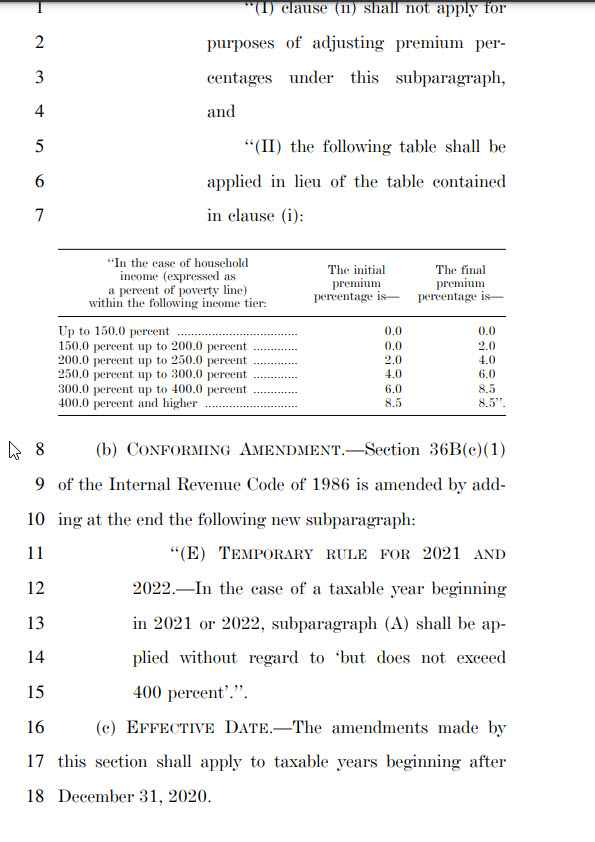

The short version of the bill is that for 2021 and 2022, almost everyone earning over 100% FPL will be eligible for an ACA subsidy and those subsidies will get notably bigger.

The long version is that this is an aggressive affordability attempt. It will make the 2022 market an almost entirely price-spread sensitive market. There are significant challenges on automatic re-newals as a lot of people could conceivably be placed in strictly dominated plans because in 2020 when they bought their 2021 plans, they purchased a lower premium but higher actuarial value plan from an insurer offering lower cost-sharing but higher premium options on the same network/plan type. They made those choices under a different subsidy system. However, it is likely that at least some higher premium plans with lower AV but on the same basic platform will now be zero premium plans. Actively aware individuals can make changes during the upcoming open-enrollment period. Not everyone is actively aware and involved. There will be people who are eligible for 87% or 94% Silver CSR plans with zero premium buying either zero premium Bronze or Gold plans in 2022. Fixing the automatic renewal process so that people are placed into plans with the highest actuarial value on the same fundamental platform of network, plan and plan type for a given premium will be an urgently needed update.

The second big question I have is if this passes in anything like its current form, what is the purpose of state subsidies like in California or 1332 reinsurance waivers for at least the 2022 plan year? Both of those are attempts to lower premiums for people who earn over 400% FPL. An 8.5% benchmark cap makes both state subsidies and 1332 reinsurance waivers irrelevant. So what happens to those funds. Thirdly, states that run a Section 1331 Basic Health Program where the state gets 95% of the federal subsidy that enrollees who earn under 200% FPL would other receive in order to provide a state funded and designed program that is effectively Medicaid Plus will see a huge cash windfall. The value of the APTC pass-through will skyrocket for two years.

There are a lot more things happening but these are things that stick out to me in this draft.