Yesterday I gave a brief overview of how Rep. Tom Price (R-GA) HR.2300 would work. The “plan” is to repeal everything related to health insurance in ACA and the reconciliation bill, and then replace it with generous tax treatment to savings, high risk pools, small subsidies by age for use on the individual market, selling …

Distributional impacts of the Price PlanPost + Comments (16)

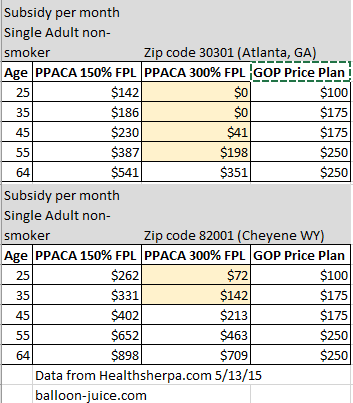

The first thing to look at is the subsidy/tax credits (they are the same damn thing) being offered by ACA and Price.

I looked at Atlanta pricing as it is near Rep. Price’s district, and it is not wildly divergent from typical experiences, as well as Cheyenne, Wyoming as that is one of the more expensive markets in the country. I used Healthsherpa.com for the premium subsidy offered to a non-smoking, single individual at different ages.  Yellow bands indicate where a person receives more money from Price than from PPACA. In Atlanta, anyone who makes under 150% FPL receives more money in PPACA advanced subsidy tax credits than they would receive from Prices’ plan. The same applies in Cheyenne. If anything this chart significantly understates the amount of subsidy people who make under 150% FPL receive as it does not include the Cost Sharing Reduction (CSR) subsidy that bumps the actuarial value of Silver plans from 70% to 94%. But even with that concession anyone who makes under 150% is most likely worse off.

Yellow bands indicate where a person receives more money from Price than from PPACA. In Atlanta, anyone who makes under 150% FPL receives more money in PPACA advanced subsidy tax credits than they would receive from Prices’ plan. The same applies in Cheyenne. If anything this chart significantly understates the amount of subsidy people who make under 150% FPL receive as it does not include the Cost Sharing Reduction (CSR) subsidy that bumps the actuarial value of Silver plans from 70% to 94%. But even with that concession anyone who makes under 150% is most likely worse off.

People who make 300% FPL are a bit more complicated. People under age 58 in Atlanta get slightly more money from Tom Price’s plan than they do under PPACA. People under age 42 in Cheyenne get more money from Price than from PPACA subsidies.

People over age 55 and in the individual insurance market are significantly better off under PPACA than they are under Price for multiple reasons. Price lifts the premium banding restrictions as PPACA is repealed. This means premiums for comparable policies for a 55 year old will be much higher for a perfectly healthy 55 year old in Price’s world than under current law. Premiums for a 64 year old who is perfectly healthy will be five to eight times more than the premiums of a perfectly healthy 21 year old instead of the three times more healthy. Note that I am specifying perfectly healthy. If a 55 year old or even more so a 64 year old has an actual medical history with pre-exisiting conditions such as getting old, insurers will either significantly upcharge them from a base rate of three, four, five times that of a 21 year to ten, twelve or fifteen times that of a perfectly healthy 21 year old or not cover them at all if they can find a way to do so. As a side note, the medical recission regulations in PPACA are repealed, so insurers will again start going through 15 years of medical records to find reasons to deny claims after the fact and cancel policies due to non-disclosure of acne as a teenager.

The subsidy plan makes people who make under 150% of poverty line universally worse off as either their subsides are much lower or Medicaid expansion is gone. Young and healthy people who are making 300% or more FPL are slightly better off. Healthy people of all ages who make more than 400% FPL are better off as they’ll qualify for an individual market tax credit in Price’s plan instead of being disqualified by income for subsidy under PPACA. Healthy people in general will see lower premiums due to the resumption of medical underwriting. Any one who is sick or has a history indicating higher future expenses (two slightly different things) will probably be worse off as their premiums will soar.

Price will argue that premiums under his plan will on net decrease and thus affordability is not a concern. Premiums will decrease because covered services will decrease for two reasons. The first is that he got rid of all Essential Health Benefit requirements in repealing the ACA. That means mental health, maternity, contraceptive and preventative screening care will be voluntary add-ons to coverage with massive adverse selection in pricing (Only women who think there is a decent chance they’ll be pregnant in the next eighteen to twenty four months will buy a maternity rider etc).

Secondly, he wants to replicate the credit card regulatory environment for health insurance. If a plan is approved in one state, it can sell in any state without the second state imposing any additional coverage burdens. That means within eighteen months of this law being passed, one small, easily bought state government will be home to 98% of the nation’s health insurers as they’ll do whatever it takes to please their new job creating overlords. Mississippi or South Dakota or Delaware will then impose their minimalist regulatory burden that won’t require coverage for autism, won’t require coverage for addiction rehab, won’t require coverage for anything expensive and politically unpopular. It will be a Gresham law situation where any insurer who does offer decent coverage will death spiral out.

These changes means that a young, male with no medical history will again see $57 a month policies for $10,000 deductibles. They’re a winner until they are either not young or have a medical history. Anyone else is probably no better off and potentially significantly worse off as they’ll either be uninsurable, their needs won’t be covered or their rates will significantly increase.

HSAs

Health Savings Accounts are a primary focus of the Price Plan as well as most other Republican health care ideas. The idea is to put people in control of their health care spending by having people covered by very high deductible, low actuarial value plans while allowing them to save money in a tax advantaged account. High deductible plans are great from a Republican point of view as long as they are proposing them but evil when Silver plans have high deductibles, but that is another post for another day. There are a couple significant HSA policy changes. Right now, a single person under age 55 can contribute up to $3,350 while someone over age 55 can contribute up to $4,350. HSAs are restricted to spending on prescribed medical care and limited non-prescription items.

Under Price’s plan, the HSA contribution limit is moved to the maximum limit to an IRS retirement account contribution limit. I am not sure if the apporiate limit is the combined IRA/Roth IRA limit of $5,500 for people under age 50, or $6,500 for people over age 50 making catch-up contributions, or the $18,000/$24,000 for Under-50/Over-50, or something else. I am not a retirement expert.

In any case, bumping up the contribution limits only helps people who are already maxing out their current contributions. That means the benefit will be overwhelmingly concentrated for people who make over 400% FPL who are looking for a tax advantaged savings vehicle. The tax advantaged nature of the HSA means a person who makes poverty level wages might see a $50 federal subsidy on their $500 HSA contribution (the odds of a person in this situation actually having an HSA is low), while someone making $500,000 a year will see a $350 federal subsidy for an marginal increase contribution of $1,000 to their HSA.

So the HSA scheme is a massive transfer of resources to the well and very well-off.

Cadillac taxes

As we all know PPACA has the Cadillac tax. It is a 40% surcharge on the incremental dollars for policies that cost more than certain thresholds. In 2018, those thresholds are $10,200 for individual coverage and $27,500 for family coverage. It is scheduled to increase at CPI-U+1 for 2019 and then CPI-U. Price’s plan modifies the Cadillac tax by reducing the thresholds but decreasing the tax rates.

Sec 131: Allows for the employer exclusion of health care coverage up to $20,000 for a family and $8,000 for an individual, with any additional funds used to be taxable dollard….

The threshold changes are important. In 2013, employer sponsored coverage for individuals averaged $5,500 and family coverage averaged $16,000. To hit the Cadillac threshold, the average plan premiums from 2013 would need to grow annually at 13% for individuals or 11.5% for family coverage. Right now we are seeing growth rates of less than 5%. Bringing the thresholds down to $8,000/$20,000 changes the growth rates needed to hit the thresholds down to 7.8% for individuals and 4.7% for family premiums. Family premium growth is roughly the sum of real growth plus inflation.

These threshold changes mean most employer provider health plans will have some portion of their premiums taxed within a few years even in a low premium growth environment. This means families with slightly above average premium plans will see their wages decrease as their health insurance will be partially taxed under Price but not under PPACA. This difference in rates will benefit individuals with very rich benefits but low cash wages. It is probably a wash to slight disadvantage for people like the Cruz family with their $40,000 a year policy from Goldman Sachs as they’ll pay a slightly lower rate (35% to 39.6% vs. 40%) on a larger increment.

(NB: From a behind the veil build a system from scratch, clawing back the employer tax exclusion for health insurance premiums is a good thing, but the transition in front of the veil is a nasty problem with significant distributional issues.

High Risk/High Cost Individuals

PPACA deals with high risk/high cost individuals by using community rating, subsidies and participation enforcement through a soft personal mandate to build big risk pools that can absorb the costs of people with consistent $30,000, $100,000, $500,000 or million dollar claim years. Price plans to deal with these people in two ways. The first is to block grant $1 billion dollars a year for four years (or $2.2 million per Congressional District per year) to help states fund high risk pools. The second is to create re-insurance pools where the states agree to pay claims above a certain level and taking the high cost tail risk off of private insurers. Re-insurance is part of PPACA as a short term bridge function. Historically state based re-insurance pools are under-funded with high premiums, long waiting lists, and limited benefits. For instance, the Tennessee high risk pool (ACCESS TN) in 2014 had a maximum annual benefit limit of $250,000 for medical expenses and $100,000 for pharmacy and a lifetime limit of $1,000,000. There are numerous conditions which can burn through either of those limits by mid-March.

The Price Plan makes people with high cost, chronic conditions far worse off as either their premiums will be far higher for far skimpier benefits, or they’ll be waitlisted for access to limit care via the high risk pool.

Wrap-up

The typical person who benefits from the Price Plan on net are families making more than $200,000 with employer sponsored insurance as they’ll see lower taxes and expanded tax shelter opportunities in the HSA. Additionally, young men with no medical history will see cheaper premiums for equivilant or worse plans. Individuals who are sick, poor, and/or female will be on net worse off. Seniors on Medicare with moderate prescription drug usage will be worse off as the donut hole re-opens.