Yesterday I gave a brief overview of how Rep. Tom Price (R-GA) HR.2300 would work. The “plan” is to repeal everything related to health insurance in ACA and the reconciliation bill, and then replace it with generous tax treatment to savings, high risk pools, small subsidies by age for use on the individual market, selling insurance across state lines and tort reform pixie dust. He funds the plan with a modified Cadillac Tax. So who wins and who loses from this proposal when compared to the baseline of current law.

Repealing all of the ACA

This is the largest source of people who will be made worse off. The big changes are the killing of Medicaid expansion, the re-opening of the donut hole, and underwriting changes.

Anyone who is newly eligible for Medicaid due to expansionwill be far worse off. At best they will transition from very affordable or free high actuarial value coverage to unaffordable junk coverage with $10,000 or more deductibles. More likely, most of these people will become uninsured as they have made the determination that food, rent, heat are more immediate needs than healthcare on a limited budget.

Senior citizens who are moderate to high prescription drug users will also be worse off. The Donut Hole in Medicare Part D is scheduled to be closed entirely by 2020, and it is significantly smaller and hitting fewer people now than it did in 2009.

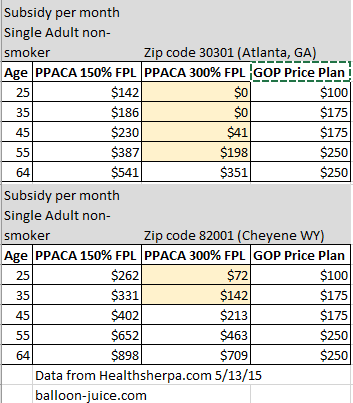

Underwriting changes are significant. The ACA/PPACA has guaranteed issue/partial community rating (age/geography/smoking bands). That means a 24 year old non-smoking woman pays the same as her 24 year old non-smoking male roommate. Premiums are banded so a 64 year old can not pay more than three times the premium of a 21 year old. Under Price’s plan, guaranteed issue and partial community rating go away. Instead, insurers are allowed to charge whatever they want and to underwrite with price discrimination. There is a minor carve-out for continuous coverage through Section 134 but if there is any coverage gaps, people will face full medical underwriting to get back into the market. Job lock will be back with a vengeance.

Repealing PPACA makes poor, women, sick, 50 to 64 year olds, Medicare beneficiaries and people not employed by larger employer groups worse off. On the other hand, young men with no pre-exisiting conditions and decent incomes are better off as they don’t have to pay for pregnancies any more. Additionally, the very well off who are paying higher taxes are better off as those taxes disappear. This is not surprising as it is why the Americans for Prosperity anti-Obamacare ads sucked last year:

There are a couple of categories of people who are undeniably worse off under Obamacare than they would have been under a no change policy. They can be clustered into a few broad groups.

- People earning over $250,000 per year in Modified Adjusted Gross Income who have employer sponsored health care or Medicare and are paying more in taxes

- Young single males with absolutely no health problems, no relatives with health problems and incomes over 250% Federal Poverty Line that previously had a $42 a month, $25,000 deductible plans that did not cover maternity or mental health needs. Those policies got cancelled and they actually have to buy good insurance. Young guys making under $25,000 a year usually will get decent subsidies, past that, it is hard to be sympathetic to someone bitching that they (a member of a high accident group) have to buy decent insurance. Avik Roy has been trying to make this class sympathetic and failing miserably)

Those are the two big classes of losers under the law. Neither are particularly sympathetic.

The New Plan

Once the ACA has been repealed, the replacement component has even more distributional implications. Subsidies, tax treatment for HSAs, Cadillac taxes and how the Price plan deals with high risk and high cost individuals are the major points I want to cover.

Distributional impacts of the Price PlanPost + Comments (16)