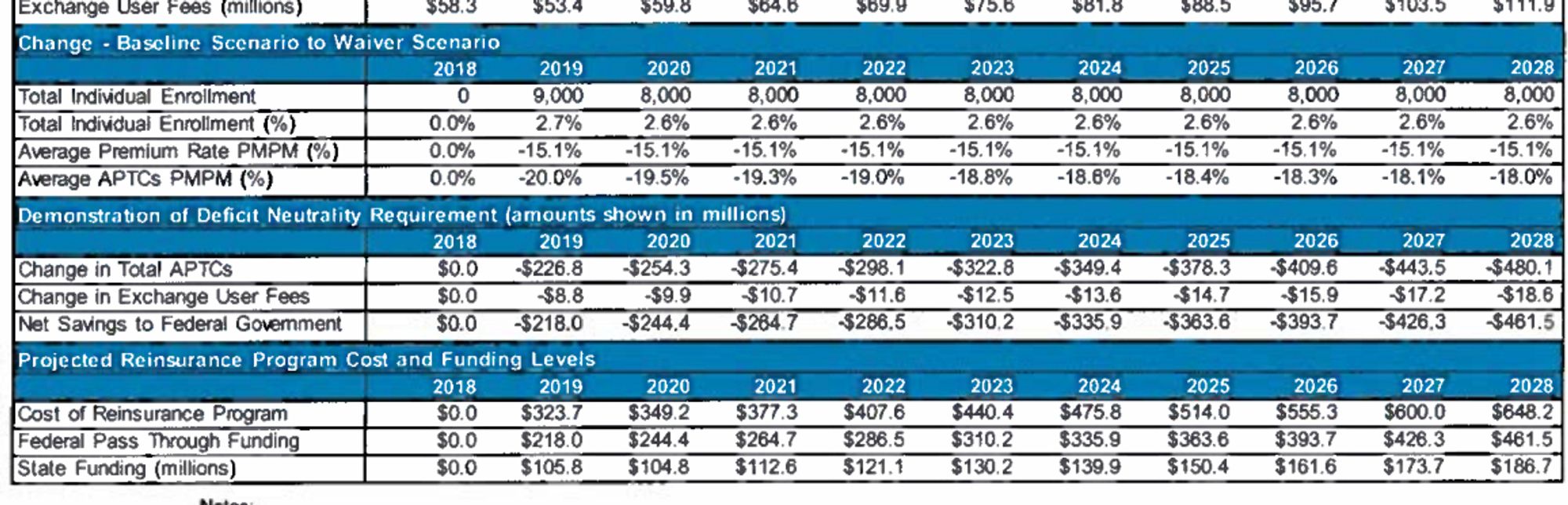

I’m just popping in as I’m waiting for the last analysis of my 2nd dissertation paper to finish running through a couple thousand bootstraps (for those who don’t know what that means, consider yourself lucky!) But there is an interesting paper in the Journal of Risk and Insurance by Handon and Minicozzi, both employees of the Congressional Budget Office. They use the full 2017-2019 risk adjustment data set to estimate the cross subsidies various demographic groups insured by the ACA give to each other — ie which groups spend on average less than their premiums and which groups, on average, spend more. Premiums in the same geography for the same plan vary by age. The authors compare individual market enrollees to small group market enrollees.

We should expect cross-subsidization. Insurance is a transfer of resources from the lucky to the unlucky. Some groups are likely to be systematically lucky or systemically a bit unlucky.

They find lots of interesting things:

Our results suggest that women aged 55–64 helped stabilize the nongroup market

through high enrollment and relatively low spending. Men enrolled in the marketplace also subsidized other nongroup enrollees but to a lesser extent than expected. In fact, men aged 25–50 enrolled in nongroup plans spent 18% more than their counterparts enrolled through a small employer.

Takeaway #1 Employment is one hell of a screen for non-chronic health conditions.

Takeaway #2 Older women are comparatively cheap — this could be the result of either better aggregate health then similar age men or less adverse selection.

Mega Takeaway MEDICARE BUY-IN PROPOSALS LIKELY RAISE ACA PREMIUMS

Medicare buy-ins would transfer a net lucky group from the ACA to Medicare. More premiums are pulled out of the ACA pool than claims. This means the surviving ACA pool would be heavy on claims and light on premiums which would drive premiums up.

Now the welfare effects are messy as the 55 to 64 year olds would have messy experiences with Medicare or Medicare Advantage stratified by geography and individual health status and income. Under 55’s who are willing to buy benchmark plans or plans priced below benchmark and who receive premium subsidies are likely to be better off as things are no more expensive and likely cheaper. Subsidized individuals who want to buy above benchmark plans (likely to be less healthy on average) are worse off, and almost all non-subsidized buyers would be worse off.

Before the ACA, research suggested that young adults (those aged 21–35) in the nongroup market would subsidize older adults (aged 60 and older) under a 3:1 age curve for premiums. By contrast, we found that in the post‐ACA nongroup market, the age‐rating curve would shift up by around 5% if enrollees aged 55 and up were excluded from the market, while in the small group it would shift down by around 0.5%.

Damn, it is almost like health policy is complicated and heavily fact dependent.