I have never really understood the argument that rate shock would collapse the Obamacare Exchanges (at least as long as the Feds can subsidize all eligible policies). The subsidies are designed to transfer the risk of premium rate increases above the rate of general economic growth to the Federal government and off of the individual. Subsidies are determined as the gap between the second lowest silver and the expected family contribution. The expected family contribution is a function of income as a percentage of Federal Poverty Line so that someone at 101% FPL is expected to contribute 2% of their income for the premium of the 2nd Silver and someone at 399.99% FPL is expected to contribute 9.5% of their income for the premium of a second Silver. If the price of the 2nd Silver doubles, the contribution stays constant. If the price of a 2nd Silver drops in half, the maximum family contribution stays constant. Subsidized buyers are insulated from price changes.

Kaiser has a good chart that I’ve snipped a part that shows this argument:\

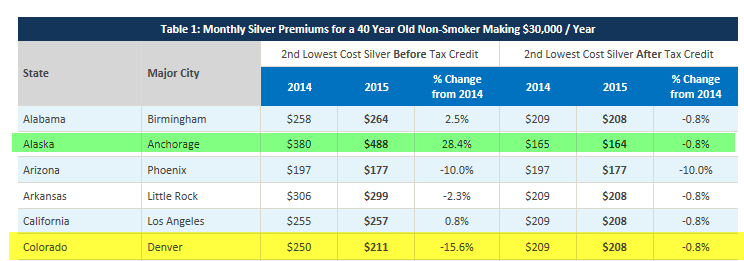

Alaska saw a 28% increase in 2nd Silver prices for 2015. The post-subsidy cost for the example decreased by a dollar. Coloardo saw a 15% decline in price for the 2nd Silver. The post-subsidy cost also declined a dollar. The dollar decline is due to inflation bumping up the poverty level brackets slightly so $30,000 in 2014 supports a slightly higher family contribution than $30,000 in 2015.

Arizona is an interesting case. In both years, the example policy holder is not getting subsidy as the 2nd Silver cost is below the maximum family contribution. In this case, the Arizonan saves $20 a month due to increaed competition if they switch policies to chase the lower premiums.

There are two major advantages to this program design. The first is that it provides predictability and security for individuals who make under 400% FPL. Their premiums will only increase as their purchasing power increases due to either more income or fewer dependents in the house. Secondly, and I think more importantly, it transfers pricing risk from atomized individuals who can’t do much about it to a big powerful entity (the Federal government) that can do something about pricing that is getting out of control. What that something is in this political climate is nothing but future political climates, a big buyer who can throw its weight around can get a good deal.