Charles Gaba passed along an interesting tidbit from the New York State ACA enrollment report:

As of January 31, 2016, 63 percent of consumers enrolled in standard QHP plans, and 37 percent enrolled in Non-standard QHPs, a decrease from last year when 39 percent enrolled in Non-standard QHPs.

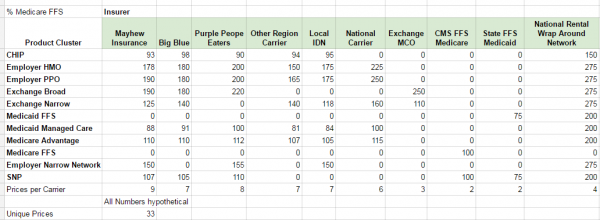

The standard plan in New York is a structure of deductibles, co-pays and co-insurance for a given metal level that every carrier has to offer.

I like this idea as it removes one area of confusion from the decision process. Healthcare.gov is encouraging carriers to offer standard benefit configurations for the next open enrollment period. That is voluntary. Carriers on both the New York exchange and Healthcare.gov can still offer non-standard plans. My preference from a public policy and consumer advocacy point of view is to only allow standard plan configurations on the Exchanges. Insurers should still offer standard benefit designs with varying networks and plan types (PPO vs. EPO vs. HMO etc) as network and plan design choices for the same actuarial level will produce very large premium swing. More importantly from a consumer point of view, those differences are truly meaningful while a Silver EPO with a $2,500 deductible and 40% co-insurance is not particularly different than a Silver EPO with a $3,000 deductible and a 35% coinsurance.

Non-standard plans allow for a lot of socially wasteful game playing by carriers. It allows for the Silver Spamming strategies to lock people out of realistic and plausible choice spaces. It drives people to have only the illusion of choice.

If the Exchanges are to work reasonably well, they must present products where people can tell why A is better than B for a given price. The metal bands are a good first step in providing a basis of comparison but the wild variety of benefit configurations with minimal differences in pricing is just cat FUD thrown against the wall to confuse the issue.