A friend of the blog passed me the Arizona approved rates for the 2017 Exchange year. They look really odd to me. Not the premiums (#’s are for 40 year single non-smoker with no subsidy), but the plan offering array seems very strange.

I really want to look at two rating areas to pull out the oddness.

The Silver Spam and Silver Gap strategies are fundamentally market segmentation plays exploiting the subsidy attachment formula. Market Segmentation is one of the first Neat Little Tricks taught in business school. Creating slightly different products at slightly different prices allows for higher allocation of transactional surplus to the produce instead of the consumer or society in general. That is why there are 12, 16 and 20 ounce soda bottles of the same brand in the grocery store.

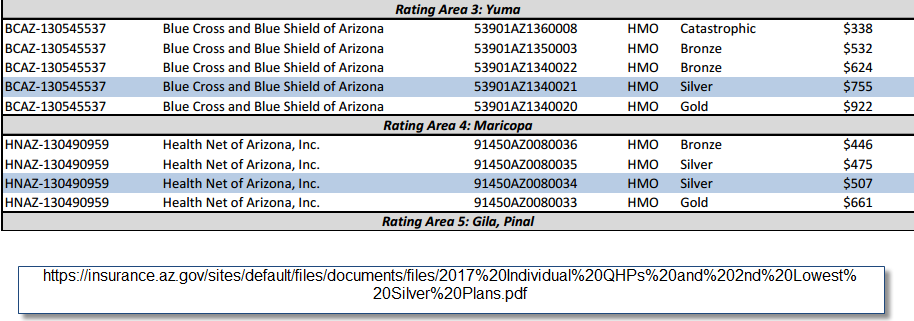

Rating Area 3 has two pieces of oddness leaping out at me. The first is the massive price differential between the catastrophic and the Bronze plans. Bronze has slightly more actuarial value than Catastrophic. The two major differentiators is that Bronze is subsidy eligible while Catastrophic is restricted to under 30 without subsidy. Additionally Catastrophic is a distinct risk adjustment pool. Getting out of the really sick risk pool and only selling to young people leads to a much healthier and cheaper product. That is interesting but not too interesting to me.

In Yuma, the intriguing thing is that Blue Cross and Blue Shield of Arizona is only offering a single Silver plan. Subsidies will be base based on that single plan.

This is really weird and I am professionally puzzled. We know that BCBS-AZ can take a plan type (HMO) and a network and build out two distinct policy offerings. They did that with their Bronze offerings in the same rating area. The big lift in building a plan offering is assembling a network and building the utilization management and plumbing for a restrictive product type like an HMO or an EPO. Adding slightly different cost-sharing components to the base of a network and plan type is dirt cheap. It requires little incremental actuarial work, it requires little incremental system plumbing, it requires little incremental provider outreach. The incremental cost of adding a new cost-sharing arrangement once you’ve done the hard work of building the base plan is low. And you can justifiably offer a tweaked plan at a slightly different price point. And that slightly different price point rejiggers the subsidy attachment point which makes the less expensive Silver plan more affordable post-subsidy. A minor tweak improves the local risk pool incrementally.

Now Maricopa County (Rating Area 4) is not as odd. Health Net of Arizona is doing a moderate Silver Gap. Their less expensive Silver will be $32 less than the second least expensive Silver. For an individual making $18,000 a year, the less expensive Silver is roughly half the post-subsidy price as the benchmark Silver.

The odd, to me, thing about the HNAZ strategy is again segmentation. They’ve shown they can tweak their benefit configuration from a common base to get distinctive price points for their Silver product. I am surprised that they are only offering a single Bronze and a single Gold plan on-Exchange. Adding a few clones would be very low cost and it would allow them to more effectively segment the market.

I don’t know why these decisions were made. They just seem odd to me.