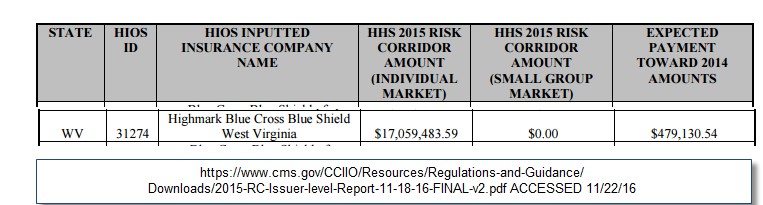

This post is a look at a weakness in the ACA. This particular weakness is mind-numbing stupidity of some carriers. The example is West Virginia and Highmark Blue Cross and Blue Shield’s strategy and results from the 2015 plan year. I am using the recently released 2015 Plan Year Risk Corridor allocations. Companies that have a positive risk corridor balance lost a lot of money on the QHP market. Carriers that are at zero balance either made or lost a little bit of money on the QHP market. Carriers paying into the pool made good money on the market.

I’m picking on Highmark in West Virginia as they are a corner case. They were the only carrier in 2015 in the state. They were the only carrier in 2014 in the state. They should have been able to make money hand over fist. Yet they lost a boatload of money.

Highmark BCBS adapted a Silver Spam strategy in West Virginia in 2014, 2015 and 2016. This means that there was a small spread between the least expensive Silver and the subsidy setting benchmark second least expensive Silver. On a practical matter that meant an individual was not getting a particularly good deal on the least expensive Silver post-subsidy. From a risk pool standpoint, a comparatively expensive lowest cost Silver and fairly high cost Bronze plans means the risk pool will be fairly old and fairly sick.

Highmark was operating as a single, monopolistic carrier for 2014 and 2015 in an environment where the federal government was willing to shovel an amazing amount of money into their hands if they configured their products correctly. A large Silver gap where the spread between the #1 and #2 Silver pricing would have produced a large APTC revenue stream and a significantly healthier, younger and cheaper risk pool was a viable play that could have been done without risking an adverse selection risk dump by other competitors. Highmark had no other competitors, they were absorbing the full risk of the state and could have effectively chosen their own risk pool. And they made decisions that led to a sick and expensive risk pool.

Stupid strategy on the part of the private sector is a weakness of the ACA as it is designed.