The Healthcare Blog has a great interview with Mark Pauly. One part made me laugh, all of it made me think long and hard through multiple states on my drive back to North Carolina. There is one part that left me scratching my head that I want to work through a bit here.

Here is the piece that has me scratching my head. Dr. Pauly is arguing that community rating is an effective but very inefficient way to make sure that high cost individuals get the effective coverage that they need.

What’s your prescription so that the high-risk aren’t financially fleeced?

MVP: If insurers are permitted to risk rate, the premiums for the healthy will fall and more healthy people will voluntarily buy insurance – let’s agree that’s a healthy outcome. The premiums for the high-risk will surely rise. My proposal– let the insurers risk rate but let us subsidize the premiums for the high-risk.

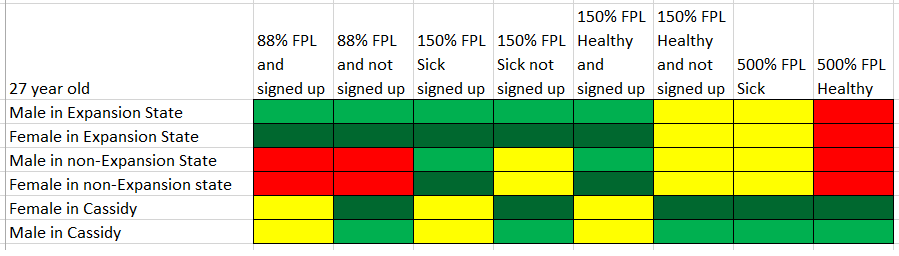

He clarifies later on that by risk, he means chronic condition risk. There are two ways this can be done. The first is to carve a set of chronic, high cost conditions out of the general risk pool and into a high cost, high risk pool. That high cost, high risk pool would then need to be financed by general taxation so that the people with chronic conditions are not decimated by only high cost people paying for each others’ care. This would be 5% to 10% of the total covered population and forty to fifty percent of the total costs. There are other high cost individuals but they are transient high cost individuals due to cats trying to assassinate them, four corner bed impalement or other one-off events. John Cole is personally a chronic risk. John Cole is statistically not a chronic risk.

That is one way to do what Dr. Pauly suggests. The other is to do a risk adjusted individual subsidy. This is where I scratch my head. It makes elegant theoretical sense but the implementation hurdles are large.