I was flipping a coin between this and the Kevin Bacon Animal House All is Well memes.

Open thread

![]()

Come for the politics, stay for the snark.

I am a student in the doctoral program at the Duke University Department of Population Health Sciences. I am working towards my my doctorate in Health Services Research with a policy focus. I am fundamentally fascinated by insurance markets, consumer choice and the navigation of complex choice environments. I'm currently RA-ing at the Duke Margolis Center for Health Policy.

I used to be Richard Mayhew, a mid-level bureaucrat at UPMC Health Plan. I started writing here and have not found a reason to stop.

Conflicts of interest: Previously employed at UPMC Health Plan until 12/31/16. I also worked full time as a research associate at the Duke University Margolis Center for Health Policy. I have received direct funding from the National Institute for Healthcare Management, and I have been on projects funded by the Rockefeller Foundation, Kate B. Reynolds Charitable Trust, Gordan and Betty Moore Foundation, Duke University Health System, CMMI, and various value based payment consortiums. I serve as a consultant on a grant from the Commonwealth Fund and have acted as a consultant to several ACA insurers.

Research Production is here: https://scholar.google.com/citations?user=zof9b4IAAAAJ&hl=en

David Anderson has been a Balloon Juice writer since 2013.

I was flipping a coin between this and the Kevin Bacon Animal House All is Well memes.

Open thread

Charles Gaba is doing his usual exceptional work of tracking rate increase requests from insurers that want to sell plans on Exchange. He recently highlighted Oregon’s initial requests. As I was reading through the actuarial summaries, the different insurers modeled sabotage risk differently. Two carriers effectively discounted it. The rest are extremely concerned. I will highlight a few key elements to show how an actuarial shows significant concern about sabotage.

First is Bridgespan. They are projecting a rate increase of 17.2%. There are two lines of interest in their summary.

The first line is they projected an 8.5% increase in medical trend. This is the cost of services. 8.5% is a bit high but not unusually so. In the alternative counterfactual universe of a Hillary Clinton presidency, 8.5% would be the vast majority of the requested rate hike. But that is not the universe we’re in. Trend makes up less than half of the increase.

The second line explains the thinking Bridgespan has in their rate increase. They think that the non-enforcement of the mandate or at least the perception that the individual mandate is gone will lead to a sicker covered population. Individuals with cancer will still sign up, individuals who are in good health and see a doctor once every couple of years won’t sign up in the same numbers.

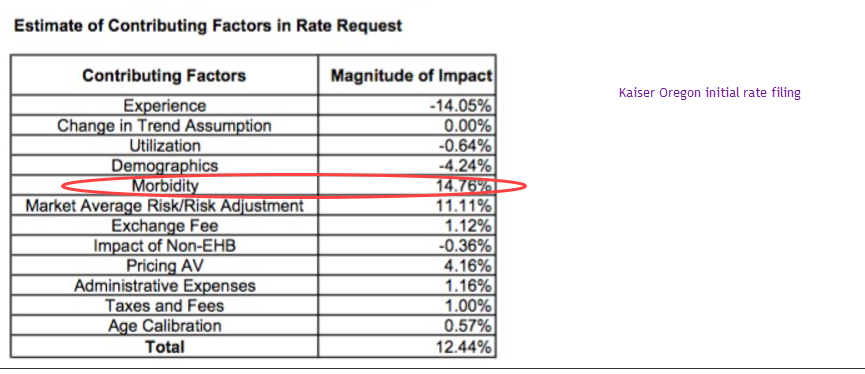

Kaiser in Oregon wants a 12.5% increase. They break down the components that drive premium changes in the following handy table:

The key assumption here is morbidity. They are assuming that their covered population will be significantly sicker in 2018 than it is in 2016 and early 2017 claims. Mechanically, the pathway is again simple. They are projecting that the perceived lack of an individual mandate will more frequently discourage relatively healthy and low cost individuals from signing up in 2018.

All of the insurers in Oregon that filed and broke out their pricing assumptions had a morbidity increase of various sizes. Everyone is expecting a sicker population on the 2018 guarantee issued, community rated plans. The typical drivers of change in rates are changes in the prices paid (trend) and morbidity. One-off adjustments such as the health insurance tax are pretty much a uniform requirement and administrative expenses. Trend is easy to prove. Regulators can ask to see provider contracts, networks and utilization patterns. Morbidity is fuzzier. Morbidity is where insurers will put their policy uncertainty risk in their rate filings.

Finally, there is a side note on optimism. Optimism on the behavioral impacts of perceived mandate non-enforcement is a big bet for actuaries to make. The most optimistic projection of low morbidity increases will lead to higher enrollment. If there is no behavioral change from the perception of a lack of mandate enforcement, the optimistic company will do very well although it would be leaving money on the table if it is too optimistic. If there is significant behavioral response to perceived or actual non-enforcement of the mandate, the most optimistic company will lose a massive amount of money as it will have attracted a significant proportion of the somewhat expensive and expensive without the counterweight of the very healthy to balance and fund their care.

Let’s avoid talking about the newest round of crazy that has been dropped on us by the Orange Gibbon and enjoy a great hockey game tonight! **

** This post written on Monday evening with no knowledge of what the cray-cray will be but high confidence that there will be said crazy.

Open Thread

BREAKING: DOJ appoints former FBI director Robert Mueller as special counsel to investigate Trump-Russia ties https://t.co/xBIBWBXc3p pic.twitter.com/KXaKPvfjsa

— HuffPost (@HuffPost) May 17, 2017

Oh yeah, the Majority Leader in the House is arguing that his statement on tape that the statement he made that the current President and a senior member of his caucus were paid by the Russians in 2016 is just a joke.

That never happened

[finds out there's audio]Take us neither literally nor seriouslyhttps://t.co/E1fq7kz79x pic.twitter.com/8XRTttZ4OB

— Adam Cancryn (@adamcancryn) May 17, 2017

Things are getting real, and they are getting weirder than ever….

Oh boy… now it is getting real and weirdPost + Comments (225)

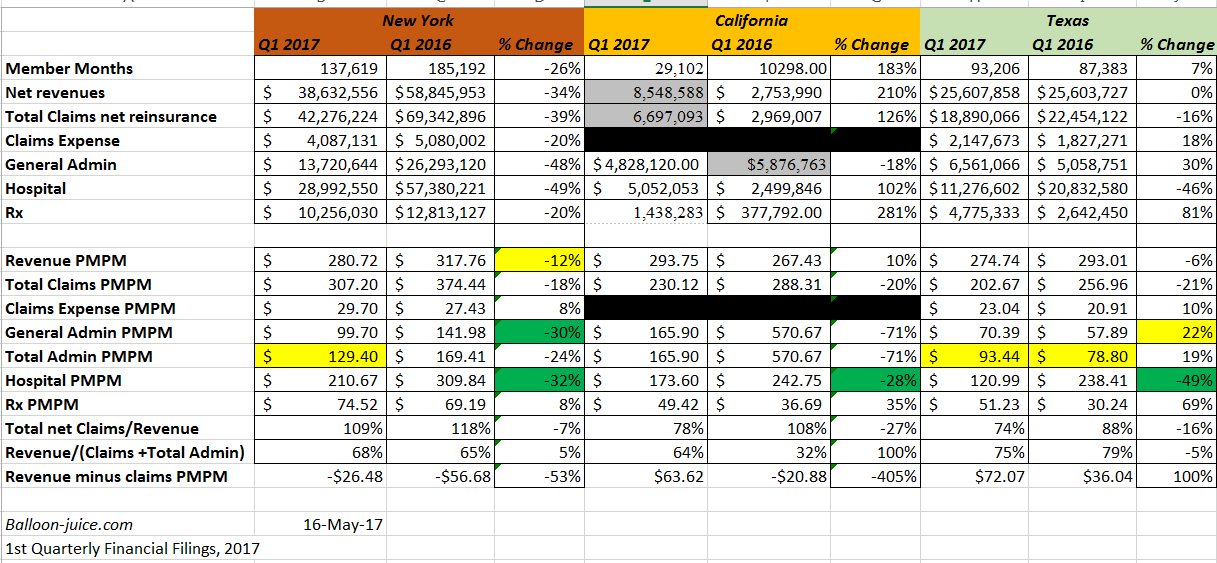

Zachary Tracer at Bloomberg recently reported on Oscar’s first quarter results. They are mixed. They are only losing $25 million dollars this quarter instead of almost $50 million dollars.

The privately held health insurer, created to sell plans under the Affordable Care Act, lost $25.8 million across three states in the first three months of this year, compared with a loss of $48.5 million a year earlier, according to regulatory filings Tuesday. The company is beginning to get a handle on its medical costs, as the premiums it collected exceeded what it spent on health services…

The company’s membership fell this year to 90,171 people as of March 31 from 106,000 across the three states a year earlier, weighing on revenue. The decision to exit markets including New Jersey and part of Texas also slowed growth. Here are the company’s results in its three states:…

Let’s look at what the financials are telling us. All are first quarter 2016 and 2017 with my own calculations.

The overall picture is still Meh. But looking deeper there are two distinct stories. Texas is a pretty good story for Oscar.

Just saw this tweet from a reporter at the Hill:

Durbin tells me it's ok for Dems to meet with Cassidy/Collins on healthcare b/c those 2 are "beyond repeal" https://t.co/F0RBQb8GvR pic.twitter.com/recMUqHDm3

— Peter Sullivan (@PeterSullivan4) May 16, 2017

When I read through Cassidy-Collins in January, my impression was that this was the contours of a deal or at least the start of a discussion on a deal:

The bill actually grapples with trade-offs. As a starting point of discussion for replace, this bill is worthwhile as it mostly focuses on further decentralizing the US health finance system to the states in the individual market and very little else. It does not do anything too controversial on non-germane subjects. It can be seen as a technical corrections bill with a conservative slant to the ACA…. A critical question will be what is the counterfactual? The counterfactual is critical in evaluating the quality of the outcomes of this bill.

It is a healthcare bill. It is a conservative healthcare bill.

Again, it is a healthcare bill. It is not a tax bill.

It is also sponsored by four Republicans which is one more than the minimally viable blocking coalition. It is a pitch to restore healthcare politics back into the realm of normal politics. That was my read on it in January and that seems to be the read Democratic Senators in seats that are not at risk in 2018 have on it now.

The most critical question on evaluating Cassidy-Collins is what is our counterfactual. Is our counterfactual a smooth and fully operational ACA? Is it a monkeywrenched ACA? Is it the AHCA minus 10% of the worst? What is the counterfactual will determine a lot of your analysis.

In other news, 9% of Americans were uninsured in 2016, down from 16% in 2010 (pre-ACA) and the lowest rate ever.https://t.co/sFOVlUi1Cc

— Larry Levitt (@larry_levitt) May 16, 2017

Open thread