From last week’s post on common problems that we all have with the health insurance system, it seems that Medicare is a major source of concern. I want to highlight a couple of questions and responses and then fill in as needed. After that, raise your new concerns in comments and we’ll figure things out as we go.

Let’s start with a common string of questions on Medicare supplemental plans using Peej01 as our jumping off point:

I’m not 65 yet, but I’m thinking that I should get a Medicare supplemental insurance plan when I go on Medicare. Can you explain the costs/benefits of those policies?

Barbara, an actual expert, replies:

For starters, go to Medicare.gov. There is a handbook that you probably already received but its on-line alternative can be easier to navigate. There is also a health plan comparison tool that allows you to plug in your exact drugs in order to personalize the comparison. It is my experience that most Medicare beneficiaries ask a threshold question of whether their doctor is in the network. For that, you might need to just ask your doctor. The comparison tool allows you to order results by premium, maximum out of pocket, etc.

MA versus Med. Supp. or some other kind of wrap around: The general perception is that if your employer is paying for an option, it usually ends up being a better deal, but you should do your homework. And no, I wouldn’t waive anything.

One thing to remember: for Medicare Supp, you are not underwritten when you are first eligible so if you think you want Supp, the best time to try it is when you are first eligible, because if you first enroll later, you will end up paying more.

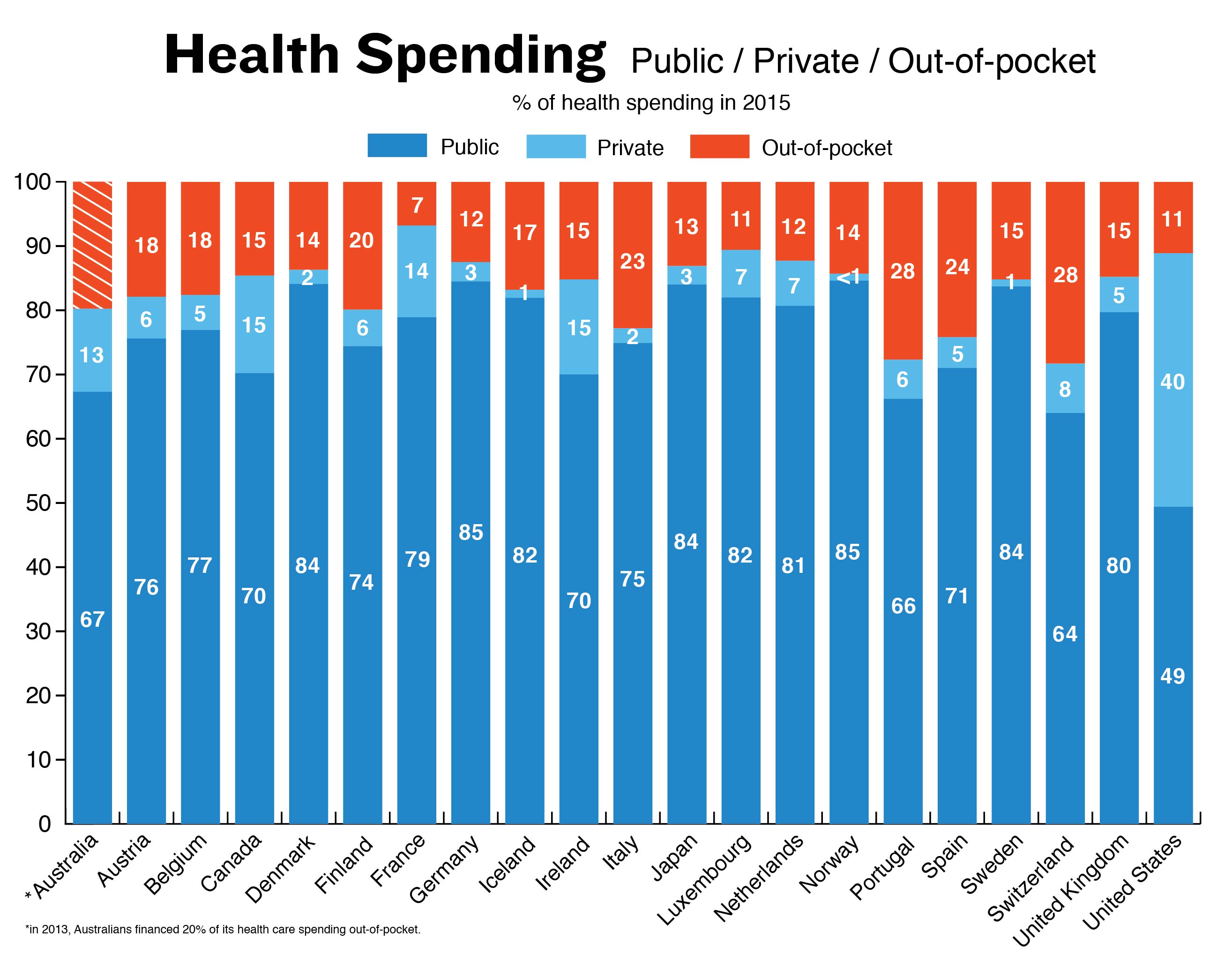

The key point is that Medicare does not cover everything.

The biggest weakness with traditional Medicare and prescription drug coverage (Part D) is that there is no out of pocket maximum. This can be dealt with in four ways. The first is to be rich enough to self-insure. That works for millionaires who can pay the 20% coinsurance out of cash. The second is to never get sick or at least die very quickly. The two most common methods are to get a Medicare Advantage plan (Part C) or a Medicare supplement.

Supplemental plans are a buy-up. They limit out of pocket expenses for people. The richest plans move Medicare from an 84% AV plan to a 99% AV plan. The least expensive plans put in a fairly reasonable out of pocket maximum and a few other benefits. At the linked guide book, you should look at page 7 and 11.

The important thing with a Medicare Supplement is that you only need it if you go the traditional Medicare route. I worked for a company that sold Medicare Advantage plans and in Pittsburgh that was a popular choice. Medicare Supplemental plans are worth considering if you think you will choose traditional Medicare.

Next from Stibbert:

Awhile back (when you were Richard), you had a friend FP about end-stage home hospice care.

Can you post a link to that thread?

Sure thing!

And if Cactus Prescott wants to write some more, I want to read and learn some more from him!

May 14, 2016 Hospice

May 21, 2016 Death the Final Frontier

End of Life Doulas

My wife had thyroid cancer (easily treated, in remission).

Part of the treatment required 2 injections which cost $1700.

Her endocrinologist office submitted the claim as medical and we would have been stuck with most of the cost.

My wife’s hospital job is in insurance so she told the endocrinologist to check the prescription benefit and we were able to get it for $100So: why does the endocrinologist, who does this all day, every day, submit for the wrong coverage, or not submit for all coverages?

The short answer is that they don’t know. I’m working on a project right now that looks at the cost differentials of infusion instead of oral treatment pathways and there are some significant cost variances. But docs in most systems don’t know. More importantly, most of the docs have historically been told that their job is to get the patient better and not to worry about how the payment stream is categorized. This is a symptom of an underlying problem.

I don’t think there is anything nefarious going on; they will get paid $1,700 from either stream, it just matters if they are getting a big check from you or a small check from you plus a big fund transfer from the insurance company. If anything, they should prefer billing the pharmacy benefit as it gets them their money faster and more reliably in most cases.

Insurance benefit design is a mess. I spent a significant chunk of my working life in insurance and I get confused as to why a certain code is cross-walked into a certain benefit category. There are good operational reasons as to why this is the case but it creates massive complexity with only one insurance company much less the dozen or more insurers a typical practice could be dealing with.

That is what I have for this week… so tell us about your problems with insurance in comments and we’ll try to solve at least a few for next week.

Bring out your problems: Medicare editionPost + Comments (32)