The American Rescue Act (ARA) significantly lowered the amount of money everyone has to pay for the benchmark plan that they purchased on Healthcare.gov for all of 2021 and all of 2022. Healthcare.gov is not automatically processing subsidy redeterminations at this time. Individuals need to go into their accounts and refresh their data to force a subsidy redetermination through. This process opened up yesterday, April 1st and will be available throughout the year. It is a forward looking process and it can be quite large.

I am a insurance agent in NC – just processed my first enrollment on https://t.co/WeCWs0xJ0n with APRA subsidy change. Small biz owner’s premium for him and his fam went from $ 1672 to $ 25.

— Christopher Smith (@042377_LedZep) April 1, 2021

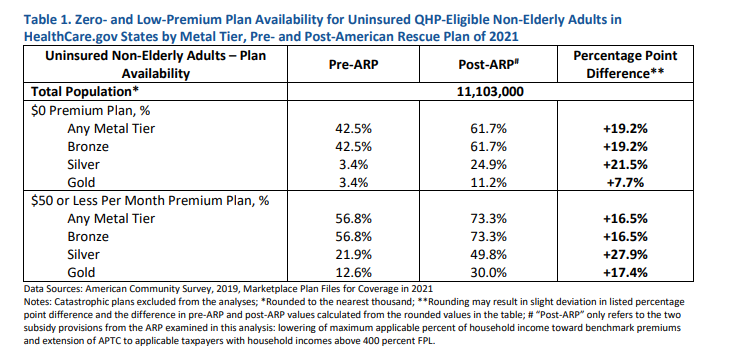

The case in the tweet is for a family of three with two people in their mid-50s who had a Bronze plan see a 98% reduction in premium. That is a bit extreme. But for people who are in their mid-50s who earned just over 400% FPL and who bought a plan priced well below the local benchmark, these types of premium reductions are plausible. For more people, the reductions are going to be smaller. However, ASPE, the Department of Health and Human Service policy and evaluation team, has projected a massive increase in the availability of zero premium plans for people who are currently uninsured.

Updating your Healthcare.gov profiles will lead to an immediately decrease in premiums for anyone who does not have a zero premium plan already. The process is currently forward looking only, so for people who bought Exchange plans that started before April 1, 2021, you should see a significant reconciliation payment on your taxes next spring to make you whole.

For people who live in states that operate their own marketplaces (California, New York, Pennsylvania, New Jersey etc) each state exchange is doing their own thing. It will never hurt to go in and update your account but don’t rely on doing that as a one time thing. You may need to monitor your premiums to see if they change.

Butch

Sorry to ask a question about something that should be obvious, but I went on the site and it’s not clear how I refresh the information needed so that I can be considered? (The policy is actually for spouse but the account is under my name.)

David Anderson

Seek out a navigator or a Certified Assistance Counselor (CAC); they will know the mechanics.

Julie

According to an email I received from the Washington state exchange, “The majority of current customers will not need to take action to receive additional tax credits and will see changes reflected in their June premiums. Customers will receive notification from Washington Healthplanfinder in April if any additional information is needed.”

WaterGirl

@Julie: I suspect there’s a lot of value, financial planning-wise, in knowing what the changes are going to be.

Brachiator

This is a big deal. I hope the message is getting out.

Also, a big deal for 2020 tax returns with Excess Advance Premium Tax Credit. Quick version:

I got this as a memo from a tax site I use. More info may be on the IRS web site.

More later.

wetzel

If anyone figures out the steps, please post these in the thread. For an old person like me, the prospect of calling a bureaucracy’s phone system for something like this is an open invitation to hypertension.

ProfDamatu

I just went on Healthcare.gov to do the update, using the Report a Change item. I actually did have to report a change to my income (it’s probably going to be about $7k higher than initially reported, assuming that all of my classes make). I’d guess that one could do the same and just enter some basically meaningless income change to trigger the recalculation.

Interestingly, when everything was recalculated, I’m only going to be saving about $30 a month compared to what I was paying before for the same plan. Given that I’m dropping down below 8% of income to premiums (from the previous 9.83%) I had assumed that the additional $7k in income wouldn’t make that much difference. But every little bit helps!