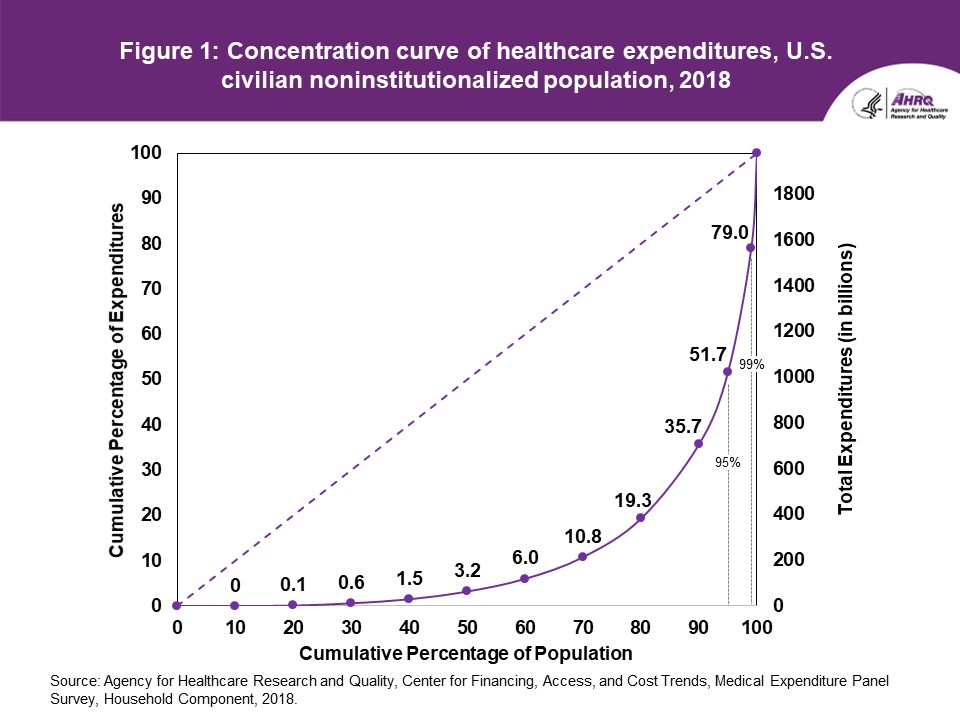

A few days ago, we highlighted the annual spending distribution among percentiles of the population. As we all know, healthcare expenditures have an extreme right hand skew:

In any given year, half the non-institutionalized population is barely touching the medical system. From a health insurance policy point of view, these folks are likely to be benefit design indifferent as either they are not using any services so no theoretical cost sharing applies, the few services that they do use are already exempted from cost-sharing (flu shots) or the plans that they are offered have high enough cost-sharing that the difference between a $500 deductible and a $5000 deductible is completely theoretical retrospectively.

Yesterday, I was chatting with my fellow nerds, and the idea of a wide variety of “copper plans” came up. In this context “copper plans” can be several different things but fundamentally, it is the introduction of a low actuarial value plan with a wicked high deductible and relatively low premiums aimed at price sensitive buyers. Colorado had proposed, in 2018, an ACA waiver to allow the state to sell Catastrophic plans that cover 3 primary care visits and nothing else until a patient hits the deductible which is the maximum allowable out of pocket expense.

Plan premiums are effectively composed of three parts. The first is administration and overhead. Some parts of A&O are relatively scale independent such as the cost of having an actuary run the modeling to price a plan and some costs are scale dependent such as the number of claims to be paid or the number of customer service reps needed. The second part is claims experience. How many and how expensive are the claims that the covered population generates. The final part is risk transfers in the form of reinsurance premiums going out and reinsurance claims coming in as well as risk adjustment transfers.

Right now, Bronze plans are almost always net risk adjustment payers. Bronze plans are wicked attractive to healthy people who are buying only on premium. In a new working paper with Coleman Drake, Sihting Cai and Dan Sacks, we show that a significant chunk of the Colorado exchange buying pool is just buying the cheapest plan available to them. Copper plans would be viable for this population that is looking for the cheapest possible hit by a meteor coverage. Bronze plans are also attractive to older individuals who know that they have massive medical expenses (2018 data for Healthcare.gov here).

If we were to introduce a Copper plan with a 50% actuarial value with deductible somewhere between $12,000-$14,000 for a single individual, we can make some assumptions about enrollment and premiums. First, this plan will be less expensive than a minimum 61% Bronze plan. Premiums will be lower. However, they won’t be 18% lower.

Right now, a significant chunk of Bronze premiums don’t pay for claims generated by people buying Bronze plans. Instead, they go out the door as risk adjustment transfers to help pay for the claims generated by people buying Silver, Gold and Platinum plans. Bronze plans cross-subsidize the premiums of people who buy higher actuarial value plans. Copper plans that are in the same risk pool would do the same.

So we’re probably looking at modest premium reductions relative to Bronze in a world where most people are subsidy eligible. We know that zero premium plans are proliferating with the expanded subsidy table of the American Rescue Act so it is very likely that zero premium copper would go further up the income scale than zero premium Bronze currently does.

For most people, in a subsidy eligible world, Copper offers dirt cheap premiums and massive exposure. Most people who would look at Copper have private information that indicates that the odds of them having medical expenses greater than $8,000 in a year (about where Bronze starts capping out) is really low. We would expect some movement out of Bronze of people who know that they have massive claims for next year into Copper as well but given the new subsidy table, this is a harder decision to make now. We would expect a massive barbell distribution of claims spending. A lot of people will have absolutely no claims and very few people will have massive claims.

From a choice perspective, anyone who is exposed to a same insurer/same network zero premium bronze or higher plan should not go to copper. This basically means these plans would be primarily aimed at folks earning well over 250% and usually over 400% FPL. I think that there is enough people who are relatively healthy and who have enough liquid assets to pay a $12,000 deductible in the case of a cancer diagnosis that there might be some interest in increasing the choice menu to allow for a lower premium but higher cost-sharing product. But again, the premium reductions will not be 1:1 for the reduction in actuarial value and the increase in risk.

germy

Butch

You really think most people who get a cancer diagnosis have a spare $12,000 lying around? Wow….

David Anderson

@Butch: No I am not assuming that —

I am assuming that a subset of people earning well over 400% FPL who are in highly probable good health will have liquid assets available to cover a massive Oh-Shit moment…. this is a small sliver of the universe but it is sliver that is currently being served by Catastrophic plans

different-church-lady

I’m holding out for a Tin plan. It will be like not having insurance but I pay for it.

Butch

@different-church-lady: They already exist. We have one. It just goes by the name Bronze plan.

Victor Matheson

So, here’s the real question in my mind about whether we want people to be able to buy high deductible plans.

What percentage of people buying these plans can really afford the out-of-pocket $15K hit in the event of an major emergency room visit or a negative diagnosis? And if most of the buyers of these products who have an adverse event can’t afford the $15K o-o-p (for many people $15K might as well be $1,000,000 in terms of their ability to pay), then it’s not really insurance and shouldn’t be sold.

rafid

@Butch:

germy

@different-church-lady:

I’m getting the wood plan.

It’s cheap because it’s based on my low income.

But I’ll have to provide proof of income every month, and send all my sensitive, private financial info over my crappy old computer, software and internet, and hope I don’t get hacked.

Or maybe I can talk to an operator!

Bill Arnold

David, for amusement only, you might want to know (if you don’t already) about the Sumerian disputations, specifically the “Debate between silver and mighty copper”. Copper wins several thousand years ago, but Silver wins in your contemporary rematch. :-)

Sumerian disputations

The debate between Silver and Copper: translation

Old School

@Victor Matheson:

My in-laws were basically offered two plans: a high-deductible plan that came with a fully-subsidized premium or a low-deductible plan with annual premiums that came to more than what the high-deductible level was.

They opted for the high-deductible plan.

Mormo

@Victor Matheson:

Indeed. Insurance & warranties are to cover, by pooling risk, losses one cannot, or would prefer not, to afford. For which service we pay, in the aggregate, a service fee (profit & overhead to the insurer). The temptation for us as customers is to purchase insurance that is (as you say) insufficient or excessive coverage, because it’s hard for us to price risk. Fortunately lifetime maxima and recission are a thing of the past under the ACA, but surveys say that some very large chunk of Americans don’t have $400 available for emergencies, which already puts Bronze deductibles and copays quite plausibly into “not proper coverage”. If our goal is to provide healthcare, continuity of care, and preventative care, in part to reduce emergency and too-late care, to say nothing of human suffering, Bronze plans are probably already too thin under many circumstances.

David, you’ve written extensively and thoughtfully about the fact of many people choosing objectively worse plans due to choice overload. Here you are pointing to thinner coverage plans, where per-member overhead would presumably be proportionally higher, and at least implying they could be suitable for certain narrow slices of the population, with careful customer choice. But we know very well that customers aren’t very good at choice, especially with choice overload & friction etc.! The ACA is pretty great but choosing exchange plans is already burdensome even in single-benefit-design California. Let’s say clearly that additional “customer choice” is bad public policy—even if it’s good in an economic model sense, people neither possess nor use perfect information.

Another Scott

Thanks for this.

tl;dr –

So the poor are subsidizing those better off. Check.

So it’s a bad choice for someone who gets a subsidy and effectively only helps the insurance companies. I think I see a solution to this problem – there should be strong minimum AVs for zero premium plans.

Make the 2nd cheapest Silver the minimum plan and subsidize it for everyone. No Bronze, no Copper, no Tin, no Chalk.

Say No to Chalk Plans!!

Thanks.

Cheers,

Scott.

Another Scott

@Victor Matheson:

TheAtlantic (from 2016):

If nearly half of people cannot easily come up with $400 (i.e. from savings), you know they cannot come up with $15,000 without major, continuing hardship.

Cheers,

Scott.

taumaturgo

We pay more than our counterparts in other democracies, and what do we get? Worse results. Eliminate the middleman extracting profits from the top.

46 million citizens can’t afford choice among the precious metal named health plans.

https://news.gallup.com/poll/342095/estimated-million-cannot-afford-needed-care.aspx