I am utterly fascinated by the ACA choice space and choice architecture. Most of my ACA related research can tie into this fascination with no more than a wink and a nod. I currently have papers in pipeline that examine plan domination, zero premium effects, market re-entry, insurer strategy, competitive responses to market entry and exit on a few axis. I have long thought that the ACA “meaningful difference” regulation makes the choice space cluttered and confusing. Insurers have three basic tools to build a unique plan. They can alter the plan type (HMO/PPO/EPO/POS) which changes the out of network benefits and the gatekeeping functions, they can change the network of contracted providers and they can change the benefits offered by manipulating

An insurer can offer a dozen near clones of a basic plan in a “silver spam” strategy as I outlined in 2016:

a Silver spam strategy that has been a hobby horse of mine for a while. The goal is to proliferate a bunch of plans tightly clustered around the subsidy benchmark point. For markets where all insurers are paying near commercial rates, this is not a big deal. In markets where one insurer is paying Medicaid plus something or Medicare like rates and everyone else is paying commercial rates to providers, this is a big deal. It forces heavily subsidized buyers to choose between half a dozen affordable plans that are functionally similar from the same insurer or not really be able to afford a choice.

This is due to the lack of good meaningful difference regulation….

Insurers can silver spam by making small changes to one of the three categories while holding everything else constant.

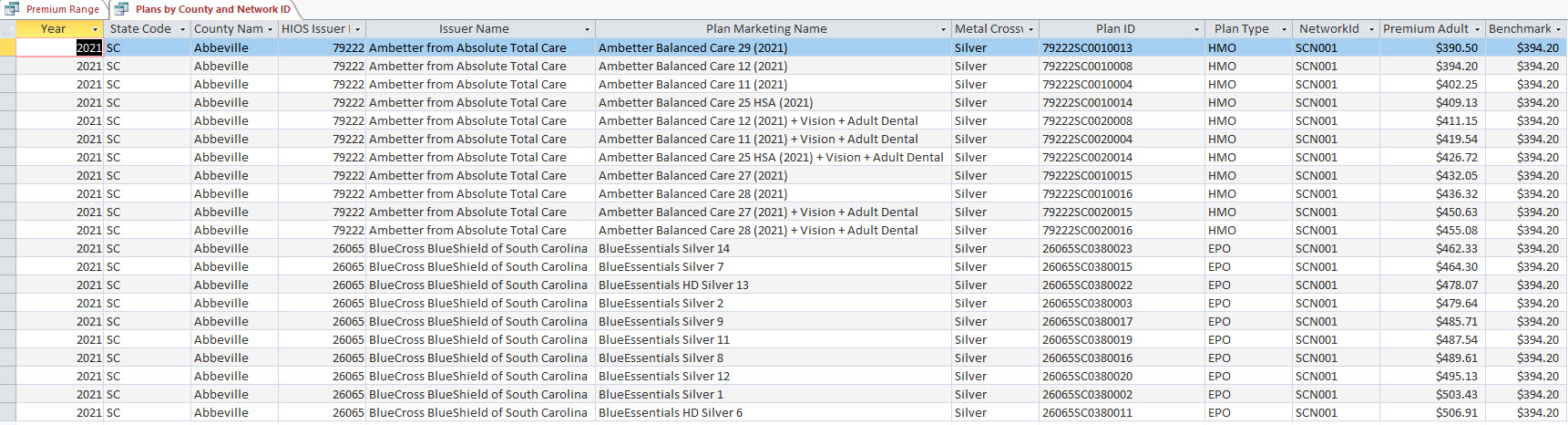

Abbeville County, South Carolina is a prime example. I used the 2021 Landscape PUF and Plan Attributes PUF to identify a county where there are multiple insurers offering at least five plans on the same network and same plan type for each insurer. A few counties in the US met this qualification. Abbeville was notable:

Two insurers, Ambetter and BCBS of South Carolina are offering a total of 21 silver plans. Ambetter offers an HMO on a single Ambetter specific network with eleven variants that have a 16% premium spread between the cheapest Ambetter plan and the most expensive Ambetter plan. An Ambetter plan is the benchmark silver plan.

Blue Cross offers 10 silver EPO plans on a single Blue specific network. BCBS-SC has a premium range of 10% between their cheapest and most expensive variant.

This is a tough choice environment. Ambetter gives some clues with the inclusion of optional adult vision and dental benefits in their plan titles, but the choice environment is challenging. The different choices are attempts to both dominate the search engine optimization of display pages for marketing purposes, own the benchmark point which means owning the CSR eligible enrollment space, and segmenting the market by risk profiles. It is also likely to make a lot of people confused and perplexed as they attempt to make a good enough choice even if they accept that they will not make an optimal choice.

Simplifying the choice space can be done by regulation. California simplifies their choice space by only allowing an insurer to offer a standard benefit package for each metal level. Healthcare.gov may not want to be that interventionist in the market. However, meaningful difference could be redefined so that any dyad of plan type and network, an insurer has to offer plans with a meaningful difference in premium of 5% or more of the minimum premium offered within a metal level. This could allow insurers to offer variants that they think are critical to offer while removing some of the surplus confusion while at the same time allowing for the possibility of wider premium spreads and greater affordability for low income silver buyers.

Barbara

Medicare Advantage and Part D imposed meaningful difference regulations to reduce consumer confusion, but Trump repealed those. It’s arguably less consequential for MA and Part D because the regulator imposes actuarial equivalence standards that are hard to game, as well as network adequacy standards that make it almost pointless to try to get by on a narrow network differentiation.

Ohio Mom

We are in the midst of making the choices traditional Medicare requires here in Ohio Family and the last phrase I would use to describe our current state of mind is “utterly fascinated.”

I don’t begrudge you, David, just jealous.

dnfree

You used the term “hobby horse”, and that gives me the opportunity to reference the book it comes from. https://en.wikipedia.org/wiki/The_Life_and_Opinions_of_Tristram_Shandy,_Gentleman

Much of the bawdy humor doesn’t still cause laughter, but the characters, especially Uncle Toby, are indelible.

David Anderson

@Ohio Mom: I was recently required to write up a connecting thread of my research agendas and fascination with the ACA individual markets was makes 75% of my publication pipeline coherent.

grandpa john

@David Anderson:Abbeville, my home town but since I am 83 insurance rates don;t really matter to me.