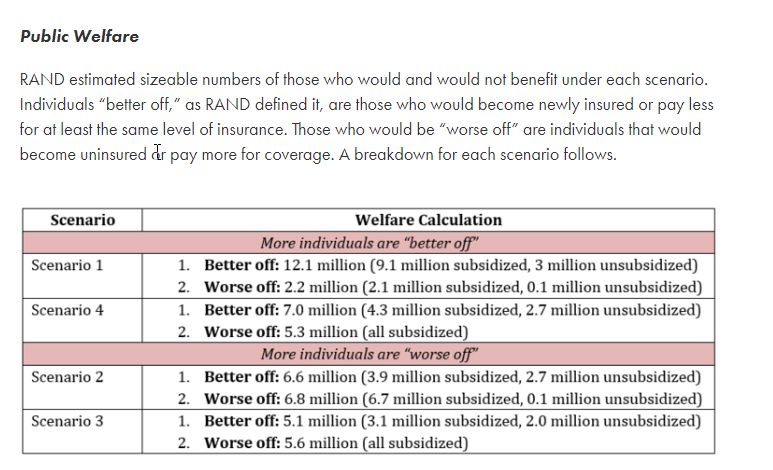

Researchers at Rand, including Jodi Liu who I’ve written with before, have a new analysis of a variety of public option plans. Two variants that increase subsidies have more people better off. Two variants that merely low index premium levels have more people worse off. The Public Option Institute has a good summary:

The public option at this time is a solution in search of several different problems. Lower price levels are good for individuals who are not receiving subsidies. Lower price levels are bad for the affordability of coverage on the ACA exchanges for people who get subsidies and purchase plans that are priced below the benchmark.

We found a strong contrast between the affordability impact of the single public option plan and multiple public option plan scenarios. Our analysis suggests that introduction of a single public option plan in each rating area of Colorado would reduce the contribution a sample subsidized consumer would need to make to the premium of the lowest-cost plan in each metallic tier by 40.0 percent to 73.4 percent. Introduction of multiple public option plans in each rating area would, by contrast, decrease net premium contributions by 6.5 percent for the lowest-cost gold plan while increasing the contribution required for bronze and silver plans by 15.7 and 0.7 percent, respectively.

The fact that Colorado’s 2019 market currently has limited spreads between the least expensive silver plan and benchmark plan contribute to this disparity of impact between the single public option and multiple public option scenarios. Currently, for a single 27-year-old, the difference in premium between the least expensive silver and the benchmark ranges from $1.00 to $18.00, with an average difference of $8.44 and a median difference of $6.00. A uniform reduction of 20 percent in premium would shrink the absolute difference in premiums between the less expensive plan and the benchmark if two or more public option plans were to be introduced. Lower spreads yield higher net premiums for subsidized buyers who purchase plans priced below the benchmark, which is what we have modeled here. These findings are consistent with the work of Coleman Drake and Jean Abraham who have demonstrated how insurer competition in the market reduces premiums but also compresses silver premium spreads, which reduces the value of the APTC as premiums converge over time.

Emma Sandoe and I wrote that policy makers need to understand their objectives in regards to proposals for Medicaid buy-in. I think that same warning applies to public option proposals as well”

The policy should be judged based on how the programs serve the policy maker’s intended goals. Medicaid buy-in proposals can achieve multiple goals. Each advocate may lay out their goals of this policy differently, but whether the details of their plan meet their stated goals can be determined using the criteria outlined in this post…

Medicaid buy-in proposals still need significant development to become a viable policy. At this stage, proposals should outline their intended objectives and clearly articulate the policy choices aimed at addressing these goals….

The critical questions for a public option program at this time is what problem is it trying to solve, and how does it interact with the ACA price linked subsidy formula as it attempts to solve the stated problem. The RAND analysis shows that there are significant trade-offs with meaningful distributional impacts.

Uncle Cosmo

Nothing like a wonky David Anderson health policy thread to bring commenting on BJ to a screeching halt. /grouch

I do have one substantive comment, though: IMO that 2×2 table up top is waaaaaay too coarse-grained to facilitate any sort of reasonable analysis. What’s “better off/worse off”? Cheaper/pricier? By how much? What’s the distribution of savings/cost by (say) disposable income?

The question is, how much “better off/worse off” do people need to be before it’s noticeable? Which sorts of people? And what is the weighted gain/pain? And (unfortunately) how many “very much worse off” outliers could the anti-health-insurance types dig up & splash across their pet media as examples of the horror of soshulized medsin?

(Maybe – probably – this is addressed in your paper, David, but I’m really of no mind to go digging around in the weeds to flush it out. I’m only saying that IMO what you present, to the level you present it here, is not all that informative for policy considerations.)

negative 1

I admit I’m WAAAYYYY too dumb to understand this, so maybe someone can help me out. Keeping the public option ‘off of the exchange’ helps the most because the ‘advanced premium tax credit’ decreases if the premium price goes down.

Why is this a problem? I get RAND’s analysis, like they have to analyze an idea placed into existing conditions. But why couldn’t you just increase the amount of the subsidy until at the very least people are held harmless? Or, put another way, lets say plan B was $1,000 and you were subsidized $400. In comes Public Option at $700. This decreases the subsidy to $350. Now, I understand that you are stuck — you still can’t afford Public Option at $700, but your subsidized coverage is still net $650 vs. $600. Why can’t you just run the subsidy as if the public option doesn’t exist, so that the net still remains at $600? Or, why isn’t the Public Option capable of being subsidized? I am not saying ‘gee I’m so smart look I solved it’ I genuinely don’t understand what it is I don’t understand.

David Anderson

@Uncle Cosmo: Truth — and it felt damn good to write a non-COVID thing this morning.

RAND analyzed 4 scenarios. 2 of the scenarios they had any differential in benchmark levels and thus premium tax credits funnelled back to beneficiaries in the form of higher subsidies. RAND defined Better off as being able to afford the same or higher AV coverage for the same or lower premium. Worse Off is defined as paying a higher premium for the same or worse coverage.

And I agree a 2×2 table is reductive but useful in first level communication. I’m acknowledging that I’ve become an academic as I get way too excited about the tables in Appendix B rather than the actual paper.

There was a sensitivity analysis of a paper in 2019 that had a null result that I am trying to figure out how to get 2 or 3 years worth of funding to really run down in exhaustive detail.

ronno2018

I have a news alert for Washington State Cascade Care which is under development. I really would like to hear from the staff attempting to develop it. If we can get a Biden presidency and control of the Senate, they need to coordinate with whatever adjustments to ACA happen at the federal level.

Yutsano

@ronno2018: I was curious, so I did some research. I found this PDF with some interesting information. Maybe our long lost Mr. Mayhew can pour over it when he gets an opportunity.