UPDATE 4/14/20 I am making significant updates in Italics to clarify timing

Individuals who are losing their employer sponsored insurance and qualify for ACA subsidies through a Special Enrollment Period have always had a decent chance of qualifying for a zero premium plan if their incomes are low enough, families big enough and everyone is old enough. However there is also a chance that many individuals who lost their insurance could get a negative premium plan. People could get paid to buy ACA plans but they would not see the check until the Fall of 2021.

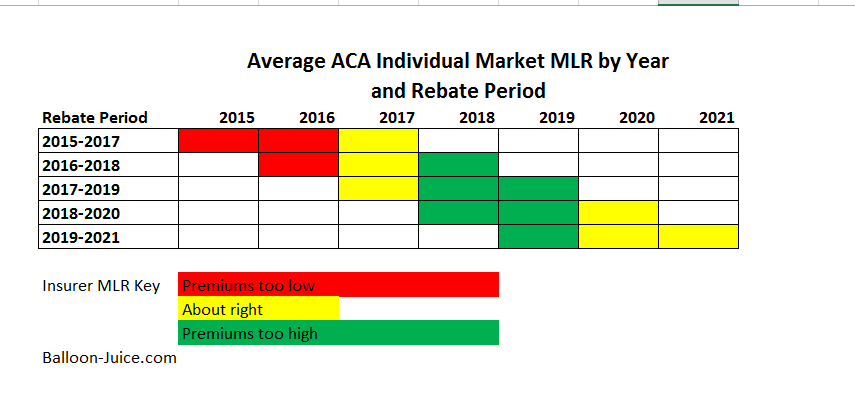

The Medical Loss Ratio (MLR) requirement is that insurers must spend at least 80% of qualified premiums on claims. If they don’t do this over a three year rolling period, the insurer has to pay back the increment between what the actually paid out in claims and the minimum allowable pay-out. Rebate checks for the preceding three years are calculated in the summer of the following year with rebates going out the door in September. We looked at this last September 2019.

The 2016-2018 MLR period has one year where premiums were significantly below claims and running costs in 2016, a year where the insurers priced things about right in 2017 and a year where insurers significantly overpriced in 2018. Depending on the insurer, the underpricing in 2016 could reasonably cancel out the overpricing in 2018. The 2017-2019 MLR period has one year priced right and two years overpriced. This will produce larger MLR rebates in Fall 2020. The 2018-2020 MLR rebate period also has two overpriced years and one year that may be priced about right.

Rebate checks are issued to policy holders of the pay-out last calcuation year. The size of the check is a the proportion of gross premiums that their policy is worth for the current year times the overall rebate pool. An individual who qualifies and buys a $10 a month net premium Bronze plan with a $500 month premium gets the same MLR rebate as an unsubsidized individual buying that same policy for $500 per month net. Given these mechanics, it is quite plausible for subsidized buyers who purchased low or no net premium plans to actually purchase negative premium plans by the end of the rebate cycle. This most likely happened in 2019.

A little birdie told me recently that the entire Medical Loss Ratio (MLR) rebate that will be paid out in September 2020 for the 2017 to 2019 plan years will be massive and likely to be almost an order of magnitude greater than it was in 2019. Many people will be in the position to be effectively paid to have purchased insurance in 2020 2019. Individuals who are currently buying insurance through a SEP have the ability to be slightly more strategic and purchase low net premium plans that can likely be negative premium plans once MLR rebates are processed in the summer of 2021 for the 2018-2019-2020 rebate period.

WaterGirl

Good news, I’ll take it! Finally something where low income people don’t get the short end of the stick.

WereBear

President Obama is still working for us. I’m sure Joe Biden is committed to it as well.

Just Chuck

Ah healthcare, where actually providing the service people pay for is called “loss”