The Civitas Institute of North Carolina is arguing against Medicaid expansion. They contend that Medicaid expansion will throw thousands of people off of their current zero premium plans that they can buy on the Exchange.

The expansion population is composed of working age, able-bodied adults, 78 percent of whom have no dependent children. Working full time at minimum wage, these individuals would be eligible for fully-subsidized, no-cost-to-them plans on the federal exchange….

Expansion will force approximately 146,000 North Carolinians off of their private plans and move them onto the state’s Medicaid rolls. It will also disqualify an additional 120,000 uninsured people from the fully-subsidized plans for which they are currently eligible, but of which they are not taking advantage.

Zero premium plans are common. However, they are incredibly different in the benefit structure and financial exposure borne by someone who earns between 100% to 138% FPL to compared to Medicaid Expansion.

Zero premium plans happen when a plan is priced below the silver benchmark and the relative premium spread is bigger than the individual’s expected personal contribution. For the 100-138% cohort, the personal contribution for a single individual ranges from $22/month to about $55 per month for the benchmark silver plan. The benchmark plan is a silver plan with 94% AV CSR benefits. That translates into a deductible ranging from zero to a few hundred dollars and an out of pocket max of less than $2,000. Compared to a baseline silver, this is a great improvement in the quality of the benefit. It is still significantly worse than Medicaid if we assume appointments can be found.

However, silver plans are not guaranteed to be zero premium. There could be a “tight spread” between the cheapest silver plan in a county and the benchmark which often happens if the region is a competetitive region with strategically adept insurers or if there is a monopoly and the monopolist for some reason or another only offers a single silver plan as both the benchmark and the cheapest silver. Instead, the vast majority of time, the zero premium plan are bronze plans. In Orange County, North Carolina, the bronze plans all have deductibles over $6,000. If someone is earning 138% FPL, that is over a third of their annual income before the insurer actually starts paying for catastrophic expenses. Bronze plans, in this scenario, are hit by a meteor protection.

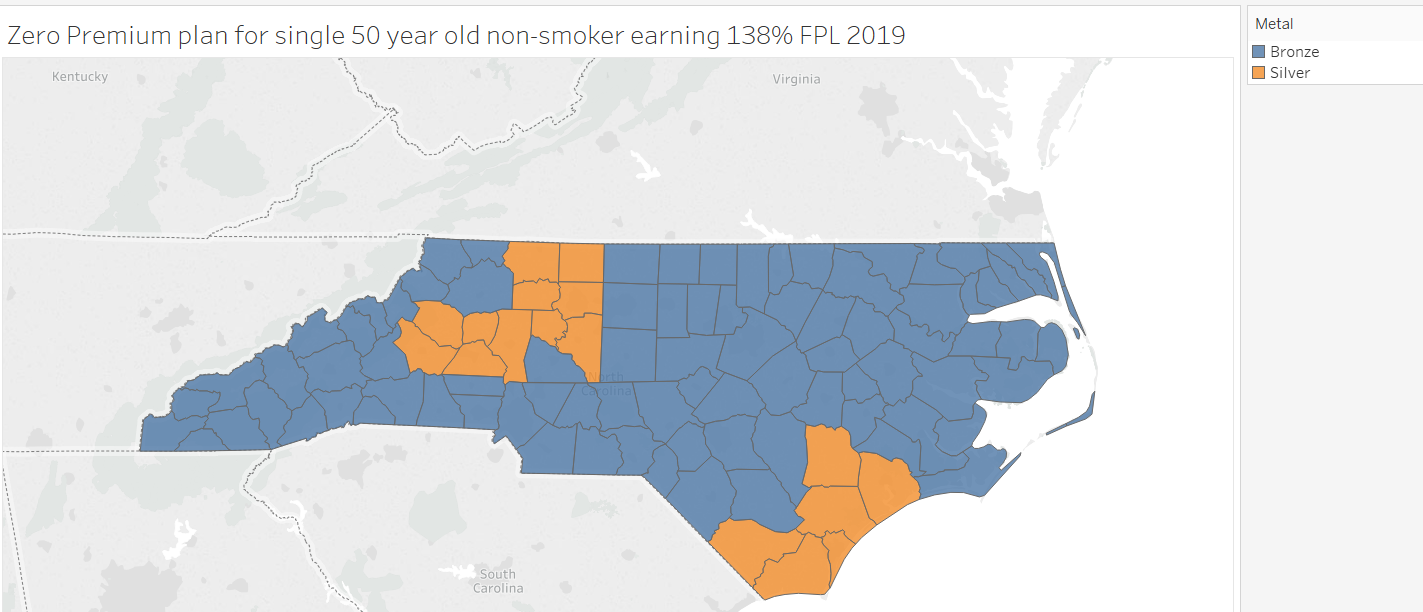

I am using Robert Woods Johnson Foundation HIX Compare data for the map below. I am looking to see what is the highest metal level (with CSR benefits included) that is available at a zero premium for a single fifty year old.

For someone at the top of Medicaid eligiblity, the zero premium plan requires them to spend several months of income before they get any non-preventive services covered by the insurer. If we hold the income constant and make the person younger, zero premium plans that are not bronze are even less likely. Older and larger families are more likely to see a non-bronze zero premium plan. At 100% FPL, zero premium silver plans are available for all single fifty years thoughout North Carolina.

If we make the assumption that plan quality matters and cost sharing attributes matter for significant elements of the 100-138% FPL cohort, then zero premium exchange plans, even zero premium 94% CSR Silver plans are, on some critical financial attributes, significantly inferior to Medicaid and zero premium Bronze plans are grossly inferior on those financial attributes compared to Medicaid. For these to be equalized, there has to be an incredible assumed quality differential between exchange plans that are offered by private insurers and Medicaid plans that will be soon be offered by most of the same private insurers as North Carolina transitions to Medicaid managed care. That assumption has to be heroic and so far unobserved.

Zero premium exchange plans have some really nifty attributes but they are not a near substitute for Medicaid expansion for the 100-138% FPL groups.

Matt

Shorter Civitas: “Private insurers should get to pocket 20% of the federal outlay for these patients because we’ve spent thirty years sabotaging Medicaid”

Scott

I have learned a lot from reading your takes on the health care system. What I find totally ironic is that I understand what you write (like this article) but I’m not a customer for what you’re writing about. On the other hand, those who would benefit from understanding whether it is a good idea to expand Medicaid or not would have a difficult time wading through this. This seems to me to be a big structural information hurdle for a lot of folks. Keep up the good work.

Duane

@Scott: One problem with private insurance is its crapshoot nature. People can’t be certain of what they’ll have from year-to-year or if they’ll have insurance at all. I have good insurance now, but what about next year?

J R in WV

Do you suppose Civitas would benefit from reading this information?

OR are they a front group for Republicans determined to fuck the most number of people out of health insurance that they can possibly manage to fuck off?

Probably that there… Republicans hating on people having health insurance. Does anyone know why Republicans hate health care so much? It seems the idea of someone seeing a doctor and perhaps getting better, more healthy, nearly makes Republicans foam at the mouth… so strange.

Didn’t their living god Jesus provide health care to his followers for free? But they don’t believe in that kind of Jesus, do they… That Jesus was generous and kind, dark skinned, with dark brown hair, and the Republican Jesus is mean and blonde, totally different guys. Explains a lot, they believe in the anti-Christ instead of the real deal…