Which plan is better for you? Which plan will have the lowest premium plus out of pocket expense?

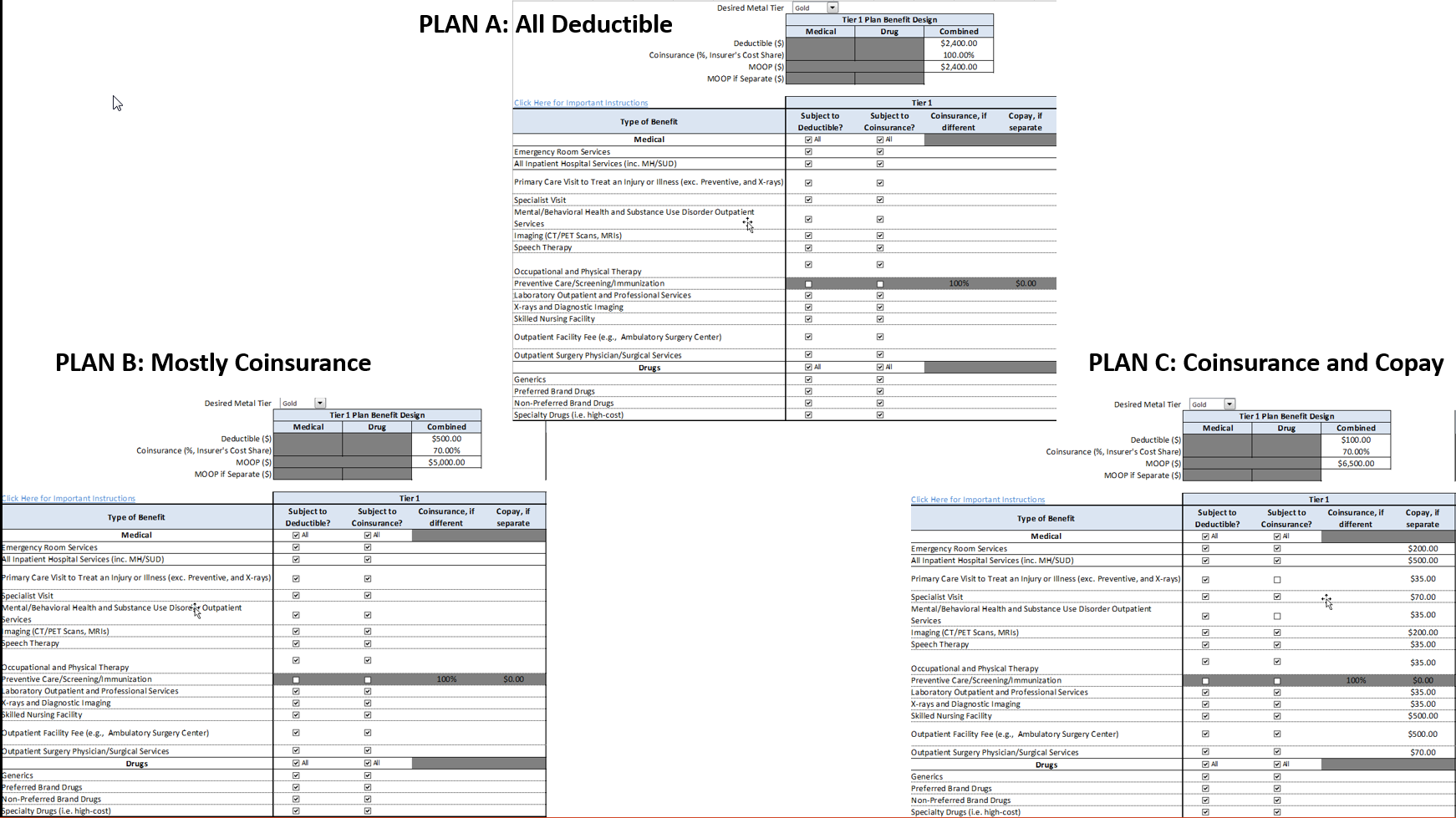

Plan A is entirely deductible for its cost sharing. Plan B has a $500 deductible and a 30% coinsurance with no co-pays for everything up to $5,000 maximum out of pocket. Plan C has a $100 deductible, 30% coinsurance and a variety of service specific co-pays to a maximum out of pocket limit of $6,500. Let’s keep things simple and assume that Plans A, B, and C are offered by the same insurer on the same network as an EPO. Let’s assume that the premiums are in line with their relative actuarial value.

Which plan has the highest actuarial value? Which plan is best for you?

I’ll give you some time….

The answer is simple:

IT DEPENDS!

The three gold plans have nearly identical actuarial value of just slightly more than 80% actuarial value.

However, the pragmatic valuation of the insurance varies tremendously by expected health status and expected ability to absorb a financial hit. For someone who has low expected expenses and is able to take a big surprise shock, Plan B or C looks attractive. For someone who expects to have large medical bills, Plan A looks pretty good. Plan A also looks decent to people with modest ability to deal with a worse case scenario and thus need significant downside risk protection. All of these plans will be equal to each other if total utilization over the course of a year is roughly one sick PCP visit with one prescription for a generic penicillin pill. After that, it really depends.

On The Road, Now With Mushrooms!

On The Road, Now With Mushrooms!

Tata

Let’s agree that deductibles are a nightmare and no plan should have one.

Ken

Ugh, math and spreadsheets. Can we just call this another demonstration of Arrow’s proof that there cannot be a free market for healthcare?

Ohio Mom

Ugh. This is too close to what I have to do within the next six months, choosing a Medicare plan.

I’m reminded of what my sister often says: “Their actuaries are better than your actuaries.” Meaning, you are an amateur, they are not, you are outgunned, the house always wins.

p.a.

Of course there’s a paperwork premium also. For those not on the financial cliffedge, an x% ‘surcharge’ for a ‘fewer hoops to jump/paperwork to deal with’ plan can be desirable.

David Anderson

@p.a.: Completely agree, hassle minimization matters a lot. A co-author of mine is working on precisely that paper right now, and I was lucky enough to read a pre-submission draft … IT IS COOL!

Ohio Mom

@David Anderson: I sometimes say, if each of us spends a third of our life sleeping, what percentage is waiting at red lights and what percent is arguing with health insurance companies?

When Ohio Dad’s employer went from UHC to Anthem, there was a definite uptick in the amount of time we and our doctors spent going back and forth on coverage issues. I guess it is a cost of going business for Anthem but for us and medical providers, it is a time suck we resent.