Open enrollment season is getting closer for most of us. Medicare open enrollment is in a few weeks, ACA exchange open enrollment is in a touch more than a month, and peak employer group open enrollment will be just about the same time as New Hampshire gets tired of the peepers but not their money.

One of the big questions is what type of plan is best? Is a lower deductible worth it?

That is one hell of a tough question. Basically, it depends on the interaction of you and your family’s expected medical spending for the year and the premium levels of a plan. The decision is “fairly easy” for people who know that they have massive upcoming medical expenses as their calculation is to find a good enough network and then minimize the total premium plus the out of pocket expenses. That is an “easy” choice set because there is no uncertainty.

Most of the time, there is uncertainty in anticipated future health expenditures. This makes the choice hard.

We’ll talk through a few examples with three different ACA individual market hypothetical plans.

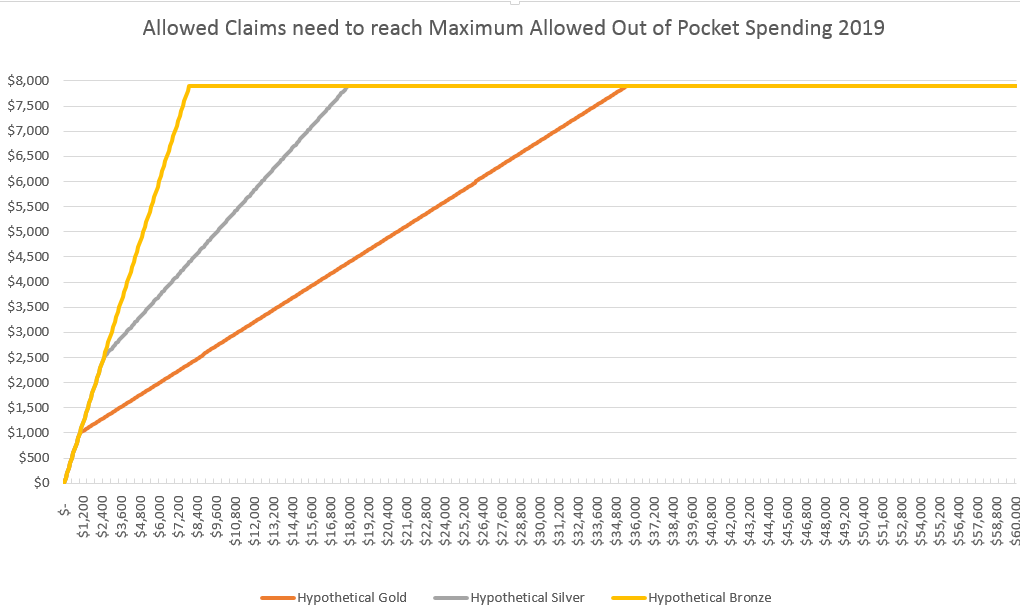

All of these plans are hypothetical ACA compliant plans that could have been sold on the 2019 exchange. We will assume that the three plans are all on the same network and are offered by the same insurer. We will also assume that there is no induced demand factor. The silver plan is a “standard” Silver with no CSR enhancement. Pricing is Bronze —-> big gap to Silver and Gold that are priced close to each other.

| Deductible | Coinsurance after deductible | Out of Pocket Max | |

| Bronze | $7,900 | 0% | $7,900 |

| Silver | $2,500 | 35% | $7,900 |

| Gold | $1,000 | 20% | $7,900 |

What is happening here?

Bronze, silver and gold plans are identical in their benefits for people who anticipate having between $0 and $1,000 in claims for the future year. The insurer pays nothing, and all of the claims expense is coming out of pocket. Between $1,001 and $2,500 in allowed amount of claims, bronze and and silver are the same. Bronze hits the common out of pocket maximum after “only” $7,900 in total allowed claims costs. Gold hits the shared out of pocket maximum after $35,500 in total expenses. If a person has “only” $30,500 in total allowed claims, their out of pocket expense for gold is $6,900 while it is $7,900.

So gold is automatically better?

NO!

We have not looked at premiums yet. If the premiums are the same for all three plans, then gold dominates bronze and silver as it matches premiums and provides more protection, longer than anything else. However, it is unlikely that premiums will be equal. Usually, bronze will be a lot cheaper than silver while gold and silver from the same insurer on the same network will be fairly tightly clustered given Silverloading. Gold usually beats non-CSR enhanced silver for most plausible spending regions as the financial protection of a higher actuarial value plan is either matched by cheaper premiums or is only slowly eaten up by gold’s slightly higher premiums.

However bronze and gold are in conflict. If we assume that bronze premiums are a lot cheaper than gold, bronze dominates at very low spends (<$1,000) and very high spends (>$35,500 or more) as the out of pocket costs are the same but the cheaper premium dominates. There is a narrow zone of gold superiority between $1,000 and $35,500 in claims where gold beats bronze.

The same type of decision process has to apply to employer sponsored insurance. It is a bit fuzzier as there is not complete banding and benefit designs may differ, but the fundamental calcualtion is the cost of premiums plus the cost of cost sharing which is a function of plan design interacting with future medical costs. From there, we should try to minimize given our ability to absorb a really bad surprise. This is tough.

Sarah in Kingston

It is very tough. I’m paying high premium for a low deductible gold plan but I don’t think it’s my best choice. Figuring out how/if I should change is very difficult and scary!

SP123

Related question- we’re close to OOP max for the year, about $450 short. Our plan is an HSA PPO with prescription benefits. But none of our prescription spending for the year (about $350 in copays) has been credited towards our OOP. Is that right or should it be counting towards our spending? When calculating whether we’d hit our max I assumed prescription spending was included. I also didn’t realize there was a separate accumulation of out-of-network OOP (8k max) vs in-network (4k max) so a foreign ER visit didn’t count toward the 4k. Hard to make educated decisions when there are so many hidden variables and rules.

daveNYC

The OOP max is $7,900 in this example. The median savings account in the USA is $4,830. These hypothetical min-maxing the policies scenarios lose their charm when the end state for all of them is likely wiping out someone’s savings and racking up their credit card bill.

Victor Matheson

In court cases I do with catastrophic injuries I routinely price in the cost of a Bronze plan. Seems counter-intuitive to use a Bronze plan when you would think you want the “best” insurance in cases of high medical use individuals. But after doing a bunch of these I was finding out that the patients were maxing out the ACA out-of-pocket even with the Gold plans, so why pay all of those higher premiums just to get lower co-pays.

guachi

Always happy I have military health care that’s free Also happy I have these posts to help me navigate health care choices (both policy and personal) going forward.

Kelly

Our income would put us over the subsidy cliff. HSA contributions don’t count as income in the subsidy calculation and put us back in subsidy land. We have sufficient savings to fund an HSA and withstand expenses up to our out of pocket limit. All our HSA options are Bronze. Our Bronze HSA premium is $3. We have saved thousands of dollars our the last two years with our Bronze HSA.