The least expensive premium (net of any applicable subsidy) determines the size and health status of the individual market ACA risk pool. We assume that the marginal buyer is flipping a coin as to whether or not they want to buy insurance. These buyers tend to be healthy and price sensitive. The point of the individual mandate was to make not buying insurance more expensive than buying heavily subsidized insurance so as to at least nudge if not hip-check healthier buyers into the risk pool.

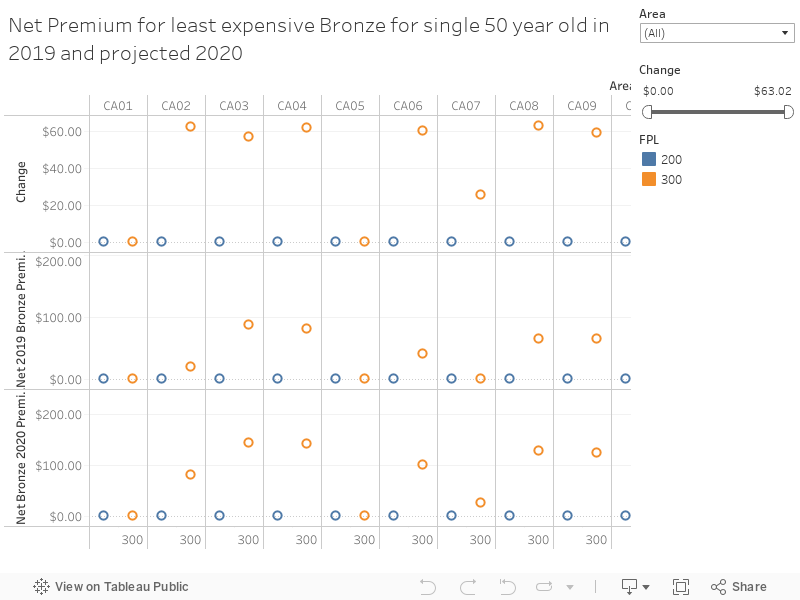

Yesterday, I outlined that Covered California will see lower silver premiums and higher bronze premiums. This action will compress subsidized spreads and potentially increase the net of subsidy premium for the cheapest bronze plan. Kevin Drum thought this was no big deal, but the details matter as I ran the numbers. I used the Robert Woods Johnson Foundation (RWJF) HIX Compare April 1, 2019 data set to calculate expected minimum premium for the cheapest Bronze plan in 2019 and 2020 for a single 50 year old non-smoker at 200% and 300% FPL for each rating area. A rating area is a group of counties where insurers have to offer a particular plan at the same premium. California has nineteen rating areas including two that split Los Angeles County. I used actual data for 2019 and projected a 5.7% increase in the cheapest bronze premium and a 4.3% decrease in the benchmark silver premium. I then calculated net premiums and changes from 2019 to 2020.

This is a significant set of changes in several rating areas in California.

2/N @ 200% FPL 14 of 19 rating areas would see no change in minimum premium. The spread between the benchmark and the cheapest bronze is bigger than the individual contribution amount

— David Anderson (@bjdickmayhew) July 11, 2019

3/N 5 rating areas would see cheapest plan increase. 2 would see ~$10/month increases, other 3 would see $38-45/month increases. Those 3 spike regions are part of Los Angeles, all of San Diego and Inland Empire so this is some real population

— David Anderson (@bjdickmayhew) July 11, 2019

6/N all of those spikers will have higher minimum net premiums even net of the new state subsidies in 2020 than in 2019. That will make some of the healthier folks drop off.

— David Anderson (@bjdickmayhew) July 11, 2019

The short version is that the changes in spreads will mainly hit folks earn between 200%-400% FPL if they are looking to buy the cheapest coverage possible. The new state funded subsidies will be smaller than the premium increases that we should expect. The state will be spending a lot of money to partially and incompletely back fill a problem that an actively managed market is creating. Previously the Feds were bearing the entire cost of making the cheapest plan very cheap and now the state is taking on some of that cost from the Feds as the spread is being compressed.

The ACA is complicated, and California is showing that seemingly good things have negative consequences for some groups.

Mormo

Thanks for running some numbers. I appreciate the work.

I do want to push back a little though on the model. Unless I’m missing something, all we’ve got is the press release with the lowest cost bronze and silver changes statewide (plus weighted average etc.). Which don’t necessarily map neatly onto the second-lowest silver (benchmark) change. And then extrapolated… Like you say, details matter. A lot.

For instance, for your 50 year old at roughly 200% FPL, area 16 has a very small gap between silvers this year ($1!) while area 15 has a big one (one less expensive plan from LA care). Is it really likely that the second lowest silver in both areas will go down by the reported percentage for cheapest silver? Or, more likely, there’ll be some convergence in area 15 and some divergence in area 16, which shows up as cheapest silver falling in 16 even as the benchmark may not move or even rise. Can we really say any more at this stage than “details matter, the market looks stable, and some federal dollars will be replaced with state even as there are likely to be some savings from healthier risk pools and broader coverage”? I am quite doubtful.

In any case the final rates are to be filed shortly I believe. Hopefully we’ll know more then. Honestly I’m kind of vaguely worried that there won’t be revenue from the mandate to pay the new subsidies, but I guess that’s a good problem to have.

David Anderson

@Mormo: I completely agree with everything that you’ve written.

Given that there is no withdrawals and IIRC some expansions, I think we can assume similar behavior within company across rating areas as there is very little wiggle room on benefit design to change premiums. The big swings are either going to be network, care management/utilization management, or risk adjustment flows.

Agreed, I need to redo this analysis in a couple of weeks when final rates are out and I will do that by zip code.

David Anderson

I’ve been hammering this point as I’ve had one manuscript published, another accepted, another under review and finally a revise and resubmit that I’m productively procrastinating away from at the moment that all are dealing with variation of this theme. This has been top of mind for the past three months for me — the ACA subsidy formula means a lot of common policy awareness heuristics go bonkers for at least some significant subgroups for any broad directional statement.

Mormo

@David Anderson: Absolutely agree! And you’re far more expert than I in this area.

I’m just an interested party (hello Los Angeles) and don’t think the assumption that similar behavior of insurers across rating areas, even if true (I’m not conceding), can reasonably be combined with the limited info about unweighted lowest cost silver to model second lowest silver rates.

Just looking at this one limited sample, lacare has a bigger silver difference in 2019 between areas 15 and 16 silver and healthnet has a much smaller one. Both are competing for lowest silver in the areas. So did somebody misprice an area in 2019? Or is it networks? Or some other choice?

I’m just arguing we don’t know enough from the limited info to guess meaningfully at 2020 benchmark now. Other than agreeing that it’s likely more or less stable in general and most areas will probably see some compression in minimum bronze to benchmark based on this release (especially as bronze has been noticeably enriched, something like 1.5%AV, as silver has held steady).