Michigan’s insurers have asked for a net, blended 2% rate decrease for the 2020 individual market year. 2018 and 2019 were major actuarial OOPSIES as revealed in the rate filings.

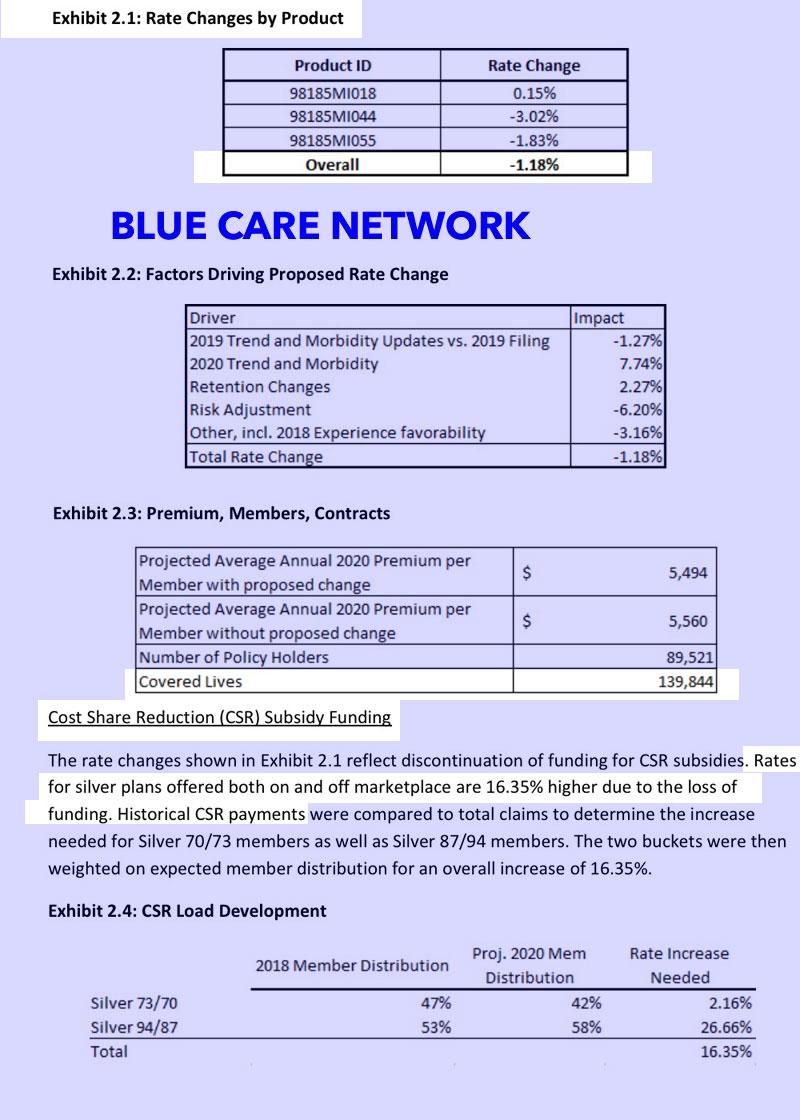

I am grabbing two screen shots that show the oopsies in rate filings. First is from Blue Care Network, the largest single individual market insurer in the state:

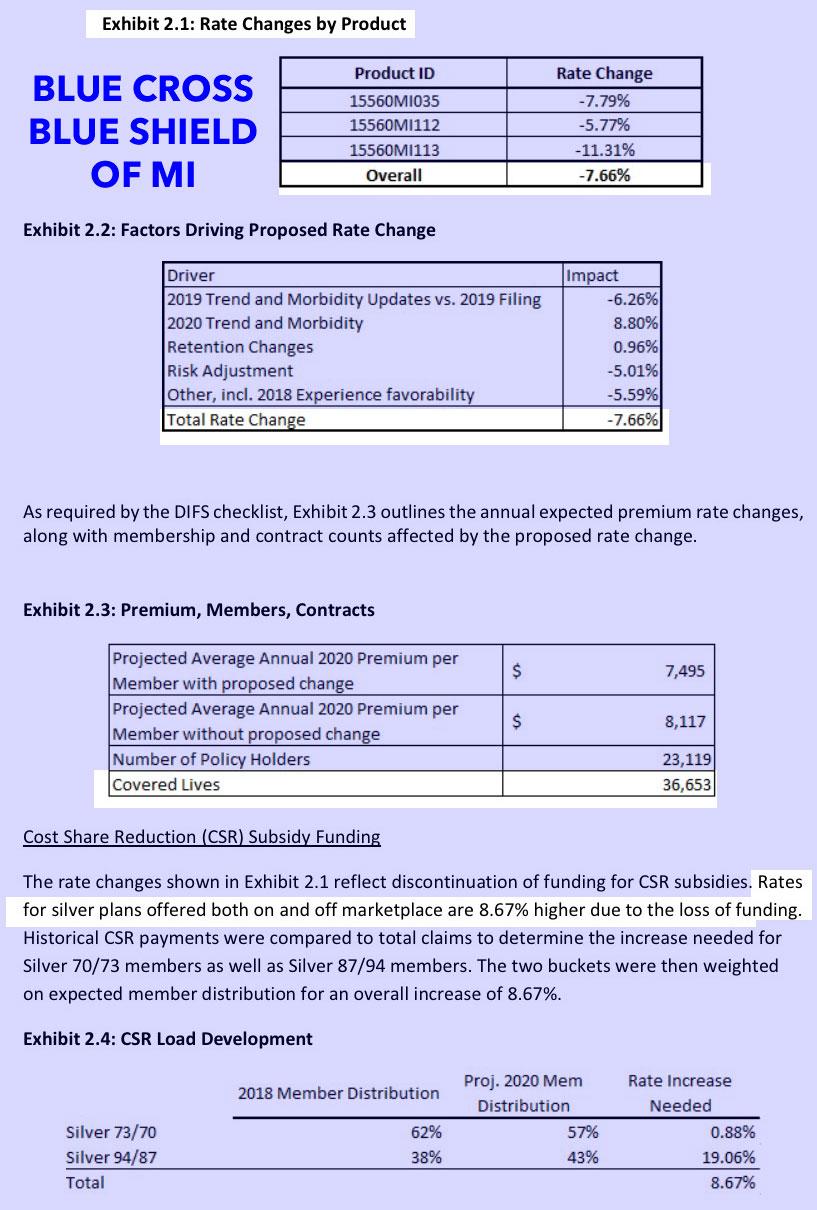

The second is from the other Blue Cross and Blue Shield of Michigan product line as it is even more explicit:

Exhibit 2.2 in both filings is where all of the action is. The short version is that the actuaries were way too pessimistic about 2018 and 2019. The original projection for 2018 and 2019 expected the federal policy actions to be the equivalent of the market getting knee capped with a tire iron. The combination of uncertainty in 2017 leading into the 2018 policy year, reduced outreach and continual negative messaging against the exchanges were expected to lead to only the super sick/expensive buying plans for 2018. The actuaries also expected the policy intervention of no individual mandate to matter a lot more in 2019.

I think both of those things matter (I have a paper on messaging regime changes that I just edited the proofs for over the weekend and our findings show it matters) but the impact on these two counts were counter-balanced by the incredible pricing discounts that the Silver Load strategy created for non-CSR buying individuals.

The actuaries thought that 2018 and 2019 were supposed to be a Category 4 Hurricane when reality had the storm come ashore as a big, messy Tropical Storm or a weak Category 1 that just went over a pool of cool water. This makes sense, actuaries as a profession are biased against making pricing recommendations that have “lose the company” risks. If they can’t predict something well based on past experience, the recommendations are to either assume a high rate or run like hell. In these two insurers’ cases, they assumed a high rate.

So why does this matter?

Medical Loss Ratio (MLR) rebate regulations is why it matters. Michigan insurers are indicating that they really guessed wrong in 2018 and 2019 on final rates. We know that 2018 has ridiculously low MLR. I’ve been using a 7% increase as my rule of thumb to determine if a state had priced 2019 close to “right” where right is defined as insurers thinking they are profitable and being in a non-refund position for 2019.

Blue Cross and Blue Shield of Michigan (the second filing) is stating that they think they overpriced 2019 by at least 10%. This means they should be expecting to pay a very large MLR rebate next year as they will be dealing with a “normal” 2017, a very low 2018 and a low 2019 MLR. Those checks will be arriving in the mailboxes of enrollees five weeks before the election cycle. The MLR checks are effectively “magic” money as they are treated as post-tax refunds and not as income for purposes of taxes and income restricted social service programs.

Large 2019 rebate checks will not be universal but they will be fairly common. Michigan will see quite a few next year.

Butch

I’m currently in the appeals process because Blue Cross of Michigan denied a claim for preventive care. I would do anything to get away from Blue Cross of Michigan; they’ve definitely made me a fan of single payer.