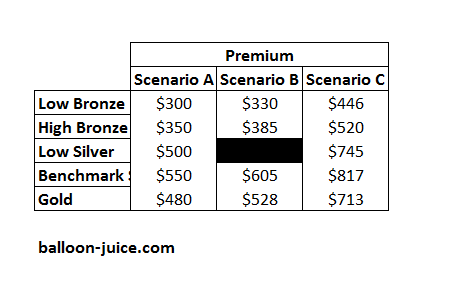

Let’s do a simple thought experiment. Let us assume that you are need to buy health insurance on the individual market. We will also assume that there is only a single insurer offering a single network with a common set of benefits across all scenarios. What scenario is best for you of the three below. I will show you the premiums only.

In most markets, the answer is easy — everyone wants Scenario A as it is the lowest price for identical plans.

In the ACA markets, it depends. It depends on if you receive subsidies or not.

In the ACA markets, no one should prefer Scenario B as a first choice. If one is subsidized, Scenario C is better. If one is not subsidized, Scenario A is better.

States and insurers are trying to figure out how file plans that allow for someone to be better off. Ideally, an insurer would be able to offer Scenario C to all subsidized buyers and Scenario A to all unsubsidized buyers. This can be done if the insurer is able to offer significant variation in plan attributes such as offering only on-Exchange/subsidized PPOs and off-exchange HMOs or by significantly varying networks. Benefit design decisions can be made so that the off-exchange plans are relatively low actuarial value with correspondingly higher deductibles/out of pocket maximums. However to do this greatly increases complexity and navigation costs.

So insurers and state regulators will make choices in multi-dimensional space that won’t be optimal on any single attribute.

takebakawashi

Is health care economics anything like this complicated in single-payer systems? Do most of the wrinkles get flattened out? Do new complications arise?

Would your job be boring or non-existent if you lived and worked in Ontario…?

Mudbrush

Every time my friend in Ontario tells me about her health care experiences I get green with envy.

David Anderson

@takebakawashi: My job would be different if I worked at McGill — probably more focus on care design and organizational financial structures rather than the front line interactions I write about here.

Butch

I’m thinking more and more than we need to shift the focus from health insurance to health care. My family has health insurance; I’ve discovered the hard way over the past few months that it does not equate to having health care.

Another Scott

Perhaps I’ve not had enough caffeine this morning, but I’m not seeing the logic here.

Doesn’t it depend on the amount of the subsidy? If the subsidy is, say, $50, then why would one want column C over B or over A? Are you assuming that the subsidy takes care of the whole premium?

Let’s say one wants a Benchmark Silver (as we learned from Prof. Mayhew that that is almost always the best baseline because of cost sharing and the like). If the subsidy doesn’t cover the whole premium, why would one ever pick column C? What am I missing?

Thanks.

Cheers,

Scott.

Villago Delenda Est

I think it all depends on from who’s perspective “optimal” is. Surely the health care consumer comes in dead last.

different-church-lady

Let us assume I can afford even the lowest figure on that chart.

[closes eyes, assumes…]

Gosh, that was a lovely assume. But now I have to get back to my real life…

Brachiator

@takebakawashi:

Interesting question. But also keep in mind that universal health care systems are not necessarily single-payer.

David Anderson

@Another Scott:

Scenario C has big spreads, so Bronze and cheap Silver are really cheap for subsidized folks

Scenario A has low levels so non-subsidized folks pay the least for any given plan

Scenario B has medium spreads and medium levels while only having a single Silver plan means CSR plans aren’t particulary cheap for 100-250% FPLers

karen marie

I have no idea what any of this means. I just can’t with the complications of figuring any of it out, particularly when, as butch pointed out, having health insurance doesn’t equate to having health care. Even with insurance, I still cannot afford to get sick. There has to be a better way.