Robert Camner asked a good, broad question yesterday that I want to respond to:

I’d be even more interested in your analysis of whether a public option that is designed to compete with private insurance plans in a standardized manner is (or is not) good public policy, which I would define as “the greatest good for the greatest number + providing an appropriate safety net for the most vulnerable

This is a damn good question.

Here is how I think about this problem. I first divide the universe into the subsidized, non-subsidized earning over 400% FPL and then the general population of the state.

From here, I first look at people who are eligible to buy individual market insurance but not able to be subsidized. They are no worse off on a simple model as a new choice is being offered. If it is a better choice (better network, better cost sharing, better customer service, better premium… better is a broad term here), they’ll buy the better choice and their welfare improves slightly. If the public option choice is not better, they are no worse off. For this group, a public option makes no one worse off and potentially some folks better off as well as potentially covering some people who otherwise would not have been covered.

This is the simple case. After this, it gets complicated.

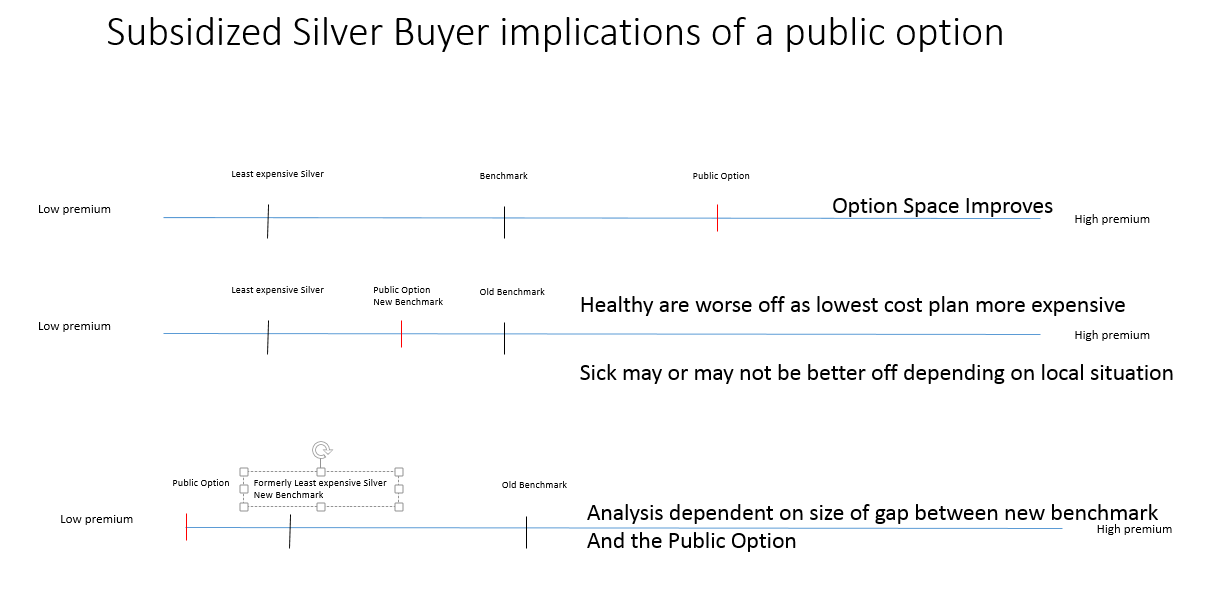

The main variables for the subsidized population are the relative price spreads of all non-benchmark plans to the benchmark. If the public option is priced at or above the current benchmark, the analysis looks a lot like the non-subsidized analysis. The choice space slightly expands and potentially the quality of plans being offered by private insurers increases. It won’t significantly increase enrollment nor lower costs but it is a minor welfare improvement.

If the public option is priced below the current benchmark, but above the current least expensive silver plan, it becomes the new benchmark plan. Enrollment probably will decrease as the cheapest silver plans will become more expensive and it is more likely that the cheapest non-silver plans are also more expensive (holding all else equal). This is based on the strong assumption that the marginal enrollee (ie the person flipping a coin to sign up) is extremely price sensitive and making an ACA plan net of subsidies more expensive will lead to them deciding to not get covered. Individuals who have high medical needs may be better off if there is a significant qualitative difference between the public option and the old benchmark plan. They could see a qualitatively better plan at a lower net of subsidy premium but this will not substantially change the enrollment universe.

Now if the public option is priced below the least expensive silver plan, the analysis is dependent on the local circumstances. If the public option is priced at a wider spread than the previous cheapest silver to benchmark spread, enrollment will increase as net of subsidy silver plans are now cheaper. Total enrollment may or may not change depending on the spread of cheapest overall plan relative to benchmark. Individuals who want/need to stay in above their current plans may be slightly worse off.

If the spread of the now cheapest public option to the new benchmark is less than the previous spread, then enrollment will probably decline.

The clearest beneficiary of a public option that is below current counterfactual benchmark is the federal treasury. After that, it gets really complicated really fast.

Now from the perspective of a state citizen who is not on the individual market, a public option probably slightly increases the option value of telling my boss to go shove it and walk out. That is a marginal value gain but it is real. Beyond that, it is a wash assuming that the state can administer the program in a way that does not introduce new on-budget costs that compete against other desired public expenditures.

On the Road and In Your Backyard

On the Road and In Your Backyard

Fair Economist

The really big shift from a public option is that it ends monopoly/oligopoly pricing, which is a killer in a number of markets. Also, don’t forget that if the public option saves the federal government money, that money can be redirected to increase subsidies, raise the Medicaid limit, etc.

David Anderson

@Fair Economist: Everything in your comment I agree with but need to caveat that it is extremely context dependent.

In reasonably competitive markets, a public option does very little. In monopoly markets, if there is a benevolent monopolist, the public option probably hurts subsidized buyers. If there is an asshole monopolist OR an incompetent monopolist, the public option probably helps.

As far as feeding money back into the state for other good things; that is a fairly complex waiver application that probably would not be approved until at least the 2021 plan year. It is not automatic

CindyH

No wonder we can’t get decent health care policy – requires thoughtfulness and analysis – something the party in control thinks is anti-American.

patrick II

From what little I know of countries with government provided health insurance, the government insurance provides some level of coverage with a private option for expanded care, much like our medicare and medicare supplemental. If the long the long term goal of the public option is to replace the private mishmash of private plans, should we also be offering guidance for and regulation of public option plus plans? The flexibility that affords seems to be a common pairing where there are government plans.

David Anderson

@patrick II: Most likely yes, but that is a 2023 or 2029 problem and not a 2019/2021 problem.

Litlebritdifrnt

Speaking of the public option just watched this on Youtube. I agree with every f*cking word.

https://www.youtube.com/watch?v=4Q1ydhgJPTE

Fair Economist

@David Anderson: Aren’t the insurance monopolists basically always assholes? I know Blue Cross is.

JDM

I would much prefer that what healthcare I can get be decided by doctors, me, and an appointed government panel (yes, panels, I’m for ’em) than by an insurance company lackey who is tasked by their bosses to deny coverage as a first step. I would also much prefer that if I’m injured or in need of emergency services at a hospital I simply go to the hospital without worrying if I might be assigned a doctor from outside my network thereby costing me thousands of dollars.

jl

All this analysis is intractable until there is some price transparency and agreement on basic uniform mandatory benefit package that everyone has to buy. There needs to be some mechanism to identify actual average and marginal costs of care versus quasi rents due to local monopoly and oligopoly power held by insurance companies and corporate providers in state and local markets. So, I fear David is increasingly playing using ground rules that will ensure he is forever lost in deep weeds.

A clear road map with market based prices requires more highly regulated market, as in Netherlands or Switzerland. Remember that a stable competitive equilibrium in insurance market with heterogeneous risks often DOES NOT EXIST. Anybody want to find a clear road map through churning chaos, good luck. The late Uwe Reinhardt can’t write any more, but his articles on the pricing problems of health insurance and medical care in the US are still worth reading. As is Rothschild-Stiglitz results on lack of competeitive equilibirum in insurance markets.

So, I fear policy paralysis by problems intractable by analysis at this point of David’s approach.