Monopolies are usually a bad thing. They lead to higher prices. They lead to poor service. They lead to rent extraction to pay for hookers snorting the finest blow. All of that is true. But given price linked subsidies for the 100% to 400% Federal Poverty Level, monopoly insurers have the ability to choose the size of their covered risk pool.

There are several flavors of monopolies within a given state. The smallest and least powerful is a single insurer covers a county or set of counties in the state while adjoining counties have multiple insurers. In 2019, UPMC Health Plan (my former employer) in Pennsylvania is the sole ACA insurer in several rural counties. UPMC’s pricing and plan offerings would be influenced by risk adjustment concerns and potentially marketing concerns from other, more competitive regions. A state can have multiple counties with a single insurer while having multiple monopoly insurers.

The next flavor is a state where every county has only a single insurer but there are two or more insurers. Arizona in 2018 was like this. Insurers still need to be concerned about how other insurers price due to risk adjustment concerns but there is a good amount of flexibility.

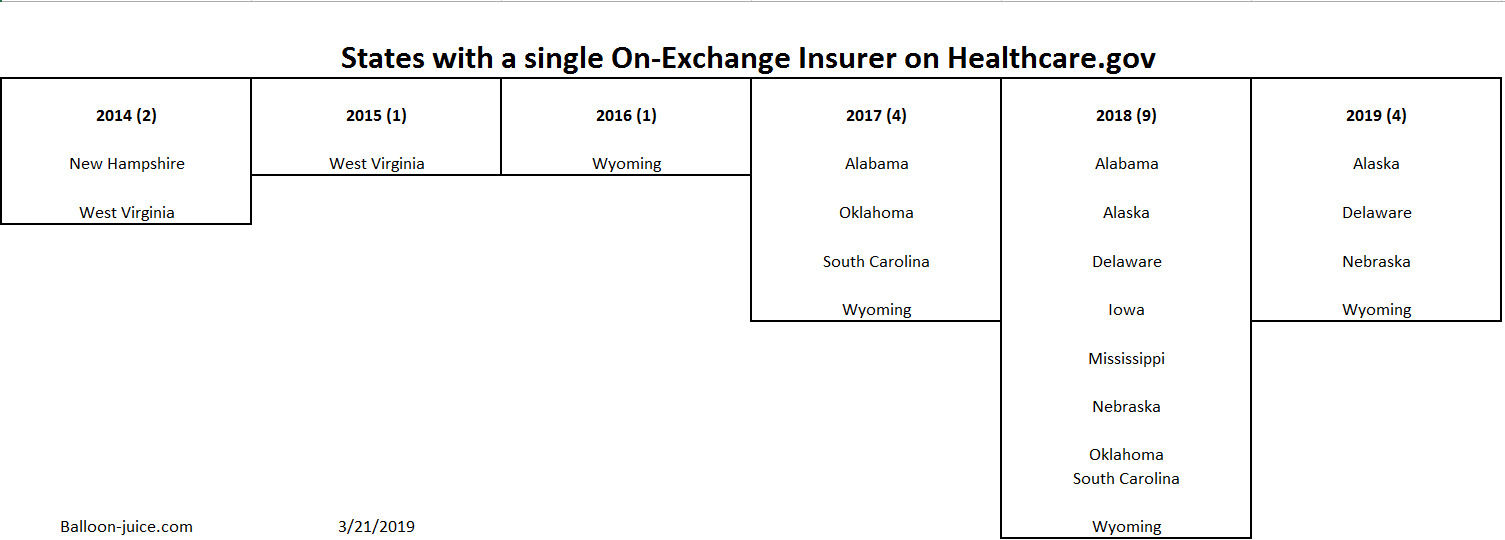

Finally, there is a single insurer covering the entire state. From 2014-2016, this was rare on Healthcare.gov. Now it is becoming more common.

I think 2018 is fundamentally an analytical mulligan for most ACA studies. It is a dividing year between how the Obama administration ran the exchanges and how the Trump Administration will run the exchanges. Insurers did not know what the rules would be until three weeks before open enrollment when CSR payments were terminated. When insurers don’t know the rules they either raise rates or run like hell.

In 2019, the four monopoly states have no more than three Congressional districts (Nebraska) and most have only a single representative. These are very small states. The same pattern was true 2014-2016.

I am curious about the insurer strategies in these true monopoly states. I think going forward, we should expect a few states to be single insurer every year and that those states will have the opportunity to choose their own risk pool and enrollment profiles.

On the Road and In Your Backyard

On the Road and In Your Backyard

johncarter

Being from Southwestern Pa and having to live through the BS from Allegheny County’s largest employer who claims non-profit and tax exempt status, I can well understand UPMC’s plan is to make themselves, by ANY means, Pennsylvania’s ONLY insurance provider, and with rates as high as the public can’t bear.

UPMC is NOT a friend to anyone who desires healthcare who isn’t already well off, and I mean WELL OFF!