Yesterday, John embedded the President screaming into the void that he can fix healthcare again:

A statement by the President: pic.twitter.com/vNXlXfaee6

— Real Press Sec. (@RealPressSecBot) December 17, 2018

He could have taken a W on healthcare after last year.

I made this argument in the New York Times in October 2017:

President Trump once promised a health care plan that would have “much lower premiums and deductibles while at the same time taking care of pre-existing conditions.”

That plan may be Obamacare. Mr. Trump’s decision to end cost-sharing-reduction subsidies, known as C.S.R.s, and perhaps to derail a bipartisan bill by Senators Lamar Alexander, Republican of Tennessee, and Patty Murray, Democrat of Washington, that would restore C.S.R. funding through 2019 may actually lead to better coverage for more people paying lower monthly premiums….

By pulling the plug on C.S.R. subsidies, President Trump can claim that he will provide a better deal on health insurance for more Americans. He and his fellow Republicans should declare victory, with or without a version of the Alexander-Murray bill — and check health care reform off their legislative list.

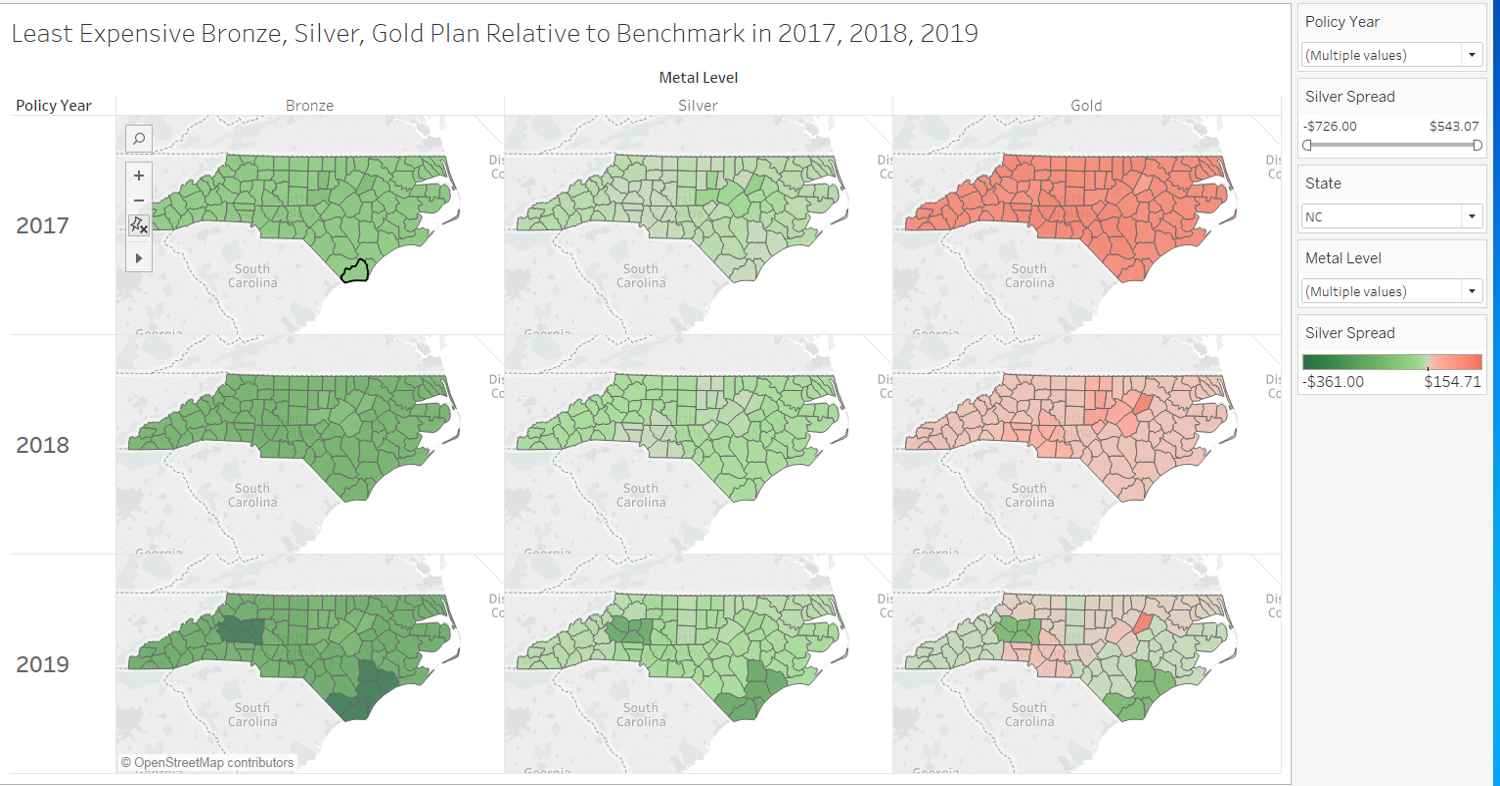

North Carolina is a good example of the facts on the ground regarding prices paid by subsidized individuals.

People earning between 100% and 400% FPL have lower premium plans with lower deductibles now under Trump than they did under Obama. In Wilmington, North Carolina, a family of four can get a $0 Gold plan with a family income of at least $65,000. That same family can earn up to $98,000 to get a $0 premium Bronze plan. These types of pricing spreads are not uncommon. They are the direct result of Trump Administration policies. The biggest driver is the termination of Cost Sharing Reduction subsidies that led to the overinflation of Silver benchmark premiums.

The problem with this fundamental argument of people actually being able to find insurance with lower premiums and higher actuarial value is that this is not the vision of health insurance that animates conservative policy making. It would not be considered a victory. Instead, the conservative vision is low actuarial value plans that are tied to health savings accounts. There is a two fold theory of change:

theory of change with the use of HSA in both a single year and over a lifetime. The single year theory of change is that high first dollar expenses will lead to lower utilization with minimal real health consequences as people become expert shoppers and evaluaters of health care need and value. The lifetime theory of change is that an HSA can be built up while an individual is young and healthy and spent when an individual is old and sick. It prefunds some of the expected health cost obligations on an individual level.

The reality on the ground would allow for the President to claim a victory as he at least partially delivered on his rhetoric but it conflicts with the policy class of the GOP’s policy vision.

Downpuppy

The notion of Trump declaring victory based on something both real and complicated runs against everything we know about the world.

Patricia Kayden

Republicans have controlled Congress since President Obama’s second term. If they wanted to fix the ACA, they’d have done something long ago. Hopefully Democrats will control the White House and Congress in 2020 when they can then fix the ACA.

Brachiator

Conservatives hate the idea of insurance. They keep trying to find ways for individuals to pay for medical services. That millions might go without or be denied health care because of pre-existing conditions doesn’t really concern them.

ETA. And Trump wants to score another petty victory over Obama.

Tim C.

@Patricia Kayden: I don’t see a valid path to 60 in the senate though. 50+1 will be enough for appointments though.

Yarrow

David, what do you know about Texas trying to come up with its own healthcare plan? I heard something about that on the radio yesterday when I was out and about so I didn’t catch all of it. Something about Gov. Abbott said they were working on their own plan and the TX Leg is going to go into session next year so they’ll work on it. I got the impression from the report that the statement dovetails with the recent decision by the TX judge about the ACA.

Southern Goth

Explain please. Our non-subsidized health insurance in NC is dropping about $350/month next year and I’m still trying to understand that or why it was so over-inflated in the first place.

tobie

I’ve never understood the fixation on health savings accounts. One major and unexpected health crisis — a ruptured appendix, a diagnosis of cancer, a car accident — will lead to intensive and frequent medical procedures, tests, and doctor’s visits that will quickly eat through the few thousands of dollars you’ve set aside (assuming you’re lucky enough to have enough disposable income to set aside several thousands). One thing that occurs to me, though, is that if conservatives think HSAs are the future, they obviously don’t believe in employer provided health insurance any longer. Yet again they’re making the case for M4All.

Yarrow

@tobie: Health Savings Accounts are a tax shelter for rich people. That’s the fixation on them. I mean, they do work for average people with a little disposable income, but as you said, one health incident and you’ll go through that money. Meanwhile, rich people can hide their money there.

Steeplejack

@tobie, @Yarrow:

In a country where, what, 40% of the people couldn’t cover an unexpected $400 expense of any kind, the idea that everyone will “prefund” an HSA is ludicrous.

Yarrow

@Steeplejack: It absolutely is. I guess given your statistic they do work for 60% of the country, at least to a certain extent. But there is no way they can be the main way people pay for healthcare. It’s wrong on so many levels. Especially if there’s a major health crisis to deal with.

tobie

@Yarrow:The idea that health savings accounts are tax shelters for the rich makes sense to me. Thanks for the explanation.

@Steeplejack: Good point. Even if people set aside the premiums they pay every month, that would cover only a fraction of medical costs in the case of an accident/unforeseen illness. And, of course, that doesn’t account for all those who receive Medicaid, which is a far larger group than those who purchase individual plans. Last I read people who buy plans on the exchanges amount to about 6% of the population.

jonas

@tobie: The idea with HSA’s isn’t that they’re meant to cover all the costs of a major medical expense, but that they cover a large deductible so that you (theoretically) pay lower premiums up front. Of course, this presupposes that 1. you have access to an insurance policy period, and 2. you have a few extra grand to sock away every year above and beyond what you’re already saving for retirement, college, etc.

Brachiator

@tobie:

As I noted in an earlier comment here, conservatives hate or don’t understand the concept of insurance, and want to “empower” individuals by letting them save money to pay a doctor or to buy (crappy) health insurance.

And although HSAs may appeal more to rich people (who have other options as well), it’s part of the conservative mania for school vouchers and expanded 529 plans (originally for college, but now also for primary and secondary school programs).

You might be right. Conservatives would sit back and watch employers get rid of health insurance. But Republicans are again inconsistent on this. Many of them connect employer-provided health insurance with individuals proving that they are not bums by having a job. By extension, they hate universal health insurance not connected with employment because, in their eyes, it lets people be social parasites.

gene108

@tobie:

@Yarrow:

I have an HSA, and I like it. I blow through what I contribute every year, so I don’t get the benefit of investments, but it is a nice way to save for medical expenses and get a tax break.

Obamacare made high deductible plans the norm. Therefore, saving to cover for the deductible with pre-tax dollars is a nice benefit.

Barbara

@gene108: Obamacare DID NOT make HDHPs the norm. HDHPs have been increasing in popularity since well before the ACA, and that trend was initiated by large self-funded employer plans. The overall effect of an HDHP is to shift the burden of health care expenses to people with chronic conditions and predictable health care expenditures, e.g., people whose dependent children have asthma and allergies. The HSA component allows the relatively well and well-off to have another tax-free way of essentially maintaining lower priced lower deductible coverage. I don’t think employers are evil for doing this, they have tried a gazillion different things to lower costs and having either failed or met significant employee resistance, this is what they arrived at. But please don’t blame Obama. Geez.

artem1s

@Barbara:

This. My employer has been able to maintain a pretty low premium match by offering a high deductible option. We do have a choice to go with the higher priced plan with a lower co-pay and deductible. But most of the staff (mostly middle income) opt for the lower premium. Why wouldn’t they? By putting the max savings in a special savings account, they can lower their adjusted gross income. It’s no different than any other pre-tax deduction my employer offers. It’s essentially, tax free income, as long as you save it or use it to pay medical costs. And you can use it for over the counter meds, eyeglasses, dental, etc. It’s been the best thing about ACA for me. If I have a catastrophic event, it’s going to cost more than my deductible anyway. And I get to save money I otherwise would have been throwing down the bottomless pit of premiums. HSA’s aren’t the problem and they don’t only benefit the rich.

Barbara

@artem1s: They mostly benefit those who are both well and well-off. They really aren’t a good policy, but they placate affluent employees who are used to a high level of benefits.

Raoul

Corporate capture of the GOP is perhaps at it’s most obvious and most galling in the realm of health care. No other country on earth, as far as I know (but I’m no expert) blows so much money per capita yet yields such craptastic results.

Some of that is the massive tons of money shoveled at making the last year of old people heroic rather than comfortable. But a lot of it is a combo of business greed and wildly overcompensated medical specialists.

I know med school is expensive. I know it’s hard. But honestly, my 36 y.o. cousin actually shouldn’t be able to afford an $800,000 house as a relatively newly minted sub-sub-specialty surgeon. But he can!

Fleeting Expletive

Mr. Anderson, I have a Medicare question on Late Enrollment Penalty for not having RX (part D) coverage. As best I can tell, the 63 days w/o coverage, and then you get the penalty, is for AFTER you sign up for D, or is it 63 days (w/o RX coverage) after you initially enroll in Medicare? I went for 6 years after age 65 w/o RX coverage b/c I didn’t need to take much prescription medicine. Will I incur the penalty now, for the rest of my life? Looks like it’s about 36$ a month but I’m a bit confused. Thank you.

John

So great that a family of 4 making up to $98,000 can get a Gold plan for $0!!!

Meanwhile in NY I will be paying $780 or so monthly next year for a gold plan for a single healthy 45-year-old. And it’s Fidelis so it is very narrow network.

So glad though that Obamacare works out so well for everyone else.

Felanius Kootea

@John: So sad that there are not enough Republican politicians who care about your predicament to actually fix the problem. Too bad that many people around the country who actually need better healthcare will continue to vote for representatives and senators who view their constituency as the health insurance CEOs’, not the people who went to vote.

Barbara

@Fleeting Expletive: Yes, but I think it is limited to every month you delayed signing up, which will be quite a while for you. The penalty is intended to actuarially offset your non-participation when you didn’t have need for the coverage.