Picking insurance is tough. It involves an ungodly number of trade-offs and incredible amounts of decision making under uncertainty for most people. Some people have an “easier” task because they know that they are facing a $500,000 claim year no matter what so their problem is a well defined and well constrained optimization problem. Most people are luckier in that they aren’t facing a guaranteed OMG claim year but this makes the optimization problem far fuzzier.

Which plan is better for your family? Let’s assume that the two hypothetical plans below are from the same insurer with the same network, plan type and otherwise identical details except for the pricing and the cost sharing. The cost sharing is very simple; everything goes to deductible and then if there is a co-insurance, it applies to every claim above the deductible amount and below the out of pocket maximum amount. This is a simplification but I think it will provide useful insight.

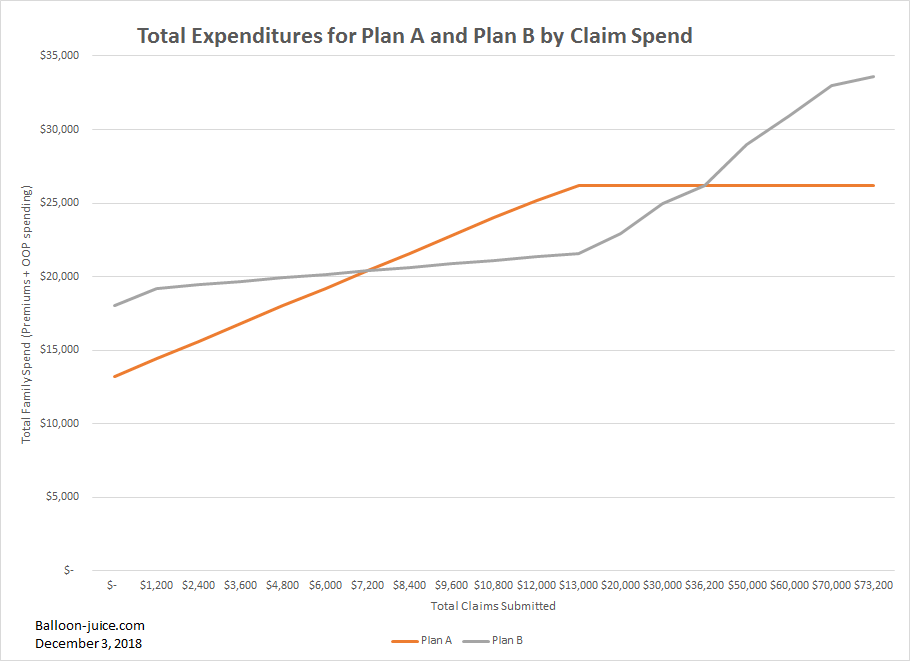

| Plan A | Plan B | |

| Monthly Premium | $ 1,100 | $ 1,500 |

| Annual Premium | $ 13,200 | $ 18,000 |

| Deductible | $ 13,000 | $ 2,400 |

| Coinsurance | 0 | 20% |

| Max OOP | $ 13,000 | $ 15,600 |

Plan A has a lower premium but a higher deductible. Plan B has a higher premium, a lower deductible but co-insurance that builds to a higher maximum out of pocket expense.

Which plan is better?

Well it depends….

What do you anticipate your family’s claims cost will be for the next year. Let’s start with two extreme examples. If your family submits no claims, then you pay the premium and nothing else. Plan A is cheaper than Plan B. Now if you have a million dollar year, the cost is premium plus out of pocket maximum. Plan A is again less expensive than Plan B. But does Plan A beat Plan B in all scenarios?

No.

Plan B has a zone of superiority over Plan A.

Plan B beats Plan A on total costs if claims costs are between $7,200 and $36,2000. In practical terms, Plan B is better if an uncomplicated pregnancy or a simple knee replacement are going to be the dominant episode for the year. Plan A is better if the family has relatively good luck or gets hit by an expensive diagnosis.

These zones of superiority are tough to calculate as I have massively oversimplified the insurance benefit designs to get these mechanical examples. I am also neglecting any tax advantages of Plan A’s health savings account which narrows the net superiority zone of Plan B significantly.

We soon start moving to the same type of calculations that early 20th century warship designers had to make when they were armoring battleships. No ship could be armored against a peer’s guns at all ranges. Instead the designers would try to balance thick belt armor for protection against horizontal fire with thinner deck armor to protect against vertically plunging fire. These trade-offs would hopefully create a several mile wide zone where a battleship’s critical functions could be protected against all likely hits. The trade-offs were based on likely enemy gun energies, fire control capabilities and the projected area of engagement as North Sea storms and fogs would have ships engage at far closer range than the clearer weather of the central Pacific. No armor scheme was impenetrable to all guns at all likely combat ranges; instead the designers had to accept risks and uncertainty even as they tried to minimize the negative outcomes of their choices.

We have the same trade-off set with insurance choice.

On the Road and In Your Backyard

On the Road and In Your Backyard

debbie

I have insurance through my employer, but every damn year I pick the wrong option. I even miscalculated my HSA this year!

ETA: The year I went for the higher priced, lower deductible, I only got $5.00 over the deductible. There’s no winning.

Another Scott

Thanks for this example. I have always figured that there were always caveats and grey areas in comparing plans – there is more than best case and worst case considerations.

It would be very interesting, I think, if you could do a similar example for a hypothetical Medicare buy-in. E.g. Nancy SMASH introduces a When-You-Turn-60-You-Can-Buy-Into-Medicare system (with as many simplifying constraints as you need). Should Congress pass it? Should everyone do it, or just people on the left-and-right tails of the distribution? If not, what changes would be needed to make it more compelling?

Thanks.

Cheers,

Scott.

dr. bloor

Sitting around the kitchen table trying to figure out how many of us are going to be hit by a bus in the coming year is a tradition on par with Chanukah, Christmas and Festivus in our house.

Butch

As a result of a layoff last June we are now eligible for a subsidy but I picked the highest Bronze plan and now I’m panicked that I’ll earn too much at my current part-time work and end up owing. So do I worry about possibly owing on the Bronze plan or paying the bills every month?

David Anderson

@Butch: What is your health status? And can you pass underwriting if you make too much money?

Butch

We’re currently on an underwritten policy but it excludes spouse’s pre-existing condition. My insurance agent looked at the underwritten policy and said it was good but it still has some exclusions and limitations that make me nervous, so I’d rather be on a policy that complies with the ACA – that’s why I decided to switch. I can’t switch in mid-year if I make too much off the part-time work, can I?

David Anderson

@Butch: I would go talk to a navigator/certified assistance counselor (CAC) for the ACA plans regarding Special Enrollment Periods.

One possibility would be for you to stay underwritten and for your spouse to go ACA

Butch

Maybe it would be better to go with a cheaper plan just in case – I will speak with a navigator and see what happens. Thank you, David!

Burnspbesq

@debbie:

You win if you actually need care. I’ve resisted my employer’s annual entreaties to move to a higher-deductible plan, and I hit the jackpot this year. I just received the hospital’s bill for my weeklong stay back in March. The gross amount of the bill is $103,000. I owe $2,800.

hilts

OT

Donald Trump apparently had some diaper change emergency issue at the G20 Summit

h/t https://www.mediaite.com/online/hot-mic-catches-trump-awkwardly-leaving-g20-photo-op-stage-get-me-outta-here

Shana

Younger daughter turns 26 on 12/29. She’s currently in TX and has a one year job that ends in July I think. She doesn’t make a lot of money and estimates her income for next year will be about $21,000. She has some digestive issues for which she takes an OTC probiotic that she has to get from her pharmacy. She has had strabismus (eye crossing) surgery 3 times in the past, last one was in her early teens. She’s unmarried and has the bc implant.

She and Hubby were looking at plans last night and were trying to figure out if she’d be better off with a bronze or silver plan. Any insight?

stinger

David, I appreciate your expertise in other areas of health care insurance, but thank you so much for basic plan comparison and analysis like this. I’d weigh in alongside Another Scott and hope that some time you can discuss Medicare Advantage. (If you’ve already done this in any detail, I missed it.)

I just turned 65 and have been getting bucketloads of mailings all year. Since I’m staying employed and staying on my employer’s medical/dental/vision plans, I only signed up for Part A and just collected the mailings out of curiosity. But in a year or two I will probably make the switch and will need to sign up for Parts B, C, D, and whatever.

I really dread having to parse out using some national, well-known brand versus dealing with a local but unknown to me entity. I can’t even figure out if the mailings are offering me insurance or offering to help me choose insurance! Medicare doesn’t seem to be any easier to navigate than the rest of health care insurance in this crazy system we have. It’s okay as a catch-phrase, but I would be against “Medicare for All” as an actual policy implementation.

The Lodger

@stinger: Here’s another vote for a discussion of Medicare Advantage. I’ll be turning 65 in January, I want to continue working and have no idea whether it’s better to take a Medicare Advantage plan and find other coverage for the wife and kid, to stay with my work-provided plan for the family and defer Medicare, or do something else.

David Anderson

@Shana: Given that she makes $21,000/year, she qualifies for CSR-87 Silver at a benchmark premium of $90 to $100/month.

that gives her pretty good protection against any hospitalization for a bit more a month in premiums. There is a decent chance that she will be able to get a $0 plan Bronze plan with a $5000+ deductible.

The trade-off is whether or not she can finance a major catastrophic event and how likely that event is in the upcoming year. If I was her age and in her shoes, I’m thinking Silver with the CSR bump.

David Anderson

@The Lodger: Sounds good… probably Wednesday’s post will be a Medicare primer.

debbie

@Burnspbesq:

Yep, that’s a jackpot alright. So is the waiting nine months to bill you.

Shana

@David Anderson: Thanks David, that’s pretty much what we thought. I’ll pass this along.