The Kaiser Family Foundation has another issue brief on the financial performance of individual market insurers through the end of the first half of 2018. The short story is that insurers are Scrooge McDucking it right now in the individual market as they massively overpriced 2018.

This has been my core analysis since March; insurers got frightened and believed (with little state regulator pushback) that the ACA individual market morbidity would have fallen off the cliff. So far it has gotten slightly worse (4% more inpatient days) but it did not crash through the bottom. So what would “accurate” or “fair” pricing looked like?

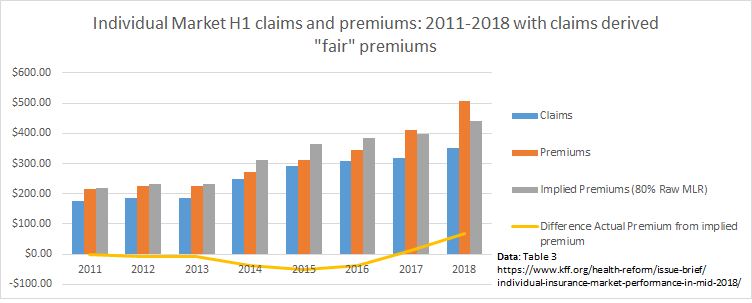

I’ve grabbed their Table 3 data for further analysis. This is a quick and dirty analysis with algebra as my only analytical tool. This is limited in that we should expect claims payable in the 1st half of the year to be lower than claims payable in the second half due at least out of pocket exhaustion. But this gets us in the general area.

All I am doing is taking the paid claims and multiplying that by 1.25 to get to a premium level which supports precisely an 80% raw MLR. I then subtract the average premium collected minus the implied premium level. Ideally at the end of the year, the difference should be zero or slightly negative (implying a higher actual MLR than the bare minimum). As the rest of the year continues to pay out, we will see the implied premiums get larger as claims will increase at the end of the year.

In 2011-2013, the difference at the mid-year is slightly beneath zero. 2014-2016 the premiums were too low while in 2017 (10% to 16% too low). In 2017 the actual premiums were 3% above the implied premiums. In 2018, the actual premiums are about 13% above the implied premiums.

These numbers will change in the 3rd and 4th quarter. But the basic trend is the key insight. 2017 was probably priced close to right where well run insurers could be profitable especially if they could squeeze their admin costs while 2018 has seen significant overpricing of premiums.

TKinNC

My 2019 premiums (59 & 58 year old) are $300 less per month than my 2018 premiums (58 & 57 year old) — I think they did overprice 2018 and it looks like they think so too. We are going to have to switch primary care provider though but that does not really bother me. We are low utilization folks … and I hope we can stay that way – especially since I’ve got a routine mammogram scheduled for later this week.

SOL (unsubsidized) PPACA marketplace customer. Person County NC

David Anderson

@TKinNC: Good to hear that your premiums are coming down (look around a bit before you renew as I think there might be some new options in your county)

burnspbesq

If they overcharged for 2018, won’t they have to make big-ass MLR rebates next year?

Origuy

Say, David, do you have any thoughts on California Proposition 8? It would limit the profits made by dialysis clinics. I’m all for controlling medical costs, but not a big fan of legislating by referendum. It usually leads to bad law.

Ballotpedia

David Anderson

@burnspbesq: MLR is a 3 year rolling look-back. 2019 MLR rebate checks are based on high MLR 2016, typical MLR 2017 and low MLR 2018. I expect to see significant MLR rebates in North Carolina and several other states that have monopolistic markets in most/all of the state. In regions with competitive markets, I am less confident that a one year MLR spike will lead to rebates.

David Anderson

@Origuy: I don’t know enough to have a reasonable opinion.

Origuy

@David Anderson: Neither do most California voters, I’m sure.

David Anderson

@Origuy: details details

Miss Bianca

When does open enrollment start for state-sponsored plans, btw? Isn’t it sometime in October?

David Anderson

@Miss Bianca: Post on this later in the week–

For ACA individual market plans, California opens up on October 15; Healthcare.gov on November 1,

Medicare/Medicare Advantage October 15

Employer Sponsored Insurance: Whenever the people in charge want it to be

Mike

The underpricing in 2014-2016 is somewhat overstated. Per the KFF analysis, they exclude transitional reinsurance from the claims. But insurers priced lower in anticipation of those funds. Even if insurers predicted costs perfectly in their rates, the KFF analysis would show 2014-2016 as “underpriced”.