“Premiums are going up 3% next year…”

“Rate increases are projected to be 7% higher….”

“Maryland expects premiums to drop…”

Those are common headlines for ACA plans. Those will be even more common headlines in the next couple of weeks as states finalize rates and insurers sign their 2019 Exchange contracts. These headlines try to roughly compare like to like with weighed averages of enrollment by metal type and/or insurer. There is a sloppiness in the language though. Most of these headlines and analysis look at a protoypical buyer of a constant age. I’m guilty of this.

Let’s assume that an unsubsidized buyer is 38 years old in 2018 and their birthday is on New Years Day. Let’s assume that they have a plan that the headline says will have no premium change at all. Is that their lived experience when they look at their proposed charges for January 2019?

No!

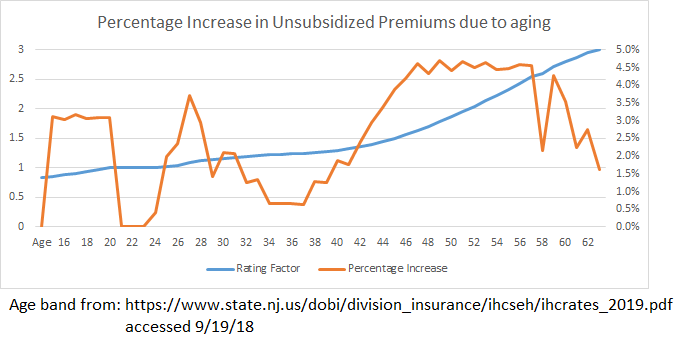

The premiums are set on a 3:1 age band (except New York and Vermont that use pure community rating) which means the premiums for a 64 year old can be no more than 3 times greater than the premiums for a 21 year old. Using the New Jersey release, I’ve built out a graph of the age factor (the blue line) and the annual percentage change in premium due to aging.

Almost every year after your mid-20s, there is a 1% to 4% increase in an unsubsidized buyer’s premiums just because they had a birthday. It is not a smooth curve with a constant increase. There are peaks and valleys with some hard spikes.

Almost every year after your mid-20s, there is a 1% to 4% increase in an unsubsidized buyer’s premiums just because they had a birthday. It is not a smooth curve with a constant increase. There are peaks and valleys with some hard spikes.

So when we use the language that premiums are increasing by 3% for a standardized population, we are assuming that everyone who buys insurance is a vampire who does not age. That is ridiculous as the lived experience is that non-subsidized buyers are seeing a couple percentage points of a price increase just because they age and this premium increase is independent of everything else that is going on with pricing.

So let’s talk about people instead of vampires.

p.a.

I find the yoot spike interesting; good health vs the ‘hold my brewski’ function. I thought the spike would be even higher.

Luthe

@p.a.: It looks like the spike correlates to age 26, aka the year kids age off their parents’ plan and have to get their own.

Mart

I don’t think you are being fair to vampires. Vampires were people too.

Martin

David, curious on your take here:

Somewhat different market, but this strikes me as a potential watershed moment from the traditional predictive actuarial modeling to something quite new. Interactive policies aren’t entirely new, but moving solely to them is kind of a big deal. On one hand I’m not exactly enthusiastic about the idea of lojacking the entire population, but when I step back and think about the job that insurance is there to provide, my objections fade away. Right now you have a serious information asymmetry with that actuary. They believe they know what your risk factors are (and charge you for them, even when they’re wrong) but you don’t necessarily do. Pricing is always a signaling function, yet it doesn’t really work in this case. Is my policy more expensive than other 50 year old males like myself? I have no idea, really, and I have no idea what I could do to lower that price. If I was told that if I lower my blood pressure my rate would go down, that would probably be enough to get me to do it. A lot of people are very good at responding to that kind of pricing signaling, in ways that they aren’t with other types of signals.

For the record, this is a place where single payer needs to be well thought out. One reason why I’m inherently a capitalist is that pricing is the most reliable signaling and throttling mechanism we have. The former is mostly because that’s what capitalism trains us to do, but the latter isn’t. There really aren’t good mechanisms for how to govern supply of a non-priced good, which is why central planning is so difficult. The VA is struggling with this right now. So under a single payer model, where there is no pricing signaling, you lose some of the ability to motivate individuals to better outcomes. Smoking has been addressed through both pricing signaling (more expensive policies for smokers) and through social signaling – banning smoking from public places, ads, general stigma attached to the act. Those do work but I’m not sure they’re kinder to the public than pricing, and does the government do these things when they’re the only ones running the show. Government’s track record on this is pretty spotty – see the work requirements for Medicaid, or the drug testing in Florida for public assistance recipients. I still believe that single payer is inevitable, but I do worry about how the benefits that a competitive marketplace can bring would be replicated.

ProfDamatu

@Martin: This is a very interesting argument, but IMHO it can only take us so far when it comes to health care. Just to take a very small example – all of the “price signaling” in the world would not have convinced my BRCA2 mutation to go away, and there is nothing at all that I could have done to eliminate that risk factor to potentially reduce insurance costs (as it is, there’s no life insurer in the world that would be willing to take me for any price). Sure, I do everything “right” to reduce my risk – exercise, stay at a healthy weight, eat well – but all of those things barely make a dent in the increased risk associated with the mutation. I realize that if we’re going strictly free market, the answer to people like me is, “that’s too bad – you’re just more expensive; no one said life was fair,” but if we’re talking about holding costs down for the whole system, price signaling like that isn’t going to make as much of a dent as one might hope, because there are so many expensive illnesses that are completely immune to that mechanism.

I dunno, I guess it just raises my hackles when we start discussing motivating individuals to better outcomes, as you put it. (This is at least partly due to my own medical history – I’m the poster child for “eat right, exercise, don’t smoke, barely drink…and still get cancer twice by age 40.”) Like I said, there are just so many illnesses for which there aren’t any reliable risk factors (like my lymphoma) – at least none that people can actually do anything about (e.g., for many illnesses the main risk factors are age and sex…); on top of that, where we do have modifiable risk factors, the correlation between those factors and developing the illness is far from perfect – in some cases, we don’t even know for certain if there is causation, or which direction the causation goes! (This is not the case for smoking.)

Also, my understanding is that wellness programs that are at least superficially like the one you mention (except that the carrot being offered was reduced health insurance premiums) haven’t been shown to work very well in terms of motivating people to do the kinds of things that would improve their health, at least not in the long term.

Luthe

@ProfDamatu: Yeah, and there’s the question of how far into your medical history they will dig. My family has a history of high cholesterol even when we eat right and exercise. Will the insurance company insist I take statins to treat it? If so, are they paying for them?

Also, there are socio-economic issues at play. If you work at a call center 40 hours a week for $12/hr and can’t afford to eat healthy plus have an hour-long commute, how can you meet the diet and exercise requirements?

Like everything else, this plan will boost the corporate bottom line while screwing everyone else.

David Anderson

@Martin: I am very curious if the “wearables” features is merely a cream skimming mechanism much like the actual impact of the wellness programs for healthcare. People who are willing to use wearables are likely to have underlying characteristics/endowments that lead to lower predicted mortality so it is not the wearables and the data produced per se driving mortality down but they are a marker of the underlying characteristics of a sub-population with low mortality even if they were never given a Fitbit.