The Center for Medicare and Medicaid Services (CMS) recently released new guidance on how they will process individual mandate exemption requests for 2018. The short version is that CMS will ask for almost no verification on anything that it is allowed to grant on its own authority. This is consistent with the January 20, 2017 executive order:

yes individual mandate exemptions will be passed out like pacifiers at a rave

— David Anderson (@bjdickmayhew) January 21, 2017

My question is how will CMS handle prospective mandate exemptions for 2019? This is an esoteric question with significant relevance because this will determine the size of the Catastrophic risk pool.

Catastrophic plans are very high deductible plans with minimal services pre-deductible (3 PCP visits and no-cost sharing preventive health services). They are similar in benefit design to the skimpiest Bronze plan. Catastrophic plans are not eligible for subsidies. Catastrophic plans tend to have lower premiums than Bronze plans. For example in New Jersey, the least expensive Catastrophic plan is priced 26% less than the least expensive Bronze plan for the 2019 plan year.

Catastrophic plans are available to two classes of buyers. The first is age restricted — anyone under the age of 30 can buy a Catastrophic plan with no questions asked. The second class are people who qualify for a hardship exemption. Some exemptions are based on affordability of plans and life circumstances. CMS added two new exemptions where anyone living in a single insurer county qualifies as well as people who live in counties where all plans offer abortion coverage.

There has been significant interest on Capital Hill in both the form of Alexander-Murray and HR6311 to expand access to Catastrophic/Copper plans. Those plans were unworkable, but depending on how CMS handles prospective hardship exemptions for 2019, this policy goal can be achieved:

If policy makers are determined to use benefit design and eligibility criteria modifications as a mechanism to offer more people lower premium plans they have two realistic choices.

The first is to offer catastrophic plans to more people while maintaining separate risk pools. These plans would be attractive to some of the non-subsidized bronze buyers who currently do not qualify for catastrophic plans. Current bronze buyers who switch would be better off even as current catastrophic buyers would face higher premiums as an older group of buyers enters their pool. Current silver, gold, and platinum buyers would see premiums increase as plans would receive less risk-adjustment transfers to cover their claims…

If CMS will be passing out prospective hardship exemptions for the 2019 open enrollment like spectators pass out water at the bottom of Heartbreak Hill, then we should expect the Catastrophic pool to widen. Sophisticated non-subsidized shoppers or their insurance agents will file requests for exemptions from the $0 2019 mandate in order to access lower cost catastrophic plans. More subtly, some very sick non-subsidized buyers may shift from the metal pool to the Catastrophic pool.

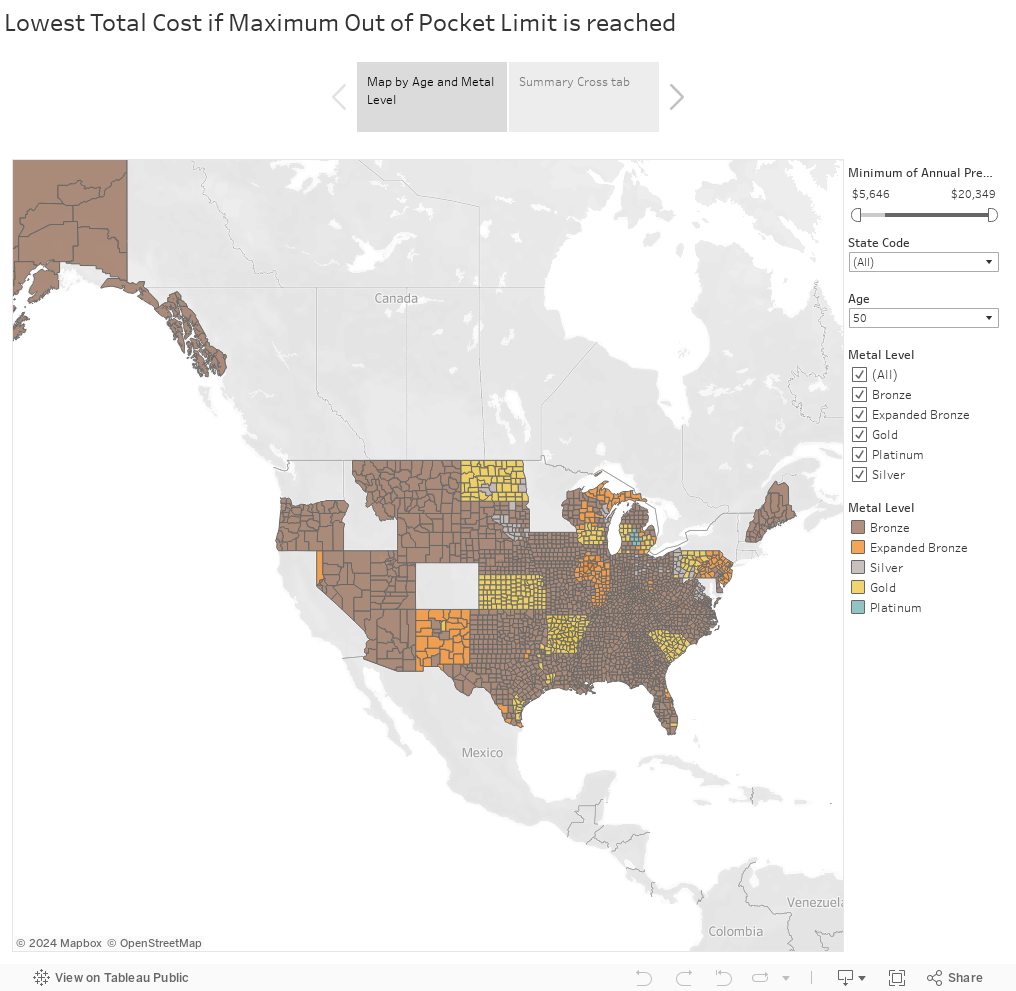

We have seen that for non-subsidized individuals who know that they will easily and certainly meet their out of pocket maximum that the plan with the least total expense can often be a Bronze plan (2018 map below the fold). If the premium differential is sufficiently large, Catastrophic plans may be more cost efficienct than Bronze plans for these individuals. This was the case in 2018 but the universe of Catastrophic buyers was very small (~1% of on-exchange buyers). If the Catastrophic universe is larger in 2019 and 2020, then we should expect more high morbidity non-subsidized folks to leave the metal pool and enter the Catastrophic pool which will play merry hell with risk adjustment but that is a minor issue.

So they key question is how will CMS treat prospective mandate exemption requests for 2019 and will the broker and assistance community shift significant tranches of more morbid people into Catastrophic plans if prospective mandate exemptions are readily granted?

StringOnAStick

Wait, if higher morbidity people are going into these catastrophic plans, aren’t they likely to end up hitting the maximum coverage limits on these plans pretty quickly since they don’t cover much and are capped? Is the idea that once they hit there, they will fall into Medicaid, or just fall off the radar, problem “solved”? I suppose if the goal is to crash Medicaid or lead to it becoming very unpopular to fund at the state level, plus jack up the metal rates so they also become unpopular, then mission accomplished I guess? It looks like they finally brought in someone who actually understands how the ACA works and are now doing a much better job of killing it by a thousand cuts.

Mart

MO Senator Claire McCasskill drives me nuts with the center right Dem act she thinks she needs to play to stay elected here. Her campaign has started running ads against her opponent for him joining the lawsuit to get rid of pre-existing conditions. I found the ad to be effective and a good move on her part (for once).

StringOnAStick

@Mart: That’s an excellent move, because everyone is pissed about getting rid of guaranteed coverage for pre-existing conditions. Uncertainty about that is why my husband and I can’t drop back to part time work since we both have them at age 60 (who doesn’t by our age?). Agent Orange totally screwed our early retirement plans.

David Anderson

@StringOnAStick:

Assume a person with CLL who has a $100,000+ year no matter what. They have an objective function, constrained by network, to minimize sum of premium and Out of Pocket costs.

A high oop + low premium can be a good solution to that problem

StringOnAStickS

@David Anderson: We could do that but until the republicans don’t control every branch of government, it’s a scary choice to make right now .