At the Health Affairs Blog, Andrew Sprung and I try to figure out the differential impact of Silver-Loading Cost Sharing Reduction (CSR) costs into premiums and messaging/outreach environment on enrollment. We find a couple of different things.

- Enrollment gains due to Silver Loading is a 200-400% Federal Poverty Level (FPL) event

- Aggressive and well funded outreach with advertising, navigators, and positive strategic messaging probably leads to a ~6% gain in enrollment at all subsidy eligible income levels (100%-400% FPL) compared to outreach activities in Healthcare.gov states.

We use Covered California as a quasi-control group assuming that it is near the frontier of active outreach and positive enrollment activities.

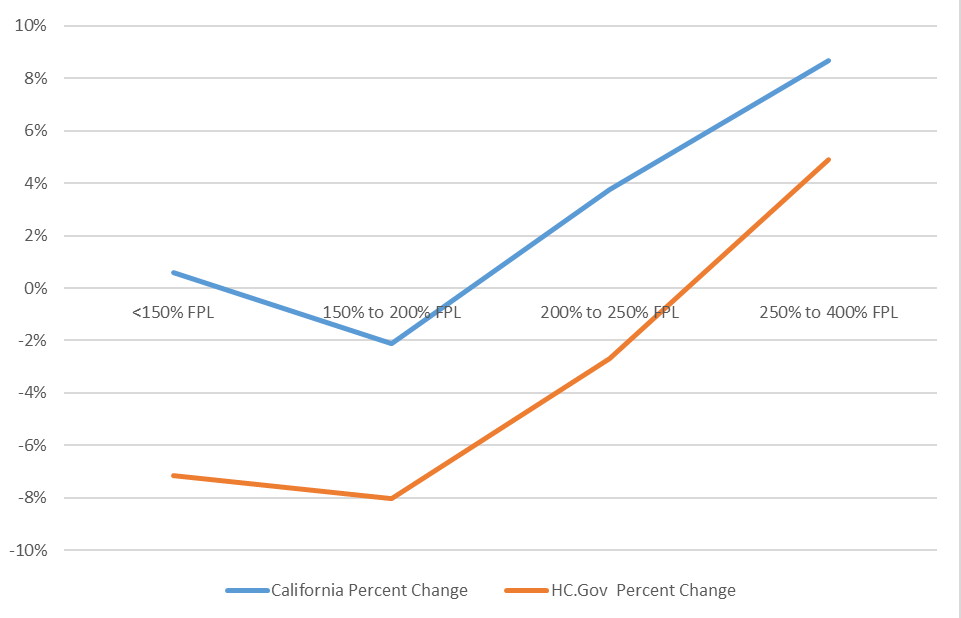

Image 2 tells the story. The vertical axis is the percent change in enrollment 2018 from 2017. The horizontal axis is the income category.

We assume that Silver Loading CSR really only changes the choice incentives for people who either don’t qualify for CSR (251%-400% FPL) or weak CSR (201-250% FPL). Someone making 148% FPL in California or Oklahoma or Wyoming or Pennsylvania will qualify for a CSR 94% AV Silver plan for $61 or less per month depending on the local Silver spread. That plan will have very low deductibles and a low out of pocket maximum. There may be lower premium Gold plans with much higher deductibles and no-premium Bronze plans with deductibles equal to four months of pay. Most folks who qualified for strong CSR stayed with Silver plans. They faced no major changes in their pricing incentives year over year.

Folks earning between 201%-400% FPL are the people who saw their pricing structures change dramatically. Gold plans may have lower net of subsidy premiums than CSR Silver plans and Gold plans will tend to have lower deductibles and out of pocket maximums than CSR Silver plans at this income level. Bronze plans can be very low premium which could be attractive for likely to be healthy individuals in this income bracket.

The most interesting thing to me in the exhibit is the near parallel trend between California and HC.Gov states for enrollment changes by income group. I’ll let the econometricians fight but to me that constant space is roughly equal to the messaging and outreach changes.

Yutsano

I don’t know about everyone else but on Firefox the image isn’t loading.

Steeplejack

@Yutsano:

Doesn’t load for me either. (Desktop site, Win10, Firefox.)

Spanky

Won’t load in IE either. Bet if Chrome were on this work computer that it wouldn’t load it.

p.a.

Android Chrome: nuttin’

David Anderson

I’ve updated the image to embedding it directly instead of linking to the Health Affairs server

Yutsano

@David Anderson: Got it now, thanks. This is really telling me that a state that really tries to make ACA work gets better results. Amazing how that works…

greengoblin

We would all be better off if the country was run more like California.

Alain the site fixer

Test from Edge

Alain the site fixer

another test

Alain the site fixer

@Alain the site fixer: I’ll be back

Duane

@greengoblin: I’m tired of insurance being complicated. It’s a constant battle to find, keep and use insurance. Then you have. Medicaid, a system that should be straightforward, but people like John Roberts and Asa Hutchinson want to destroy it instead. Health insurance should not be so damned difficult.

J R in WV

@Yutsano:

It loaded for me at 11:36, current version Firefox on a Linux laptop running 14.04, also pretty current.

Dave, I see people complaining that their private employer-based insurance is beginning to suck and cost more. Do the rules about ACA insurance plans also apply to private insurance — like the 80%/20% payout versus profit retained rule, breadth of coverage, etc?

Duane

@J R in WV: That’s what I mean about insurance being too complicated. A simple question like that and it requires a health insurance expert to get a answer.

J R in WV

@Duane:

Not only insurance. Medical care is as opaque as the nuclear weapons program! You can’t discover the price of anything in advance, from simple things like – well any simple thing, to a 59 day stay with a month in ICU.

They can’t tell how much your joint replacement will cost, which is something they do 30 times a day in many hospitals. They can’t tell you how much your share will be, regardless of how common your coverage is, like Medicare and the local state insurance supplemental, which a hundred thousand people have here locally.

Simple diagnostic X-ray? We don’t know how much it costs, we just know how to perform the X-ray… your doctor doesn’t know how much anything costs. He can not advise you as to how much his recommended course of action for a medical issue will cost, whether one facility is less expensive than another, Nada! It Can’t Be Done!!

This is not how it is supposed to work!!! That isn’t a marketplace at all~!!~