CMS just announced that it had approved Maine’s 1332 waiver application to run a reinsurance program. This is not surprising as CMS is gung-ho about reinsurance. It happen a week or two earlier than I thought but this is good news, CMS will process reinsurance waivers very quickly.

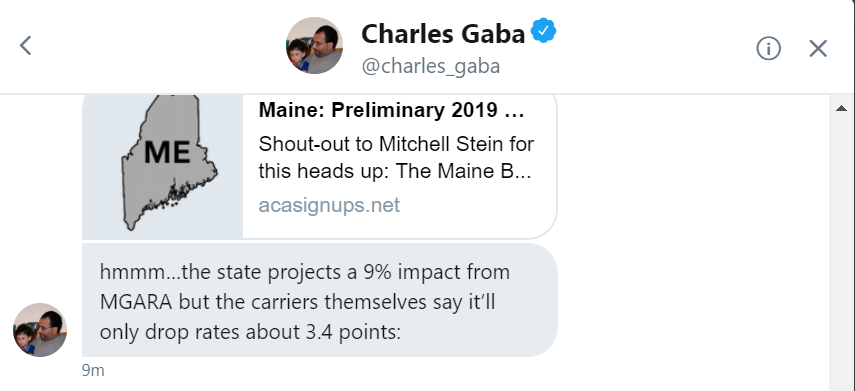

I was chatting with Charles Gaba. He noticed something odd about the waiver. The state’s actuarial models expect reinsurance to do a lot more in lowering rates than the insurers. There is nothing wrong with discrepancies, different models with different weights should produce different results.

Insurers are making informed guesses as to the effect reinsurance will have on their rates. Their guesses will be wrong. It matters in what direction the guesses are wrong though. If insurers think that reinsurance is super-duper wonderful and drop their rates far below what the actual claims experience is, they lose a ton of money and the C-level may not be employed. If insurers price their products on the assumption that reinsurance won’t do much, they are profitable. I think the incentives line up for insurers to try to price their products as accurately as possible with a bias towards thinking that reinsurance won’t be kittens and rainbows.

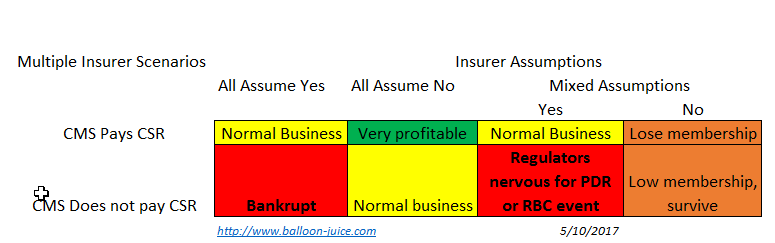

I used similar logic in thinking through CSR assumptions in the Spring 2017:

Now the interesting, to me part, is that Medical Loss Ratio (MLR) acts as an awkward one way risk corridor for mis-pricing reinsurance. If insurers think that reinsurance won’t do much to eat high cost claims and thus price high, and then are wrong as reinsurance eats all the big claims, they have a windfall year. However MLR acts as a cap on the windfall. If an insurer spends less than 80% of its qualified revenue on claims, it sends out rebate checks to its buyers.

This is a one-way risk corridor where overly pessimistic actuarial error benefits the consumer via rebate checks. Overly optimistic actuarial error is borne completely by the insurer’s board and balance sheet.

So what does that mean?

I would not worry too much about the discrepancy between what a state regulator thinks reinsurance will do and what the insurers think it will do. If the insurers are wrong and price high, there is a limit to the windfall profits possible.

MomSense

The current state of our state is problematic and our DHHS/CDC is one of the worst run parts of our government. It’s a shame, too since it was one of the best before LePage.

TKinNC

Off-topic but insurance related so always on-topic for Mr Anderson.

Look what I found in my e-mail this morning –

What’s changing?

Blue Cross NC will not offer your Blue LocalSM with Duke Health and WakeMed health plan next year. Instead, we’ll move you into a new ACA health plan for 2019: Blue ValueSM with UNC Health Alliance. This plan will have similar benefits to your current health plan — but at a lower price. That means most members will see a lower monthly premium next year before any subsidies from the federal government are applied.

I hope they are correct and I am in the “most members” cohort because I’m currently paying $1620/month for two olds – 58 and 57.

Hmmm. I wonder if the new ACA marketplace insurance company is planning to offer coverage in Person County.

David Anderson

@TKinNC:

From what I have heard, UNCMed will still be in the Blue Local network for high end specialty care. There is a possibility of another insurer (Centene or Cigna) will pick up Duke for Wake/Durham county, it is unlikely that Duke will be in-network for plans sold in Person County

TKinNC

@David Anderson: So far, this actually works for us. Our favorite physician has left the local practice and this gives us a cover to change primary care and still maintain our Southren genteel manners. Nuthin personal, ya’ know.