Margot Sanger-Katz has an excellent rundown of all the ways that the Trump Administration is working to make the guarantee issued, community rated individual insurance markets of the ACA work less well or fail completely. She raises one point that I want to expand on:

The administration has left one more potential disruptive option on the table. Last year, when President Trump canceled a disputed set of payments to insurers, state insurance regulators allowed the health plans to shuffle around prices to absorb the loss. In a call with reporters Monday, Ms. Verma said her agency was considering barring that practice. Without the price adjustment, consumers in the Obamacare-compliant market will have a harder time finding an affordable plan.

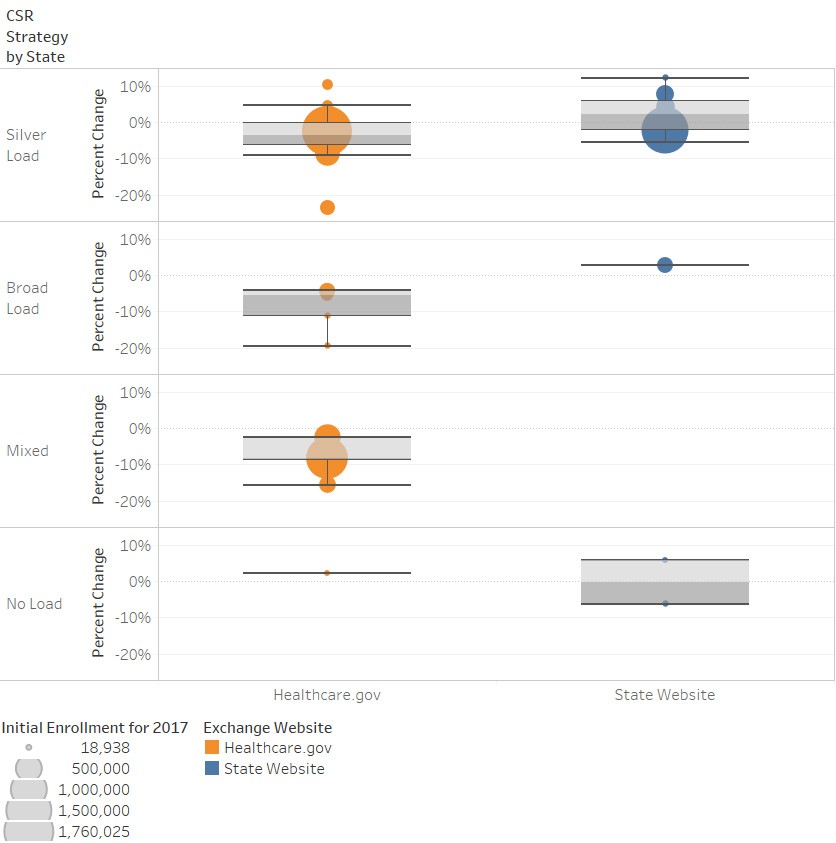

This is in reference to Silver Loading.

CMS can make a rational argument that loading CSR costs onto only Silver should not happen for public policy grounds. Silver Loading costs the federal budget serious money through much higher benchmark premiums and also higher enrollment because Bronze and Gold plans become comparatively much cheaper for subsidized buyers.

Silver loaded states tended to do better than other states on enrollment for the 2018 open enrollment.

There would be two major questions. First, what would the alternative be? And secondly how does that alternative play on the Off-Exchange only market?

The alternative would most likely be a Broad Load scenario. Last year, six states applied a uniform percentage surcharge to all plans. This meant that against a counterfactual of regular and ongoing payment of CSR, Bronze plans were less expensive than they would have been for subsidized individuals and Gold plans would be more expensive. If states that are currently using Silver Load strategies are forced to go to a Broad Load strategy, Gold plans become very expensive for subsidized buyers and Bronze plans are less likely to be zero premium plans after subsidies are applied. We should expect an additional 2% to 3% drop in enrollment from on-Exchange buyers in Healthcare.gov states due to this change.

The next question is how would this work off-Exchange? States that Silver Loaded in 2018 made sure that off-Exchange buyers who purchased Bronze or Gold plans were not touched by the CSR pricing shenanigans. Some states used Silver Switch strategies where near-clones of on-Exchange Silver plans were offered Off-Exchange without CSR being built into the pricing. This held the entire off-Exchange market harmless.

I think CMS has a harder public policy interest argument against banning off-Exchange only plans from not incorporating CSR costs into the plans as there is not billions of federal subsidies at stake. Off-Exchange plans by definition are unsubsidized. So if this assumption is right, then the off-Exchange market bifurcates completely into plans that are offered on and off-Exchange with a Broad CSR load built into all premiums and then off-Exchange only plans that have a significant pricing advantage.

Another Scott

(Your embedded image in this post has a broken linky.)

Cheers,

Scott.

StringOnAStick

The off-exchange market is what I’m trying to keep up on, since that is where my husband and I would have to buy health insurance if he becomes a contractor. Mango Moron getting elected put the kibosh on that plan since the obvious first move by him and the GOP co-conspirators was to kill Obamacare and obviously screw up pricing for the rest of the market in the process. Husband has settled for working part time so we keep benefits, though it is just one extra day off a week. He’s thrilled about that, but really wanted to go to 3 on, 4 off and only becoming a contractor would let him do that.

ProfDamatu

For the benefit of people whose states/carriers did Silver Load or Switcheroo, I hope that strategy doesn’t get banned, but I have to admit, even I can see why it might make sense on policy grounds to end it, at least with the current cast of characters in charge. Ending Silver Loading might cause a few percent of the on-Exchange market to become uninsured, but I worry that the ever-increasing APTC subsidies under that strategy might prompt the administration to try to stop paying those too…which would mean that almost everyone on the exchange would be unable to afford their insurance. I know they can’t cut off APTC unilaterally, but it would definitely be an easier argument to make as the subsidies continue to climb.

It’s also worth thinking about what the parameters of the various plans are. The one insurer in my city/county didn’t silver load, at least not in this area, which did indeed mean that Bronze plans were not zero-premium and the single Gold plan had a much higher premium than Silver. The Bronzes were about what you’d expect, but the Gold…I have to say, it was a struggle to figure out what made it a Gold plan. The OOP was the statutory maximum, the coinsurance was the same as the better Silver…really marginal differences like copay amounts was about it. I can’t imagine that for all but a tiny handful of people, the extra $350 or so per month in premium would be worth it. I’m just saying – especially in single-carrier scenarios, the lack of Silver loading may not make as much of a difference as you’d think, because the Gold plans sometimes stink or are barely better than Silver.

Jim

As Donald Trump has said, “Who knew health insurance could be so complicated?” :-)