Joshua Peck of Get America Covered is attempting to estimate a counterfactual of what enrollment would have been without Trump. I think this is a useful exercise, I have tried to build the same type of counterfactual. I think the number that he and his team use is too high.

Based on the evidence we have, without the Trump Administration’s efforts to undermine enrollment, national enrollment would have exceeded 12.9 million enrollments or roughly 1.1 million additional people would have enrolled.

There are a couple of major assumptions that I disagree with. The biggest are the impact of CSR and the impact of federally paid media. Before we go deeper, I want to outline what I think are the major drivers of enrollment changes.

- Enrollment in QHP is probably counter-cyclical as a better economy should lead to more people covered at work

- Medicaid expansion is a negative in Louisiana as eligible people are switching to Medicaid from QHP

- Overall messaging environment is a major negative

- Lack of federal outreach is a negative

- Increase in private outreach is a positive

- Insurers dropping out is a negative

- Terminating CSR is a positive

- Increased Silver Gapping is a positive

Peck acknowledges that CSR is a big deal:

Marketplace consumers saw lower net premiums this year than last year. For many Americans, prices were much lower than previous years due to the indirect effects of cutting payments for cost-sharing reductions aka “Silver Loading”. According to HealthSherpa, overall their consumers paid on average 13% less this year than last year.

But if we are trying to establish a counter-factual based on a universe where Hillary Clinton is President we need to back out CSR impacts. I don’t think it is a straight faced assumption to assume that a Clinton HHS would terminate CSR mid-year in order to encourage Silver Loading. If there is no Silver Loading, the only pricing advantage possible in 2018 compared to 2017 for subsidized buyers is via Silver Gapping. Insurers have been getting smarter about increasing the number of counties where there is a wider spread between the least expensive Silver and the benchmark Silver. Silver gapping was more common in 2017 than at any point before. I don’t think we can create a counter-factual with a better subsidized pricing environment than reality.

Insurers dropping out is a known negative. People get lost in the wash of auto-renewals and have price shocks and then messaging. I think we would have seen fewer insurers drop out in a Clinton administration than we actually did as there would have been less policy uncertainty, but we still would have seen insurers change their covered regions and leaving counties.

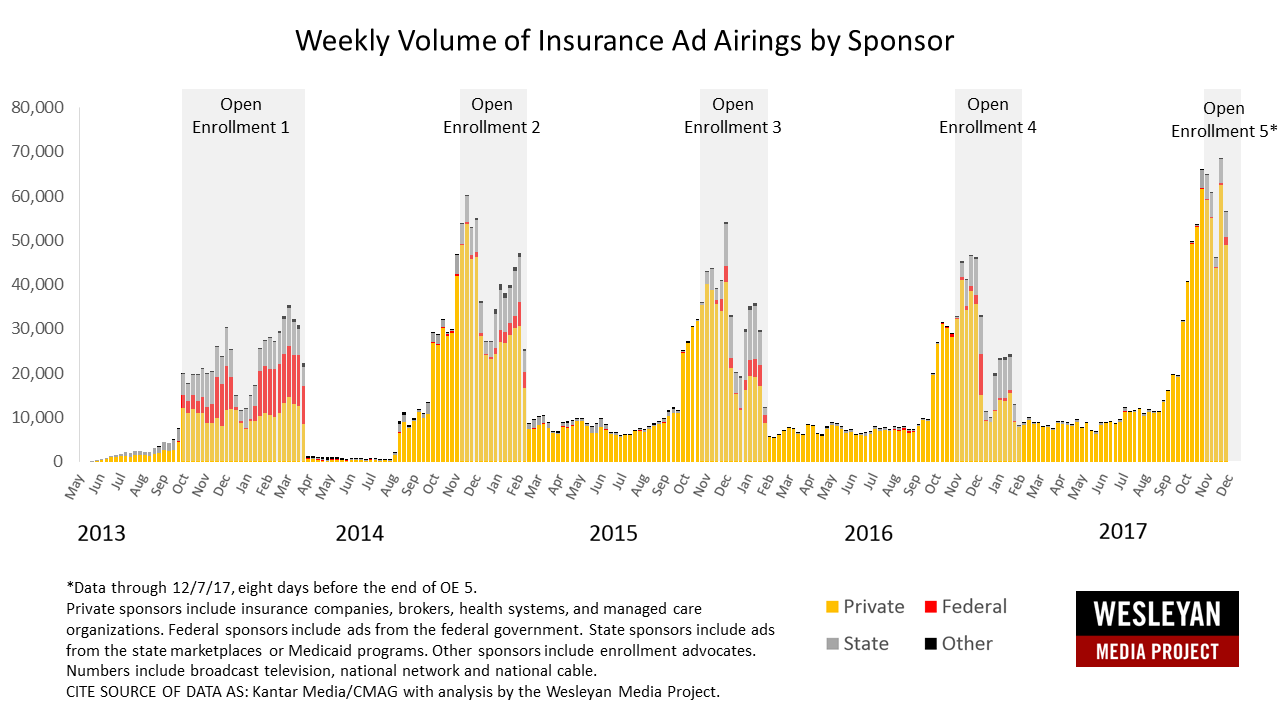

The next major areas that can drive changes in enrollment levels are messaging environments. I will start small. Healthcare.gov minimized their outreach. However, the Wesleyan Media Project shows that the private sector picked up the slack:

We also see total enrollment in California down by 2.3% compared to 2017 despite Covered California going all out on outreach and taking advantage of very aggressive Silver gapping and Silver loading.

The big counter-factual negative is the broader messaging environment. We know that the Trump executive order led to an immediate slow down in enrollment in the last eleven days of the 2017 Open Enrollment Period (OEP). Quick and dirty estimates have the enrollment loss at 4.29% while more sophisticated estimates have lower numbers for that immediate administration change period. People have been hearing for a year now that the ACA is dead and it is worthless. Marginal buyers aren’t following health insurance policy news closely and they’ve heard that the ACA won’t be around for long.

We have two other enrollment depressors that are constants across the actual and the counterfactual. The first is Louisiana had a mid-2016 Medicaid expansion where a lot of eligible people still signed up for ACA plans instead of Medicaid in 2017. Those people are switching over to Medicaid for this year. Next the unemployment rate is decreasing which means more people have jobs which means more people may have access to employer sponsored insurance. The individual market is counter-cyclical, we should expect, all else being equal, more enrollment in bad economic times and less enrollment in good economic times.

The big net depressor of enrollment for 2018 to 2017 in my opinion is the general messaging environment. A lot of other things seem to wash out. In the counterfactual universe, subsidized pricing is no better and most likely significantly worse in many counties. Advertising is just being sourced differently and fewer insurers were leaving the market.

I don’t think 12.9 million potential enrollments in the counterfactual is a reasonable estimate. I think a number that is closer to 12.4 or 12.5 million potential enrollments is probably a more defensible counterfactual.

MomSense

I was hoping we could build on the outreach with a Clinton administration. There are so many people in rural areas who are older, either without internet or without the ability to use it effectively, who have limited transportation options, and limited cell plans. We honestly need navigators with tablets who can go to people to sign them up.