Pennsylvania released their 2018 ACA rates on Monday afternoon. Their data is here (XLSM file) and the press release is here. They are explicitly Silver Switching the entire state to accommodate the CSR cut-off.

Because cost-sharing reductions are only available on silver plans, rate increases necessitated by the non-payment of these cost-reductions will be limited to silver plans. On-exchange bronze, gold, and platinum plans and off-exchange silver plans will not be impacted by these disproportionate increases.

Premium subsidies are calculated based on the cost of silver plans in each rating area, and subsidies increase in connection with rate increases. Because rates are rising on silver plans due to cost-sharing reduction non-payment, premium subsidies may be generous enough to allow an individual who qualifies to purchase a gold-level plan that has more favorable cost-sharing at a lower price than previous years.

Acting Commissioner Altman strongly encouraged individuals who do not qualify for premium subsidies to consider off-exchange options. The department worked with each of Pennsylvania’s five marketplace health insurers to ensure they would offer an off-exchange only option that is not impacted by the disproportionate rate increases for on-exchange silver plans. Off-exchange plans must be purchased directly through one of Pennsylvania’s five marketplace insurers or through an agent or broker licensed by the department to sell on behalf of these companies.

This is a really good short explainer of how people should shop in 2018. If you make more than 400% FPL, don’t even look at the exchanges. Use a broker or go direct to the websites of the insurers in your county and buy directly from them. If you make between 200% and 400% FPL, take a very hard look at Gold plans. In most counties, there will be at least one Gold plan that is less expensive than the Benchmark Silver plan.

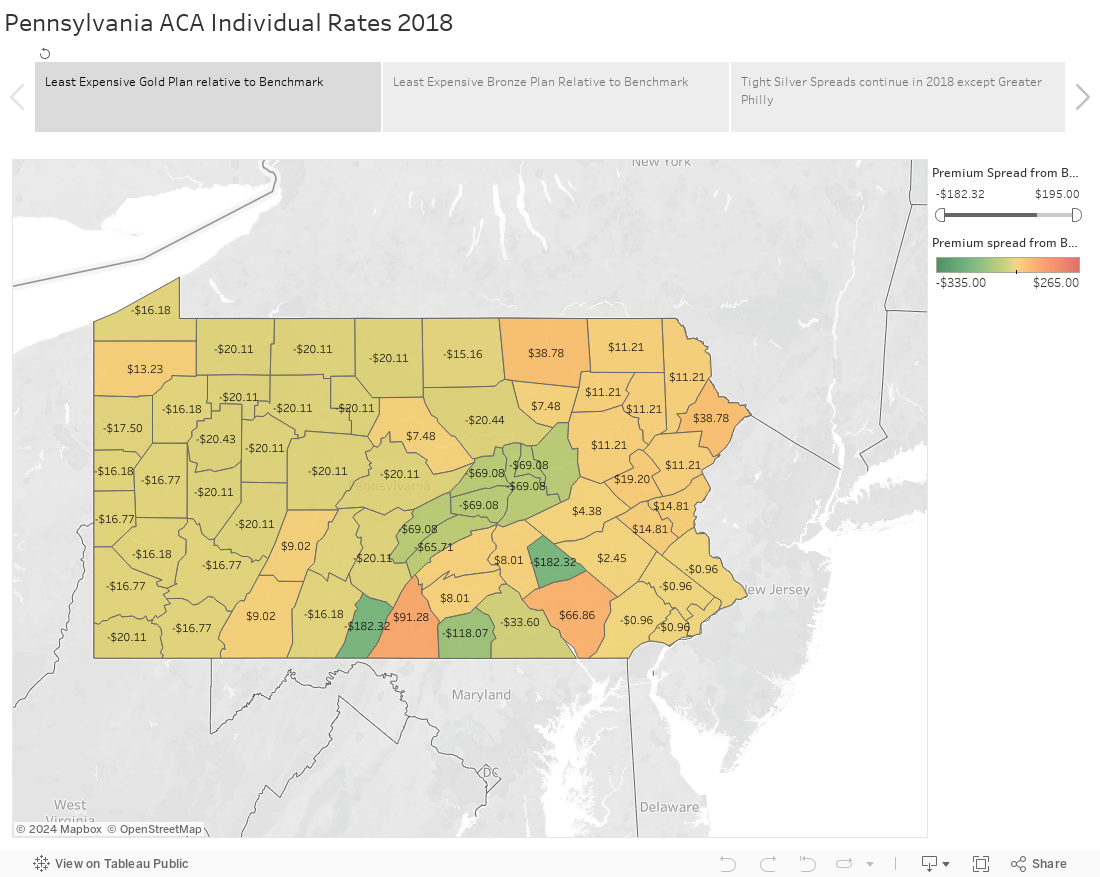

Below is a Tableau that has most of the details of the entire Pennsylvania insurance market. My data is here as a .txt file. I started with the state data, stripped out the small group plan-county combinations. After that, I identified the APTC eligible plans. From there, I flagged the county level benchmark. I then calculated the distance from each plan-county combination from the benchmark plan for that county. A negative number means that Plan X is cheaper than the benchmark. All premiums are based on a 21 year old non-smoker who does not receive a subsidy. As people get older and families get larger, the spreads between Plan X and the benchmark will increase by a fixed ratio.

I have a few observations below the fold.

I am somewhat surprised that not every county had a Gold plan less expensive than the benchmark Silver. Most of the are north and west of the Turnpike and east of I-99 fit this criteria.

Fewer plans seem to be offered by most insurers. With the exception of my former employer of UPMC Health Plan, insurers are only offering a handful of plan designs per metal band per county. UPMC still Silver spams Allegheny County with 15 different Silver plans. Their product offering is based on three distinct networks (very narrow, narrow, broad) and then five replicated benefit designs. They will file every product type in every county where a network is adequate to sell. UPMC has minimal competition in Western Pennsylvania outside of the core Pittsburgh metro area but they keep tight Silver spreads in their monopoly counties. I think this is a mistake

There are some incredible deals for Gold and Bronze plans Fulton, Lancaster and Adams Counties. Geissenger and Capital BCBS have an interesting dynamic where they each offered a single plan in each metal level but Geissenger is at an incredibly low price point in these counties.

For an enterprising reporter, there is one hell of a story to be found in late November if you interview subsidized buyers in Adams and Fulton County and then talk to similar people in Franklin County. You should also have the same conversations in Lebanon and Lancaster Counties. The ACA is always a county by county story.

Frank McCormick

What happened to Philadelphia and its collar counties? (I’m from Chester County )

Spanky

Thanks Richard. Living in MD but having grown up in Allegheny County I’ve been mulling a move back to PA post-retirement. I’m paying attention here not for the direct impact, which post-age 65 would be nil, but what changes to the whole health system will happen post-ObamaCare. I’m not finding a whole lot of reasons to move at this point.

ETA: I’m not looking exclusively at Allegheny County, but, you know, Philadelphia, Pittsburgh, and Alabama in between.

Spanky

Also too, I just came over from the Post-Gazette:

ETA:

I need to embed a couple of graphs from the article:

Kind of reduces the impact of that headline, doesn’t it?

David Anderson

@Frank McCormick: Philadelphia and the Main Line Counties are all served by a single on-Exchange insurer, Independence Blue Cross. IBC decided to aggressively gap by offering an expensive Silver plan via one of their subsidiaries and an inexpensive Silver through another subsidiary.

David Anderson

@Spanky: I have a lot of sympathy for local reporters trying to get this right as it is counter-intuitive and confusing. The national reporters were iffy for most of the weekend and started to figure things out on Sunday afternoon/Monday

satby

It’s insane that your heath care costs and access vary so much by county.

Barbara

@Spanky: I also grew up in Allegheny County and my mother still lives there (as well as one of my siblings). The Post-Gazette isn’t usually that retrograde with headlines. I thought of moving back too, as my mother is the only living parent for both me and my husband. I can’t quite pull the trigger.

Jerry

Do you think this bit of advice would apply to North Carolina residents as well?

Spanky

@Barbara: I have a few cousins there, and that’s it, so no real pull. Then again, my wife had a two-week work assignment in the North Hills a few years ago. In January. And loved it there! And she’s from Southern VA. She wouldn’t mind the move. It just seems like a retrograde move for me, though.

David Anderson

@Jerry: Pretty much in all states shopping on the Exchange when you are not subsidy qualified is a major gamble. It is easier presentation but given the Silver strangeness that ease could cost you serious money.

MobiusKlein

Seems a terrible hack, going thru the trouble to set up exchanges to help compare different plans on an even basis, then trashing the whole thing.

We were supposed to have a marketplace, not a bazaar.

rikyrah

thanks for the information, Mayhew.

StringOnAStick

@David Anderson: Major gamble is right, and in many ways. My husband had planned on quitting and becoming a contractor for his company this coming January, and then the orange fart cloud was elected and we worried that the 5 years we’d need to buy our own insurance would be an issue. Then my husband was diagnosed with a chronic leukemia that likely won’t affect him until he’s a least a decade into Medicare, but with no idea about how pre existing conditions will be treated (though probably at great cost) we feel like the gamble is too great. How can we be sure pre existing conditions won’t suddenly become impossible to buy insurance for this year; how about in 2, 3 or more years? What if they succeed in pushing Medicare enrollment out to 67 or more?

Here we are just about to hit 60 and with enough saved to semi-retire early, my husband is burned out at his job and having watched his only sibling die last year so he wants more free time now, but the chaos in health insurance means job- and situation-lock. Thanks, Vlad and all you R voting morons.

Barbara

@Spanky: Well, if you haven’t been recently you could go for a long weekend. It’s not the same city you grew up in. My problem is that I really liked the city I grew up in, even though I do appreciate many of the changes, most of which make it more like the place I have been living in for just about my entire adult life.

David Anderson

@Barbara: That is a really good description of the changes of the East End in Pittsburgh….

Rick Gundlach

David,

As to counties like Lancaster, Highmark said in a filing that they were dropping certain on-exchange Silvers if Trump eliminated the CSRs. Page 5 of the below PDF.

http://www.insurance.pa.gov/Consumers/HealthInsuranceFilings/Documents/2018%20ACA/HHIC%20IND%20HGHM-131020572%20-%20Final.pdf

If neither of these Silvers is offered by Highmark, the benchmark second-lowest changes, and the amount of Premium Tax Credit available rises substantially, maybe sufficient enough to make a Gold Plan competitive for those above 250% FPL. And a Bronze Plan almost cost-free net of Premium Tax Credit.