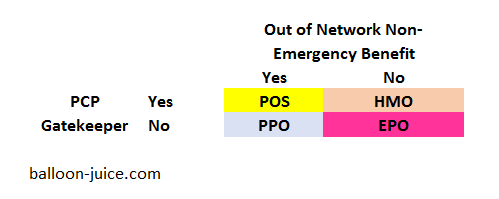

There are four basic plan design types. They are based on two elements. Is there a Primary Care Provider (PCP) gatekeeper requirement? Is there an out of network benefit for non-emergency changes?

That is it. There is nothing inherent to a Preferred Provider Organization (PPO) that makes it immediately superior to an Health Management Organization (HMO) or an Exclusive Provider Organization (EPO) plan design. Plan type does not drive network. So when you have to choose a plan during open enrollment, don’t automatically choose a PPO until you look at the trade-offs.

If we hold everything else equal, PPO plans will be more expensive than anything else. They are the most permissive. They don’t require referrals from PCPs for services, and they will give some money to any provider anywhere in the country when they perform a service. There is a lot of leakage from the contracted network.

EPO’s don’t pay out of network benefits. They also don’t require primary care referrals for in-network specialists. They tend to be a middle ground on the hassle factor. HMO and Point of Service (POS) plans require PCP referrals for complex and specialty care. Some plans will have stringent gatekeeper requirements. Other insurers will have loose requirements. That will vary. HMO plans will not pay non-emergency out of network benefits. POS plans will pay out of network charges to some degree.

Network size is independent of plan type. Some HMO networks are massive and some PPO networks are tiny. Some insurers will have one basic network that they use for multiple plan types. It will all vary.

The top 20 plans in the country according to NCQA in 2015 were a mix of plan types. Not all PPOs are great, not all HMO’s are bad.

When you are choosing your plan during open enrollment, please be ready to think through the trade-offs.

satby

Thanks David.

This is helpful, but I expect to be priced out of the market this coming year without CSRs. So I have started to look at becoming a medical refugee expatriate, at least until I can get Medicare. Assuming that’s not gutted in the next two and a half years. I don’t have serious health issues now, but untreated asthma has a tendency to cause problems down the line.

David Anderson

@satby: e-mail me and let’s figure out what can be done.

satby

@David Anderson: you’re a good guy, David.

Brian Pierce MD

One fledgling innovation in primary care, Direct Primary Care, is offered by about 1000 independent physicians and several large chains such as Iora and R-Health offers affordable primary care (typically $50-75/month). While DPC offers better access in and out of the office, longer visits when needed, help with lower cost tests, meds, surgeries, etc.

However, HMO patients find themselves facing big financial penalties if they use a primary care physician that is outside their HMO’s panel. Patients lucky enough to have or live near a DPC practice ( https://www.dpcfrontier.com/ ) should consider a PPO plan and avoid HMOs including HMO Medicare Advantage plans.

David Fud

If one is a consistent reader of yours but is unlearned otherwise about health insurance and our health care system, who else would you recommend reading to round out our understanding?

Thanks for this post. Very interesting.

David Anderson

@David Fud: Louise Norris

stinger

Bookmarked. Thank you, David!

Raven Onthill

Thank you. That makes it very clear. My one comment on this is that HMOs give a single doctor an enormous amount of power over one’s care. Combined with already overinflated medical egos, this life-or-death power can be drastically abused and there is usually an incentive to deny care. (I have a friend whose symptoms were dismissed and a large and inoperable tumor pancreatic was allowed to grow until she finally had a medical emergency and she was diagnosed because of a referral from the ER. She may survive.) The ability to make one’s own choices about what is a significant health problem is important.

satby

@Brian Pierce MD: wow, one of those is right nearby, and membership is $29/ month. Thanks!

David Anderson

@Raven Onthill: Raven — that type of strong gate keeping incentive varies by insurer. At UPMC, where I used to work, the HMO gatekeeping aspect was extremely light. Other HMOs had strong gatekeepers. It varies a lot.

martian

@David Anderson: Is there a way to know or figure out which insurers have a strong gatekeeper vs. a light one before signing on and experiencing it directly?

MTmofo

This is new.

https://twitter.com/K_Hought/status/920006252670861313

ProfDamatu

@martian: Sometimes that info will be in the plan disclosures – for instance, in my plan documents for this year, it’s stated that I don’t need a referral for special ists even though my plan is an HMO (though I do have to have a primary care doctor on file with them – in fact, when I first signed up, I didn’t have one, so they randomly assigned me someone, but it was very easy to change).