Everyone should call the Senate right now regarding the AHCA with the ask that there is no coverage loss.

Okay, now that you’re back, let’s see what a rule change will do.

The Silver plans are supposed to be 70% Actuarial Value (AV). AV is the percentage of costs for the pool that the insurer covers. 70% AV means the insurer pays roughly 70% of the costs, and the people in the pool pay roughly 30% in cost sharing. There are lots of different ways to arrange the cost sharing but that is a detail. Under the Obama administration, there was a de minimas variation rule where a plan could be called Silver if it was between 68% and 72% AV. The Trump administration released a new rule that changed the allowed variation to a band from 66% to 72% AV.

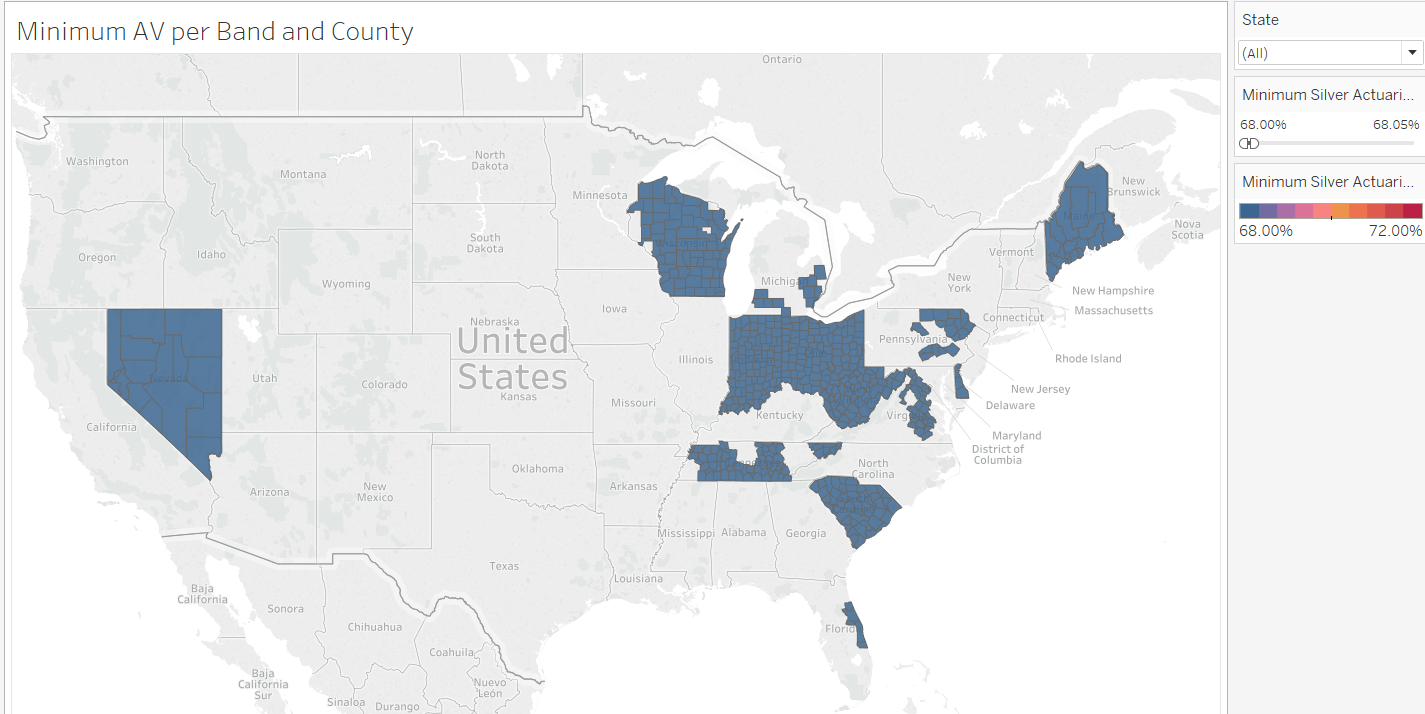

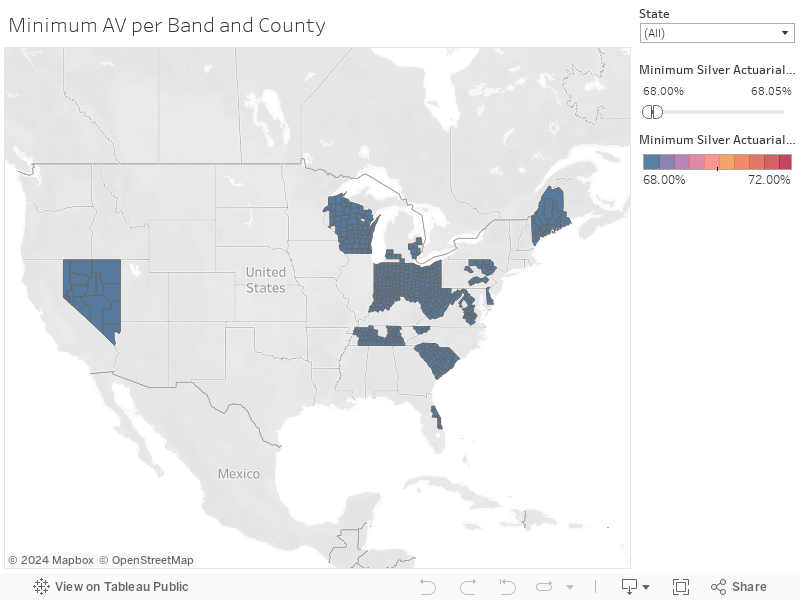

The out of pocket maximums are likely to increase significantly in the highlighted Healthcare.gov counties below:

The highlighted counties have a Silver plan with a 2017 AV between 68% and 68.05%. I figure that companies are more likely to do what they were doing, reaching for the lowest possible AV if the rules are relaxed. Counties where the lowest AV was above 70% are, in my opinion, less likely to see their incumbent carriers race to the bottom as they already had not shown that proclivity. This is most of Oregon and significant chunks of Pennsylvania and Illinois with a few random counties elsewhere.

The distributional consequences are complex. Lower AV values, all else being equal, means lower premiums. The insurers pay less in claims. It is a good deal for the federal government as the premium of the benchmark Silver will either be constant or decrease so advanced premium tax credits will decline. It is a win for healthy people who are not subsidized as they weren’t going to hit the previous, lower out of pocket maximum anyways so they save 3% in premiums. It is a wash for people with Cost Sharing Reduction (CSR) subsidies as the CSR holds constant. It is a wash for subsidized buyers who don’t get CSR but who are healthy and were going to buy Silver anyways. It gets complex for those buyers who wanted to buy another metal band as county specific pricing variations will be altered. Bronze plans will be slightly more expensive and Gold/Platinum plans will be up in the air as to their relative price.

The worst off are the Silver buyers who are not receiving CSR assistance and who are likely to be sick. They are picking up more out of pocket. Non-subsidized buyers will get a slight improvement in lower premiums but all that plus more will go back out the door via higher cost sharing. Subsidized buyers won’t see the slight improvement in premiums. They will only see higher cost sharing.

Finally, the Tableau that I was using to play with this idea is below.

Butch

David, somewhat (probably completely) off topic but I really don’t know where to turn with this question. What’s your advice for someone about to go on Medicare whose spouse is self-employed and so not covered by employer-sponsored health insurance (has been covered under my policy while I work for a large corporation)? Most of the health policies I’ve been able to find are basically just “buying a premium” (high cost and high deductible). Spouse is 9 years younger. We’re in a rural area, where I believe policies are more expensive to begin with. Are there any good options?

Josh

Would be curious how many of those counties are single insurer. Bumping that Min AV filter up to 69% brings almost the entire South and Midwest into play. It seems likely half the country will have a min AV plan in the 66%-67% range, for better or worse.

low-tech cyclist

OK, but what’s the ask? This rule change is either within the discretion granted to the Executive Branch by the ACA, or it’s not. If it’s not, then someone with standing will need to challenge it in court. If it is, then nobody can do anything about it. Either way, the Senate is sidelined here.

Sab

@low-tech cyclist: We need to let them know we are watching, and that we want something more than just lowerror premiums.

David Anderson

@Butch: Best option is to go talk with an insurance agent and then also have a conversation with the Area Agency on Aging. They are the local experts who know this segment 1000x better than me.

Butch

@David Anderson: I did talk with a local insurance agent. Her response was that we’re screwed. I didn’t know there was an Agency on Aging (there may not be in this rural area), but I’ll try that.

Edited to add: the nearest Agency on Aging is about a 6-hour drive away but there is a website, so I’ll try that.

dnfree

I have never heard of a “Tableau” in this sense and it looks like a fascinating tool for someone who knows how to use it. Thank you again for keeping us both updated and motivated.

Kelly

Comforting to see Oregon may be one of the better places if Trumpcare passes. In my county I have 5 companies to chose from. The details escape me but the state took action to encourage companies to go into counties with only one insurer before the most recent enrollment period.

David Anderson

@dnfree: I love Tableau. It is my first piece of a bullshit check on anything and everything.