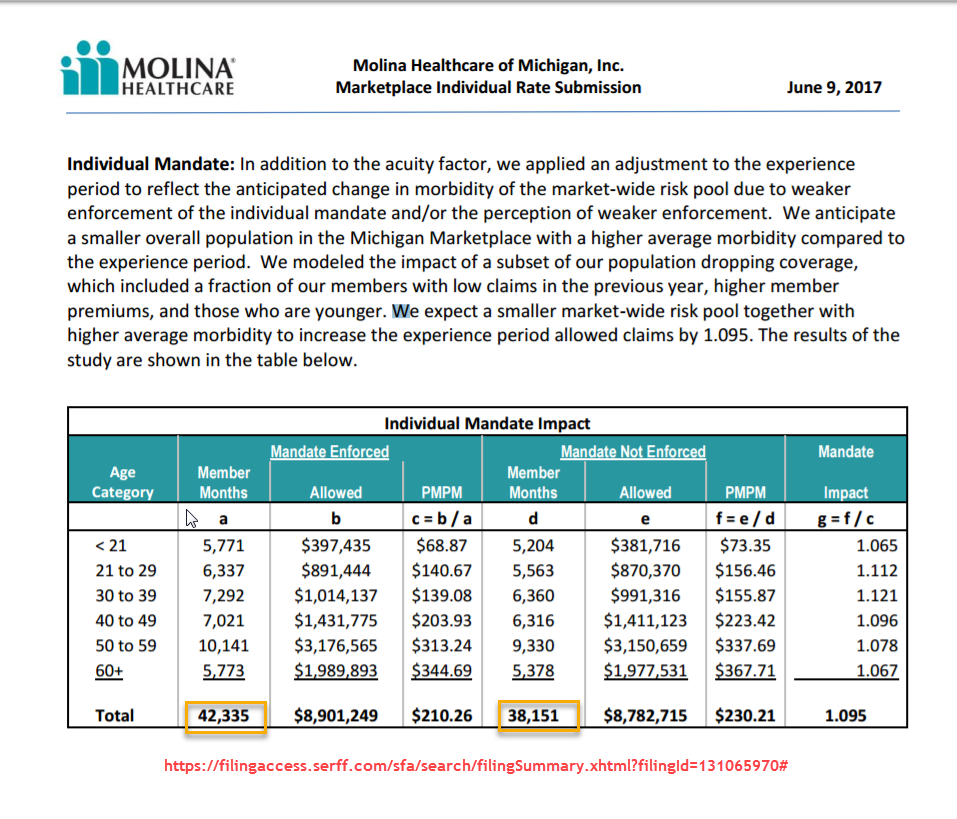

Molina has filed their initial rate increase request for the Exchange in Michigan. I want to highlight a single table that shows a critical fact. Sticky members are sick members. The first people to leave an insurance product and the last people to sign up for it are people who don’t use many medical services or file many claims. I am only using Molina because they wrote a very clear and easy to use actuarial memo. The logic applies anywhere and everywhere.

They are modeling two different scenarios. The first is the baseline scenario where the individual mandate is either enforced or more importantly, believed to be enforced. The second is a model where the individual mandate is believed to not be enforced. The first scenario had higher enrollment and a lower per member per month (PMPM) in allowable claims .

Enrollment drops by almost 10%. Claims drop by 1.5%. Premiums for the remaining people in the pool increase by 9.5%.

Molina is projecting that the people that they are expecting to lose are the people who either don’t file any claims during a year or file the very inexpensive primary care, preventative well visit and generic drug claims. The people who leave have a PMPM of $28.33. That is almost no healthcare utilization.

Insurance relies on people who make very few if any claims to pay into the pool to cover the costs of the few large incurred claims. The pool is getting sicker and more expensive. It can’t death spiral due to the subsidy design but it can and will get ugly for the off-Exchange and non-subsidized markets. The Federal government will pick up the incremental expense for people who receive subsidies on Exchange. Non-subsidized buyers pay the full hike and the lowest probabilistic expensive people will leave.

Victor Matheson

Wow, it’s almost like people respond to incentives and that there were actual reasons that the ACA was designed the way it was.

There should be a whole field of study where people reseach the allocation of scarce resources, and then we could apply that field’s ideas to healthcare. Maybe MIT could hire some professors in that area to look into this sort of thing.

David Anderson

@Victor Matheson: SHOCKING

Get behind me Economist, get behind me

FDRLincoln

Called Jerry Moran’s office (R-Kansas) about the health care bill.

Staffer said the senator opposes the GOP attempts to keep the bill secret, wants open hearings, opposes the house bill and “anything like it” and wants stronger protections for pre-existing conditions. We’ll see. Moran’s staff always says the right things but then he votes with the hard-right anyway.

Call your Senators, Folks! Don’t let them destroy health care while everyone is distracted about Russia.

MomSense

About to call Collins again. Hoping to get a human being. Wish me luck.

Kitty

Did you see this? The Cleveland Clinic is partnering with Oscar in 5 northeast Ohio counties on the Exchange rhttp://www.cleveland.com/healthfit/index.ssf/2017/06/cleveland_clinic_joint_venture_1.html

David Anderson

@Kitty: I find that interesting in a good way. The most interesting thing to me is that Ohio is seeing two entries/expansions (Centene/Oscar) and one exit (Anthem). If I was merely thinking like an economist, that would seem to me to be a boring and reasonably functional market with localized quirks……

Kitty

@David Anderson: In Cuyahoga county we are lucky to have 3 very good hospital systems, University Hospitals, The Cleveland Clinic, and MetroHealth (the county hospital). There are about 5 insurers on the Exchange, but the Clinic only accepted one (Medical Mutual) and it was the most expensive.

MoxieM

“it can and will get ugly for the off-Exchange and non-subsidized markets.” That’s me! oh, great … at the moment, being in MA, I feel a teensy bit protected, although premiums seem high compared to posters who have posted their comps from other regions. Too young for Medicare, but health + age + health make it very challenging to work full time, hence, no HC benefits. Which is another death spiral of its own.

I compare to daughter who has full German State health care (altho American citizen). Holy cow!

We are not a civilized nation.