Oscar Health Insurance is still an enigma to me. I don’t understand their business model. They released their financials a couple of weeks ago and this is the first time I’ve been able to block out enough time to think through them. I am just using their New York state financials as that is their most mature market with most of their membership.

The first take-away is that they are still losing a boat load of money. Everything else flows through there. So let’s look at it below the fold.

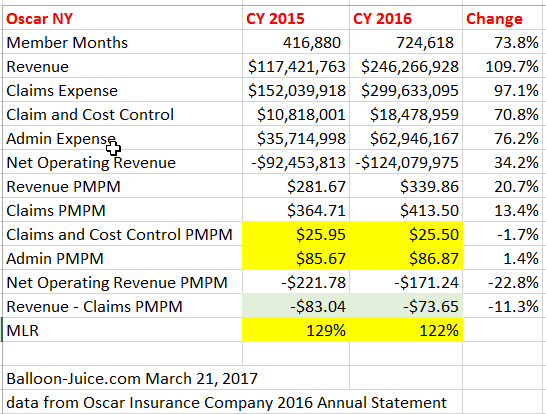

Enrollment is up and revenue is up. Revenue increased faster than the cost drivers on both an absolute and per member per month (PMPM) basis. That is the good news. There is a lot of bad news in the financials.

The MLR is still atrocious. On the individual market, the MLR has to be at least 80%. Good insurers that make money will have an MLR between 80% and 90%. Oscar is still significantly above 100%. Their strategy to get the MLR under control is a shift in networks to a low cost narrow network (which is what everyone does anyways so how are they different) and another 20% increase in premiums will probably get the MLR to 100% assuming no unusual catastrophic events. That is part of the progress towards profitability.

However closing a $73 PMPM gap is a painful process. $70 PMPM total loss was enough to set United Healthcare’s hair on fire. I remember sitting in on long, painful meetings that gave me way too much working as my former employer was trying to get a $5 PMPM change in financial outcomes.

But my issue is not the claims expenses as those look to be most solvable. It is the back end administrative costs. The PMPM has not moved at all. Efficient firms don’t have an administrative (general and claims payment/cost control) ratio of 35% of revenue nor do they have a total admin/claims PMPM north of $110. Admin should benefit from scale. Medical directors, marketing strategists, app developers all either don’t need to scale or scale very slowly with membership. Customer service reps, care management team members and billing clerks scale roughly proportional to membership. All else being equal, we should have expected the general admin PMPM to go down.

Efficient insurers would have seen their admin, claims and cost control expenses converge to $30 to $40 PMPM given the current revenue base of Oscar. The counter-argument is that Oscar is still in a build-out phase and they are building up their claims system, they are building out their investments and while they have to expense those costs as operating costs, they are really capital costs where initial expenses should lead to massive future year savings and efficiencies. I could see that argument with a squint but that is a lot of PMPM to cut through either massive growth as the slow to scale functions stay constant as the denominator increases or lots of lay-offs or pay-cuts or getting rid of the consultants to move work in-house happens.

One of the interesting to me shifts is the composition of their member market. They are going towards a mostly off-Exchange model where subsidies are not available and people are not as price sensitive. This could be a viable model where customer service matters more than price and feeling hip and cool and rebellious against staid insurance companies could be a selling point. But this is a limited area of hope for Oscar as they have also indicated that they want to go into the small group market. Unless they can get their administrative expenses under control, they are just another narrow network product with presumably good customer service and very high premiums. That is a tough sell.

I really still can not figure out what Oscar is doing. In a market where they have had enough time to get over the start-up hump, they are still losing boatloads of money on both claims expenses while also having high administrative costs I don’t think the AHCA will save them. It will help them a bit as the age based subsidies for young adults helps their current target market of off-Exchange/non-subsidized younger buyers. But their admin costs are still out of control and their expenses are still significant.

Ian G.

Yeah, as someone working in the health insurance business in New York, I’ve been waiting for the moment when it becomes clear that hip advertising isn’t enough for Oscar to revolutionize this business. And for the record, my company considers an MLR above 90% on any product to be a serious problem requiring action to get the number down.

Another Scott

Are they working on self-driving cars, too? ;-p

Someone is making money there. I don’t imagine things will change very much until the people with the power there stop making money (VC capital dries up, whatever). I know nothing about Oscar, and find your reporting on them to be interesting. But we’ve seen lots of examples like this in lots of industries (tulip bulbs, electricity, web stores, etc.). Companies implode when people get tired of it being a money pit. One just doesn’t want to be there when the avalanche starts…

Thanks.

Cheers,

Scott.

Fester Addams

As a Trump-connected business, losing money is normal. The first question would be who’s money is it losing to who.

Jerry

@Another Scott:

My god, look at those admin costs!

PaulW

remember that episode of WKRP where Johnny figures out Mama Carlson ran the radio station to lose money in order to balance her overall books?

either that or this is a front for a massive money laundering operation.

BBA

A business doesn’t need to be profitable or have a coherent business model as long as it can keep raising funds from VC firms. See, e.g., Uber.

NobodySpecial

Russian money laundering?

Amir Khalid

I hesitate to say it, but could it be that you’re overthinking this? Maybe they’re just lousy businesspeople who started out with overoptimistic expectations.

David Anderson

@Amir Khalid: Oh definitely, that is the Occam Razor explanation. An idea that is either bad in and of itself or the execution of it sucks. But I am bird-dogging Oscar for two reasons. First they get way too much positive press for doing (poorly) what other companies do better and profitably. That is where I originally started. Secondly, since the company is Trump-related, it is worth keeping an eye on

Barbara

They grew membership by 74% and their admin costs remained essentially unchanged. The claims and cost control efforts are less scalable than pure admin because they often involve clinicians at a fairly granular level (at least when it comes time to do something about them). What I suspect is lurking in the pure admin category are a bunch of outsourced services priced at a pmpm that is not scalable, or only scalable at higher levels of scale than Oscar is achieving in membership growth. E.g., let’s say they have a deal that $5 pmpm at membership of 250,000, $4.75 at 500,000 and 4.50 at 750,000. They are barely moving the needle on that expense even with impressive growth. Also, start-up insurers do a lot less or even none of their sales in-house and so have incredibly high pmpm sales costs. Most insurers utilize both methods but really good and lean insurers go out of their way to use employees as much as they can. When you do this you reduce that pmpm with virtually every sale you make, while the outsourced sales pmpm doesn’t decline at all.

Barbara

@David Anderson: Some insurers are just built to be sold. If Oscar were to sell itself to a larger company, its admin costs would go down almost immediately. All a buyer would really want are the membership and the technology, and maybe favorable provider contracts. The technology piece of it assumes that Oscar is really doing anything that other insurers aren’t, rather than simply talking about it a lot louder, which is my completely speculative hunch.

David Anderson

@Barbara: On both posts — very good points.

I don’t think Oscar is built to be sold as they don’t have much value. Their provider network until 1/1/17 was expensive as hell and now it is narrow. They don’t have a ton of membership and their technology is not that good compared to what other vendors are offering near-off the shelf.

Agreed that clinical management should be fairly fixed on membership on PMPM basis as it is labor intensive but IF Oscar’s tech is that shit-hot at predicting early cost-effective interventions we should be seeing something here. Claims expense is not just cost control — the physical act of paying a damn claim should definately scale from the combination of more claims through the system and learning by doing/fucking up should have occurred.

I know where my former employer routinely bid ASO contracts, I know what my former employer spent on total admin for Medicaid. Those numbers are small numbers compared to Oscar’s total admin cost.

I’ve been puzzled at how Oscar survives when it actually has to price its product above costs instead of passing out free ice cream. If it came into my previous market, both of the major incumbents would eat Oscar for light snack before they went back to going at each other with hammer and tongs.

hovercraft

@David Anderson:

In what way are they related, sorry if you already explained it?

Major Major Major Major

@David Anderson:

This is basically how I read the Silicon Valley business news, and this company seems to be coming from that mindset.

David Anderson

@hovercraft: A young Kushner is a co-founder

Amir Khalid

@Major Major Major Major:

That was my first thought as well.

Barbara

@David Anderson: Well, I wouldn’t buy it, that’s for sure. Their claims expense is higher than revenue before they spend a dollar for administration. Even the most efficient insurer can’t navigate around that kind of obstruction. And no, I don’t see Oscar doing to insurers what Uber has been able to do to taxi cab operators in a lot of markets (and I believe the book is still open for how long Uber can keep this up).

David Anderson

@Barbara: I can see Oscar doing to insurance what Uber does for rides — transfer VC funding to young urbanites as every ride and every claim is a money loser that they make up for on volume — as for actually making money on operations — that is a much tougher question than just breaking shit and passing out free stuff.

I think in 2017 they have a decent chance of getting their MLR to 100% between a combination of rate increase and lower per service cost at a narrow network that they built for themselves instead of the rental network they had 2014-2016

Barbara

@David Anderson: While Oscar can certainly match Uber in losing money it is unlikely to make a dime’s worth of difference to large insurers, unlike taxi cab operators, which have actually lost a lot of market share in urban areas where Uber operates. How long that can go on — or in how many additional markets — is seriously in doubt. Unlike taxi cab regulators, state insurance commissioners cannot be so easily cowed. I would love to see what kind of representations Oscar makes in its business plans to regulators of all kinds, including Medicare Advantage.

artem1s

So, how long before they have to declare bankruptcy? Will there be government bailout money involved? who gets stuck with all the bills when they do claim bankruptcy? Will there be anything left to sell off to satisfy creditors when they fold? Smells like an Enron book cooking outfit to me. Question is when will the pyramid collapse and who gets stuck holding the hot potato.

Barbara

@artem1s: It’s actually not like that at all. If they were to lose backing of VC investors, the worst case scenario is that a state regulator will declare them insolvent and find a replacement carrier for current enrollees. There are state guaranty funds in every state that are funded by insurance companies that the state will draw on to pay pending claims. This has happened. Oscar isn’t big enough to cause chaos.

Irrrr

Are there any other “start up” insurers that are working? What about Clover, Bright?

Marcelo

I think the business model is really clear and easy to understand. Raise a ton of VC, pay yourself and your friends millions in salary and stock, sell stock when company is at a high, then run company into ground until VC runs out, sell for peanuts, pocket the sale and salary, live off of that for years until the next dumb idea, repeat.

The company doesn’t have to be profitable for the people running the company to make out like bandits. What matters is having an exit strategy.