Bloomberg’s Zachary Tracer has a good review of the impact of Humana leaving the Exchange market with a focus on eastern Tennessee.

At least 40,000 people in the Knoxville area may have no health plans to pick from in the Affordable Care Act’s markets after insurer Humana Inc. opted to pull out from all 11 states where it still sell plans in 2018. Another 39,000 in the state would be forced to find a new insurance company….

Humana chose a strategy that would give healthy individuals comparatively bad deals. So healthy individuals stayed away.

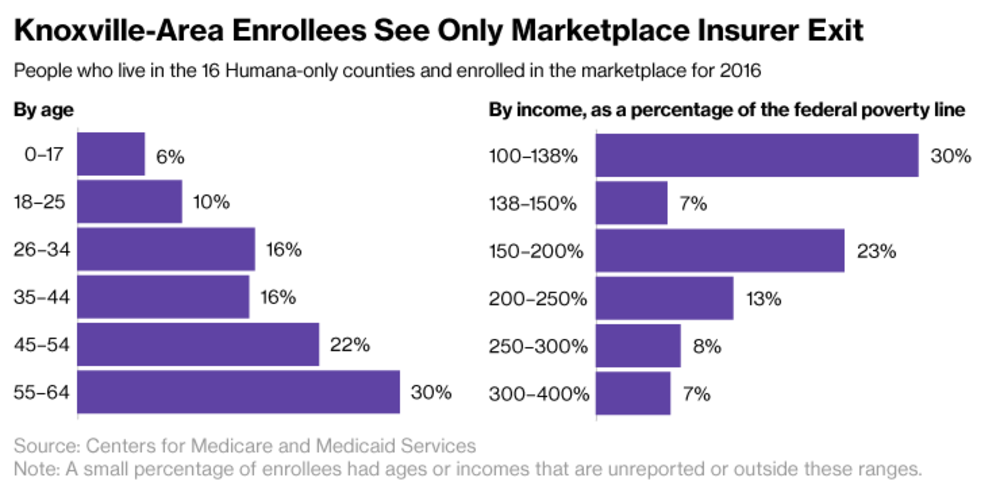

Bloomberg has a great chart on the composition of the risk pool for Humana in the counties where they are the only carrier. It is an old risk pool.

The total risk pool is 32% under the age of 35. The adult (18+) risk pool is 27.5% under the age of 35. Age is a good first pass predictor of health although it is a very rough predictor. In 2016, Healthcare.gov states had 36% (Table 4) of their enrollment be under the age of 35 and 30.5% of their adult enrollment be between 18 and 34.

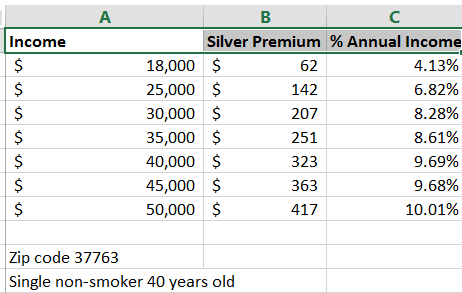

Humana’s strategy was to offer a single Silver plan in these counties. This was the benchmark plan. Anyone who signed up on Healthcare.gov and was eligible for subsidies paid their full personal responsibility contribution. There was no chance for a better deal. In zip code 37763 here are what people at various incomes had to pay for a Silver plan:

Silver plans get expensive very quickly. The Bronze plan for a 40 year old is roughly $90 less expensive but it comes with a $4,800 deductible and a $6,550 out of pocket maximum. What this cost curve means is that quite a few healthy individuals who are not rolling in cash will look at the prices (even after the subsidies) for coverage and take the risk that they will either be okay in 2017 or that they can get some type of coverage some other way if they really need it. This logic does not apply to people who are sick as they know that they need coverage and they will pay the post-subsidy price.

This was a deliberate choice by Humana to engage in a strategy that made them attractive to an older population that is likely to be sicker.

Barbara

When I think generally about the experience of carriers in the ACA, I think most of them made business case assumptions that were influenced by their existing business strengths and customer demographics.

ETA: The way I wrote that was misleading. An exchange carrier needed to achieve an “average” kind of enrollment under the ACA in order to be profitable, given the structure of the exchanges, and that “average” is not necessarily equivalent to the “average” kind of enrollment they are used to dealing with or attracting.

Clem

What strategy should Humana have used to get a younger risk pool? Are their prices as low as they can go?

Sherparick

One has to wonder, especially in the Senate, if there is a lot of lobbying going on by insurance companies with the Senate to maintain the ACA at least as is since many exchanges appear to be transitioning into monopolies and basically licenses to print money with mandatory insurance. They certainly can count on the current administration to be very light on the regulation. It will take a Democratic House, a Democratic Senate, and probably a Democratic President to reform the ACA, to add a public option, and to phase in Medicare from 65 to 55.

Major Major Major Major

Also in Bloomberg, McArdle has an almost illegible piece about this. Guess whose fault the Humana situation is? Hint: it rhymes with ‘schmemocrats’.

David Anderson

@Clem: They should Silver Gap — offer a high price Silver and a lower price Silver either with a different and cheaper network or an AV spread or different cost sharing or a couple combinations of things.

David Anderson

@Sherparick: That is where I’m thinking. It takes an idiot to not be able to be profitable with a quasi-monopoly where the Feds pick up the entire risk of price increases — there are idiots out there but not too many morons.

Weaselone

@David Anderson:

Sounds good. When is Danderson Blue Devil Maycare going to enter the exchange market for Eastern Tennessee?

Elmo

That’s my old zip code. Kingston, Harriman, Rockwood. The demos skew older and white, lower middle class. Go up the road to Oak Ridge, though, and you’ll pull in more families with kids. Oak Ridge has one of the best school systems in the country.

ETA: just a nit, btw: it’s “East Tennessee,” never “Eastern.”

David Anderson

@Weaselone: I’m trying to get out and I don’t want them pulling me back in every time.

Bob Hertz

I cannot agree with your statement on easy profits. In some states all carriers are losing money, and in many states the off exchange market is in a death spiral.

Plus, if we get Paul Ryan’s tax credits, all buyers will be exposed to price increases and then we can have an even wider death spiral.