Two pieces of Exchange information came out yesterday.

First, one of the results of the Trump Executive Order from 1/20/17. The IRS will not reject tax returns that do not contain health insurance mandate compliance activity. Under the Clinton Administration the IRS would have started to have done that for this year for the first time.

Via the San Francisco Chronicle:

In a Feb. 3 meeting with tax-preparation software companies, the IRS said it would not reject silent returns this filing season, according to Andrew Townsend, tax analyst for software maker TaxAct. The decision, which took effect Feb. 6, was not announced publicly and Townsend said he has not seen it in writing.

This is no change from current practice but it is a change from planned practice which would have tightened up mandate enforcement. It is a subtle administrative weakening of the risk pool from the counterfactual of no change.

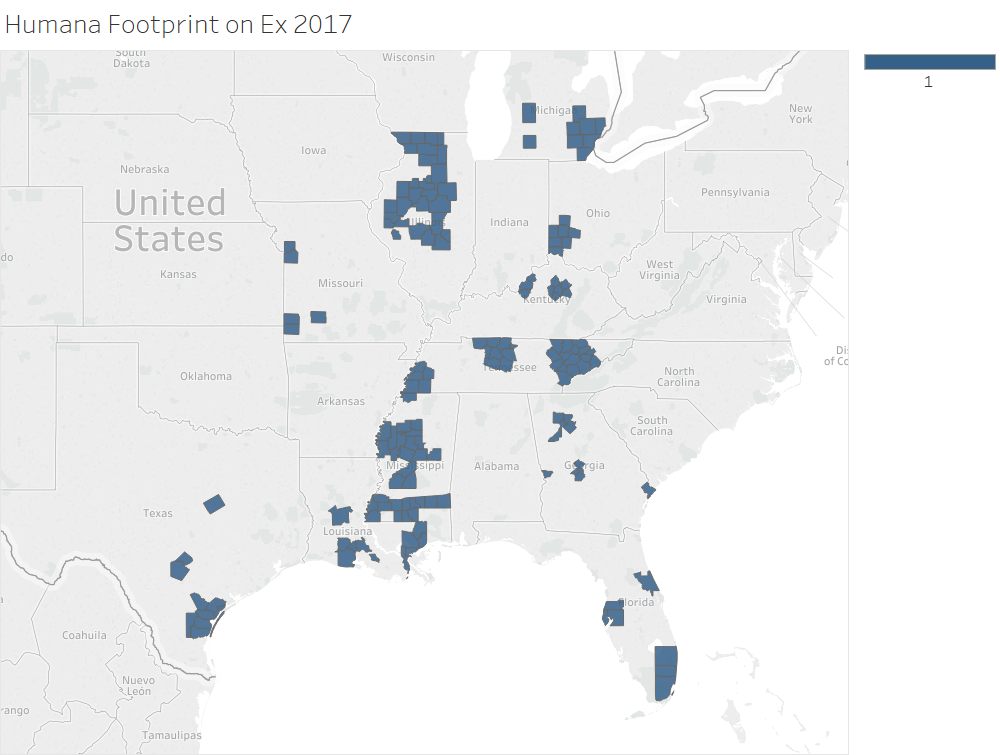

More importantly. Humana pulled off the Exchanges for 2018 last night. Their footprint was fairly small in most states and I was not impressed by their strategy. I was surprised at how early the decision to withdraw was made.

“Based on its initial analysis of data associated with the company’s healthcare exchange membership following the 2017 open enrollment period, Humana is seeing further signs of an unbalanced risk pool,” the insurer said in a statement. “The company has decided that it cannot continue to offer this coverage for 2018.”

The company said it will continue to offer coverage in 11 states through the end of 2017.

In Tennessee, Humana was the sole carrier in a significant chunk of the eastern portion of the state. There they offered a single silver which meant the spread between the benchmark Silver and the least expensive Silver was nothing. This struck me as odd in the fall of 2016. It was their universal strategy. Every county where they participated in 2017, they only offered a single Silver plan. If they are either the sole carrier or the least expensive carrier in a county, their strategy actively chose a small and comparatively sick risk pool.

Yes, there is policy uncertainty and the sabotage of the last week of enrollment which decreased the proportion of young people signed up has made 2017 a much harder year for all on-Exchange insurers but a significant chunk of Humana’s problems were self-inflicted.

As a snarky side note, this is how competetive markets are supposed to work — the ineffective and inefficient leave.

Doofus

They really only had one universal Silver? Is that as insane as it sounds?

David Anderson

@Doofus: Not universal. It had to be locally customized for local networks and local regulations BUT only a single silver offered per county.

So yes, it is fundamentally as insane as it sounds

3Jane Tessier-Ashpool (a/k/a Lorinda Pike)

I’m in one of those little gray bloblets. We only have two choices – moderately decent (Humana; has worked for me so far) and another sort-of “insurance”.

And I was on the phone for 45 minutes last night trying to explain to “Matthew” that as a self-employed person I CANNOT estimate what I will make in 2017, and my 2016 tax returns are the best I can do. I used the phrase “how long is a piece of string?”

The only way to logically estimate 2017 is 2016. He had the totals in front of him, as did I. Didn’t seem to make a damn bit of difference. He wanted a 2017 estimate. We got to a stopping point, and I still have coverage. Higher price, but I expected that. But where do they get these people?

Oh, well. It may soon be a moot point. I guess I can either move somewhere else, or just get sick and die. I’m five years away from Medicare, if it even exists by then.

Kristine

Maybe Humana really thought R’s would be organized enough to kill the ACA immediately, and they could simply revert to business as usual. When that didn’t happen, they pulled out.

It’s funny that companies that claim to be free market really want nothing of the kind. Free market is anything that can be adjusted to kill competition–buying up the competition, patent extensions, paying generics companies not to market their less expensive replacement for your blockbuster–and leave them as a monopoly. When free market conditions actually exist, it isn’t that they don’t want to play as much as they’ve apparently forgotten how.

Skeptigal

So David, what’s the recourse for people in East Tennessee who have lost their only option on the exchange? Does the ACA provide for this possibility? I have employer-provided insurance, but have many friends who were relying on exchange policies from Humana. Do you have any recommendations?

David Anderson

@Skeptigal: Right now, their policy from Humana will be in place until 12/31/17.

Most likely Blue Cross and Blue Shield of Tennessee will move into those counties and Silver Gap them (so your friends who are on a subsidized plan will most likely be better off) in 2018

Skeptigal

@David Anderson: Good news, David, thanks for this, and for all your work here.