One of the major proposals in the draft Center for Medicare and Medicaid Services (CMS) rule that was released on the 15th is to increase the de minimas allowed actuarial value band. Currently the regulation allows a plan to be included in a metal band if it is within two Actuarial Value (AV) points of the target band for normal bands, and within a point in either direction for the targeted Cost Sharing Reduction Silver plans. So that means a standard Silver plan which should be a 70% AV could be anywhere from 68% AV to 72% AV. The proposed modification would allow for a plan to qualify for a band if it was no more than four points below or two points above the target. A Silver plan would be anywhere from 66% AV to 72% AV.

All else being equal, a lower AV means a slightly lower premium. It also means higher out of pocket spending for patients. But all else is seldom equal so things can get messy.

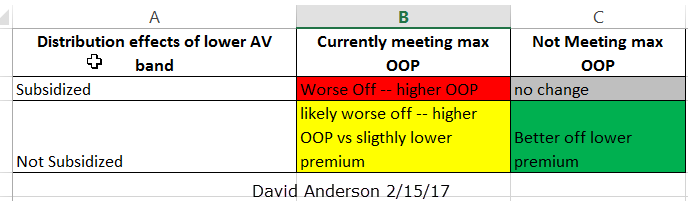

This has significant distributional consequences. And these consequences are not entirely straightforward as the individual market is a complex market. Let’s start looking at the easiest scenarios and then build in complexity. We will need to divide the analytical units into four groups. The vertical split of a 2×2 grid are people who either have met their out of pocket limit or have not incurred sufficient claims to meet their out of pocket limit. The horizontal split is between people who receive premium tax credits that are keyed to the price of the second Silver and people who are not receiving premium tax credits and thus pay the full premium out of pocket.

We will only look at individual beneficiary consequences.

The simplest scenario to analyze is a market that has converged with multiple carriers. Indianopolis, Indiana is a good example. There are two carriers that currently offer Silver plans with 68% AV with similarly narrow networks and very similar pricing. The strategic logic of that situation will have both carriers offer Silver plans that would be near 66% AV as soon as they could.

That produces a nice simple outcome matrix:

Individuals who are receiving subsidies and have significant claims that matched their out of pocket maximum under a 68% AV Silver are indisputably worse off. They will face higher cost sharing. If all cost sharing is from deductibles (an oversimplification), they will go from having a $4,400 deductible to a $4,850 deductible. They do not benefit from lower premiums as the federal government is the risk bearer and reward recipient of lower premiums as the subsidy formula is based on the federal government filling in the gap between the calculated individual contribution as determined by income and the cost of the second least expensive Silver.

Individuals who have not met their out of pocket maximum and are subsidized for a 68% Silver will still not meet their out of pocket maximum and their post-subsidy premium will not change. They are indifferent.

Individuals who are not subsidized and who meet their out of pocket maximum are almost always worse off. They have a small gain in lower premiums (2% drop in AV leads to a 2.4% premium drop on first estimate) but higher cost sharing. There is a small sliver of individuals whose costs above current cost sharing is less than the premium drop. But this is a sliver of people whose total costs are within $100 of the current out of pocket maximum.

The big winners of this change from a beneficiary point of view are individuals who are not subsidized and who are under the out of pocket maximum. They have no incremental cost sharing and they have lower premiums. If the non-subsidized market is extremely price sensitive this will bring in more healthy individuals as prices will fall slightly.

This is the simplest scenario. This intuition should serve people well, but things will get complicated.

There are very few converged markets where multiple carriers have similiar products at similar price points and with similar networks near the second least expensive Silver which sets the subsidy benchmark. The ACA has county level implementation and thus county level stories to analyze. Tennessee has two rich examples to work through. I will be drawing on a post from last November.

The next scenario uses Humana’s Roane County, Tennessee product profile. There they are the sole carrier. They offered a single Silver product which was the benchmark. That plan has an actuarial value that is squarely in the middle of the currently allowed range. If Humana had stayed in the market for 2018 and if they did not radically alter their strategy, there would be no change in distributional impact due to the increased in allowed variance in actuarial value. They would still offer a single plan in this band within the allowed +/-2 AV points.

Across the state of Tennessee in Perry County, Blue Cross and Blue Shield of Tennessee is also the only carrier. They offered two Silver plans. The benchmark plan (14002TN0330214) had an actuarial value level of 71.16%. The less expensive Silver plan (14002TN0330214) has an actuarial value of 68.02%. These two plans have a significant price spread. For a single 40 year old non smoker, the less expensive plan is $97.62 cheaper. This means the subsidized individual in Perry County can access a low cost Silver plan at an extreme discount.

BCBC-TN engaged in a Silver Gap strategy where they decided to use the allowed AV spread and benefit design tweaks to maximize the spread in their pricing between the least expensive Silver and the subsidy setting benchmark Silver plan. This strategy will produce a risk pool that is healthier and younger as the post-premium price for basic qualified coverage is very low.

If this is a deliberate strategy that has rewarded BCBS with a profitable risk pool in Central Tennessee, the logical reaction of BCBS-TN is to continue to maximize the spread. They would keep the high cost Silver at 71.16% AV or attempt to increase its AV to 72% AV with the attendant premium and benchmark increase while modifying the single low cost Silver to be just barely compliant at 66.01% AV. This will increase the spread between the two plans to over $100. It will improve the risk pool.

If there is aggressive Silver Gapping then the matrix changes. Subsidized individuals who have not met their deductible are better off as they will have lower post-subsidy premiums if they choose the 66% AV Silver. There is now a slice of subsidized users who have met their out of pocket maximums where the post-subsidy premium drop compensates them for increased cost-sharing. It is much more of a mixed bag but here the wider spread can be aggressively exploited to create a far larger and stable risk pool.

Pittsburgh has one last interesting example. Currently UPMC Health Plan dominates Allegheny County. (Disclaimer, I previously worked for UPMC Health Plan and spent 3,000+ hours building Exchange networks. Everything I’m saying is in public use files) They have the first fifteen least expensive Silver plans with a $66 spread between the least expensive Silver and their 15th most expensive Silver for a single 40 year old. The least expensive Silver and the benchmark Silver are within $5 of each other. They built these fifteen products as one plan type (EPO), three networks (Super Narrow, Narrow, Broad) and five benefit designs. Each network is attached to five benefit designs. Those five benefit designs are all around 71% AV. They spammed the Exchanges to dominate the search engine optimization of Healthcare.gov and HealthSherpa with isomorphs of the same functional plan that is based on the plan type and the network.

Increased AV bands would have no distributional impact on Allegheny County as long as UPMC Silver Spams at high AV. Allegheny County would be analyzed as if they were like Humana. However even as they have a competitor in Highmark, UPMC could adapt a strategy of a low cost, low AV, narrow network Silver Plan and then eliminate a large number of plans in between one of their high cost, broad network, high AV plans in order to maximize the subsidy gap. In that case, the increased flexibility would transform the distributional consequences towards the BCBS-TN model instead of Humana or the perfectly converged market.

Baud

I caught the first half of your radio show. You iz smart.

Calouste

Sorry to go OT, but maybe one of the frontpagers can pick this up (via Daily KOS):

I know there are quite a few people in the Seattle area around, and this looks like an important race.

Website of the candidate, Manka Dhingra

rikyrah

@Baud:

I thought that his smartness was obvious???

Smedley Darlington Prunebanks (Formerly Mumphrey, et al.)

What happened to Richard Mayhew? I don’t see any of his posts here any more. Is he all right?

David Anderson

@Smedley Darlington Prunebanks (Formerly Mumphrey, et al.): He got abducted by aliens and a body double got hired by Duke University and they gave him a new name

— Richard Mayhew was my pseudonym when I was working in the industry so I could question my boss’s boss’s boss’s decision making

SiubhanDuinne

@David Anderson:

I’ve been meaning to say, ever since you unmasked yourself a few weeks ago, that I am wildly impressed that you didn’t go for an anagram of your real name, or use the same initials, or anything that would be on-its-surface obvious. I mean, you probably pulled “Richard” from one of your great-grandfathers’ middle names and “Mayhew” from an aunt-in-law’s maiden surname, but in general you kept things decidedly sub rosa. Well done. If I ever have to go underground, I want you on my team.

David Anderson

@SiubhanDuinne: I stole the name from Neil Gaiman’s book “Neverwhere” as it was lying on my bedside table the night before I started to write here. I thought there was a proper wink towards his Richard Mayhew who was a finance industry analyst who had to go underground to fight a mythical beast and the character/persona I wanted to create.

The biggest challenge of keeping Richard separate from Dave was dealing with press and contacts. I had separate e-mail, Twitter etc and I had to turn down quite a few opportunities as Richard that would have required an in-person unmasking. Until this summer, there were four people excluding immediate family who knew Richard was me. If I truly wanted to shield myself I should never had done Virtually Speaking as my voice is distinctive enough. I figured I had done enough to survive 24 to 36 hours of a determined non-law enforcement doxxing. After that I would be fucked.

As for sub-rosa, my character backstory was that Leslie Knope was a classmate in grad school and we occasionally run into each other over the course of business. And Richard would like her respect even while knowing she would be put off by the slight degree of cynicism. I threw enough of Dave into the background (soccer, wife and kids, Herb Simon as my favorite economist) and some red herrings. “Richard” had become a very formed character with an interesting point of view and presentation style.

Baud

@David Anderson: I’m still waiting for Baud to get a job offer.

efgoldman

@David Anderson: [If you already posted on this and I missed it, I’m sorry]

What immediate impact, if any, will Mango Malignancy’s declaration today that coverage will not be required AND NOT REPORTABLE TO THE IRS have?

As usual, there’s no clarity. This year’s 1095 forms are long since sent out. Millions of people have already filed.

President Bannonazi and Deadbeat Donnie strike again.

David Anderson

@efgoldman: Not much impact.

The IRS had never rejected tax returns for failure to complete that line. The plan was for them to have done so this year. The EO on 1/20/17 as interpreted by the IRS has them maintaining the status quo.

Yarrow

@David Anderson: I liked Richard. Nice guy. When you “outed” yourself here I thought you said you would continue to post as Richard while here. Did I miss a post where you decided to change to using your real name? Or am I misremembering?

In more health insurance-y news. Did you see this by Jennifer Rubin in the WaPo? Reality dawns: Obamacare might be here to stay? Interesting to see it. Final paragraph:

Seems pretty much how it is.

efgoldman

@David Anderson: Thank you.

Amount of subsidy still gets reported on 1095, though. Because we were over-subsidized, I had to pay several hundred dollars instead of getting a refund.

SiubhanDuinne

@David Anderson:

What a fascinating backstory! Thank you.

If you ever decide to quit your day job, you could easily make it as a novelist.

David Anderson

@Yarrow: I had a sudden flurry of external interest where trying to explain to a broader public that Richard Mayhew at the blog which is the #1 search result for “Skull fuck a kitten” is also David Anderson of Duke University was a complication that was not needed. I get more leverage/impact as Dave Anderson. I can be quoted as an acknowledged expert as Dave not as Richard.

David Anderson

@SiubhanDuinne: I can turn out words. I’m good at that (3,000+ words today on health policy in only a 5 hour writing block) but I don’t have a fictional story that I want to tell yet. Tom Levenson has poked and prodded me to write a book a few times over the past three years. I don’t know how to write a book. It is something I should think about a bit more.

SiubhanDuinne

@David Anderson:

You just put your lips together, and blow.

Yarrow

@David Anderson: Thanks for the explanation. I understand why you did it. I was just confused because I thought you had said you were going to stay as Richard and then you changed to David. It makes more sense to post as David given your new gig.

Julian

Thank you for your ever insightful analysis!

I have a question for people eligible for CSR: say you are in a location where the silver plans offered are all 66% AV (but would have been 68% AV without the change in policy) and you are eligible for the 94% CSR. Would the CSR make up for the reduction in the plan AV such that you are indifferent to this change in policy?

David Anderson

@Julian: Yes, CSR AV is still a constant. If you make between 100-150% FPL your CSR Silver High would be 94% AV +/- 1% which is the same it is now. The CSR is not a bump indexed to actual AV but it is a statutorily defined target point with a little bit of fuzz.

Ned

When you will be making this sort of investment, it is best to be sure that yoou are getting

the product qualityy that you’ll be paying for. How to phrchase

premium quality of diamond ring for affordable prices. Twisting, warping or shifting thst could loosen the stones is among the most common damages that

may get lucky and tiffany or prong settings. http://kylerresf570blog.pointblog.net/