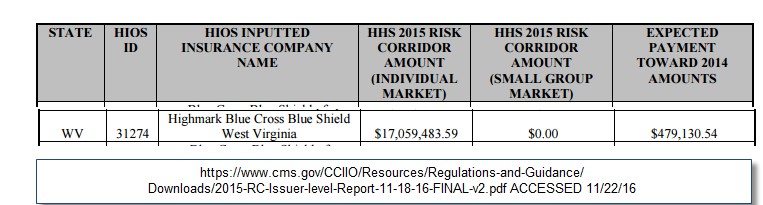

This post is a look at a weakness in the ACA. This particular weakness is mind-numbing stupidity of some carriers. The example is West Virginia and Highmark Blue Cross and Blue Shield’s strategy and results from the 2015 plan year. I am using the recently released 2015 Plan Year Risk Corridor allocations. Companies that have a positive risk corridor balance lost a lot of money on the QHP market. Carriers that are at zero balance either made or lost a little bit of money on the QHP market. Carriers paying into the pool made good money on the market.

I’m picking on Highmark in West Virginia as they are a corner case. They were the only carrier in 2015 in the state. They were the only carrier in 2014 in the state. They should have been able to make money hand over fist. Yet they lost a boatload of money.

Highmark BCBS adapted a Silver Spam strategy in West Virginia in 2014, 2015 and 2016. This means that there was a small spread between the least expensive Silver and the subsidy setting benchmark second least expensive Silver. On a practical matter that meant an individual was not getting a particularly good deal on the least expensive Silver post-subsidy. From a risk pool standpoint, a comparatively expensive lowest cost Silver and fairly high cost Bronze plans means the risk pool will be fairly old and fairly sick.

Highmark was operating as a single, monopolistic carrier for 2014 and 2015 in an environment where the federal government was willing to shovel an amazing amount of money into their hands if they configured their products correctly. A large Silver gap where the spread between the #1 and #2 Silver pricing would have produced a large APTC revenue stream and a significantly healthier, younger and cheaper risk pool was a viable play that could have been done without risking an adverse selection risk dump by other competitors. Highmark had no other competitors, they were absorbing the full risk of the state and could have effectively chosen their own risk pool. And they made decisions that led to a sick and expensive risk pool.

Stupid strategy on the part of the private sector is a weakness of the ACA as it is designed.

Barbara

I am still somewhat stunned that ACA regulators did not learn from what Medicare Advantage regulators figured out some time ago, when they began requiring a “meaningful difference” of at least 20% actuarial value between any two plans to avoid beneficiary confusion and unintended competitive consequences. Even if that seems too draconian given newness of ACA, they could have limited number of plans with comparable actuarial value to two (e.g., wide network/higher deductible versus narrow network/lower deductible).

Richard Mayhew

@Barbara: Welcome to my hobby horse — meaningful difference has been a major weakness of the current regulation as it is too easy to game the subsidy formula and too easy to confuse members.

WereBear

mind-numbing stupidity is the new normal.

Botsplainer

Richard, its dead. The administration will walk away from the Burwell appeal, and that will be all she wrote.

Richard Mayhew

@Botsplainer: 94% Agree with you, but doing a retrospective analysis of what worked and what did not is important. Stupid decision making by profit seeking entities is/was a problem with the ACA

Barbara

@Richard Mayhew: In fairness, MA did not begin imposing meaningful difference regulation until the program had been in existence for four or more years. MA has strong program management people. It helps when Congress cares about the program beneficiaries.

piratedan

@Richard Mayhew: and somehow, that’s OUR fault… we took a free market “model” that a good number of folks “insisted” had to be in place else we would end up gutting an industry (that was earmarking 40% and up of their income to paying their own employees (and especially their CEO’s and Board of directors and shareholders handsomely) to install the equivalent of the outdated VA system (NOT the Medicare system) and have people on the phone handling support issues being the equivalent of death panels.

instead, the medical insurance went the way of the baby bells, each carving out fiefdoms and handling their shops in a way that rewarded foresight and planning (and an actual understanding of the field, which you think they would at least have a tenuous grasp of) and a good number of them decided to sting the tortoise carrying them across the river. Now they get saved by the very same people who let the hookers and blow era reign… cripes, if I was a sociopath, I should have invested my money in health care stock because I fear that it’s going to lead to another era of its predecessor, big ass salaries and dividends for their CEO’s and investors and damn little health care for a fuck-ton of people. Plus, you can forget any kind of salary increases as the rise will suck any of that up and people exploring their own individual entrepreneurship is gone as well because we’ll have to be corporate slaves just to have the minimums covered. Plus Big Pharma gets off clean as does the AMA.

rikyrah

Mayhew, thanks for these posts.

WereBear

@piratedan: It’s an upending of what business is supposed to be: now it’s all about the lying and the looting.

Villago Delenda Est

@WereBear: The MBA mindset triumphs!

J R in WV

I have trouble understanding how BCBS in WV could have modified their risk pool by shaping their Bronze and Silver plans.

As the only provider in the state, won’t their risk pool be everyone not on employer-provided insurance, Medicare, the VA or Medicaid?

And given that WV is a poor rural state with a high level of people eking out their existence on transfer payments (Social Security, or SSI, or pensions) from the federal government, and a high level of people needing advanced health care because of their severely poor health, won’t that be an adverse risk pool under all circumstances?

Plus many of the non-working adults in WV don’t work because they have suffered severe adverse health issues from their work, i e, mining, timbering, oil and gas field workers, construction, etc. and are on disability.

ETA: I’m the first to admit that I do not understand insurance documents, just as I (despite collegiate accounting classes and years of work on accounting software) do not understand IRS documents at all, no matter how long I study the English they are written in.

Hafabee

My wife and I live in WV and are self- and part-time-employed so we have been buying though the exchange since 2014. We get no subsidies (which is fortunate in the sense that our income is good). In 2014-2016 we bought the cheapest bronze plan, which was an HSA-compatible High Deductible Health Plan (no copays, we pay all until we meet deductible) so we put the max we could into our HSA. In 2016 Highmark WVBCBS upped the deducible from $3K to $4K (each); the price for us was ~$500 each (late 50s non-smokers). Wife hit the out-of-pocket max of $6450 this year back in March.

For 2017, Highmark completely revamped their model. The cheapest bronze plan is ~$740 (40+% increase) and has $100/$140 GP/specialist copays — pretty damned high! Plus, they split the preferred provider network into Standard/Enhanced/Preferred tiers with different coinsurance rates among the various plans. The *only* HSA-compatible HDHP is a Sliver plan costing ~$950 each. The deductible is a “modest” $2800, but based on my back-of-the-envelope calculations there is a very small window of possibilities where this HDHP is worth an extra $210 each per month. (And isn’t the selling point of the HDHP/HSA concept that the plans are supposed to be cheaper?!)

So we have only ONE provider, with a limited but expensive and confusing set of choices for 2017. I would love to have a public option on the exchange.

Ridge

Highmark just bumped my rates up 40% starting Jan. Speaking to insurance brokers and agents in the state, even they are having trouble finding affordable health ins. One going several yrs without. That has been the one bitch about Obamacare in WV, if you aren’t on Medicare/Medicaid, your rates continually climb.

Sure will be interesting to see how the new Admin addresses those issues.

Ridge

Richard Mayhew

@J R in WV: Here is my logic on the statement of choose your own risk pool.

For any individual who is eligible for subsidies the decision tree is simple.

Decision 1: Buy a subsidized plan or not buy a subsidized plan (if not buy, either pay mandate fee or get an exemption)

Decision #1 is predominately influenced by the after subsidy cost of the available choices.

Decision #2: Contingent on the choice to buy — what plan to buy

this decision is fundamentally a function of expected health outcomes, risk tolerance and post-subsidy premiums.

Both sets of decisions are fundamentally premised on the post-subsidy premium. We can assume that people who know that they are going to be very expensive will buy insurance at community rated and subsidized prices. Analytically they are irrelevant as they are a near constant.

The question on risk pool composition is how many people who are relatively healthy choose to buy. That is a function of low post-subsidy premium prices. If there is no gap, a lot of marginal buyers will stay out of the market. If there is a large gap and the post-subsidy price on Bronzes are under $10 for families of 3 up to $70,000/year or $25 for cost sharing Silvers with $400 deductibles, a lot of healthy marginal buyers will buy in.

Botsplainer

@Richard Mayhew:

I’m too old anymore to care. In February, Ryan will magnanimously keep Medicare for those 55 and older. I turn 55 in April.

Once again, the olds fucked me over.

I’m tired, sick to shit of fighting,

J R in WV

@Richard Mayhew:

So by mis-pricing their plans, they are driving poor health risks into plans that don’t result in WV BCBS getting any good federal subsidies? That’s how a single insurer can beat themselves out of breaking even? Wow, insurance is complex.

They got too greedy in pricing, and forced themselves into not making any money, am I getting that correct now? In simple non-insurance terms?

Richard Mayhew

@J R in WV: Pretty much… they did not think their problem through. No matter what they did, they were always going to get the bad risk/expensive people.

They did not think how to get the good risk so they got very little counterbalancing good risk to balance out their pool.