A friend of the blog passed me the Arizona approved rates for the 2017 Exchange year. They look really odd to me. Not the premiums (#’s are for 40 year single non-smoker with no subsidy), but the plan offering array seems very strange.

I really want to look at two rating areas to pull out the oddness.

The Silver Spam and Silver Gap strategies are fundamentally market segmentation plays exploiting the subsidy attachment formula. Market Segmentation is one of the first Neat Little Tricks taught in business school. Creating slightly different products at slightly different prices allows for higher allocation of transactional surplus to the produce instead of the consumer or society in general. That is why there are 12, 16 and 20 ounce soda bottles of the same brand in the grocery store.

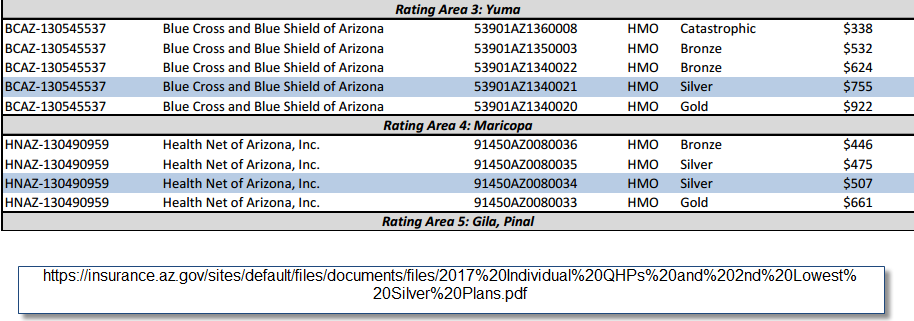

Rating Area 3 has two pieces of oddness leaping out at me. The first is the massive price differential between the catastrophic and the Bronze plans. Bronze has slightly more actuarial value than Catastrophic. The two major differentiators is that Bronze is subsidy eligible while Catastrophic is restricted to under 30 without subsidy. Additionally Catastrophic is a distinct risk adjustment pool. Getting out of the really sick risk pool and only selling to young people leads to a much healthier and cheaper product. That is interesting but not too interesting to me.

In Yuma, the intriguing thing is that Blue Cross and Blue Shield of Arizona is only offering a single Silver plan. Subsidies will be base based on that single plan.

This is really weird and I am professionally puzzled. We know that BCBS-AZ can take a plan type (HMO) and a network and build out two distinct policy offerings. They did that with their Bronze offerings in the same rating area. The big lift in building a plan offering is assembling a network and building the utilization management and plumbing for a restrictive product type like an HMO or an EPO. Adding slightly different cost-sharing components to the base of a network and plan type is dirt cheap. It requires little incremental actuarial work, it requires little incremental system plumbing, it requires little incremental provider outreach. The incremental cost of adding a new cost-sharing arrangement once you’ve done the hard work of building the base plan is low. And you can justifiably offer a tweaked plan at a slightly different price point. And that slightly different price point rejiggers the subsidy attachment point which makes the less expensive Silver plan more affordable post-subsidy. A minor tweak improves the local risk pool incrementally.

Now Maricopa County (Rating Area 4) is not as odd. Health Net of Arizona is doing a moderate Silver Gap. Their less expensive Silver will be $32 less than the second least expensive Silver. For an individual making $18,000 a year, the less expensive Silver is roughly half the post-subsidy price as the benchmark Silver.

The odd, to me, thing about the HNAZ strategy is again segmentation. They’ve shown they can tweak their benefit configuration from a common base to get distinctive price points for their Silver product. I am surprised that they are only offering a single Bronze and a single Gold plan on-Exchange. Adding a few clones would be very low cost and it would allow them to more effectively segment the market.

I don’t know why these decisions were made. They just seem odd to me.

delosgatos

Translation, please. :)

CZanne

Um… this may have changed, but Yuma historically had a relatively low, fixed population (summers used to be 50-75K year round, 300-350K winter) and a significant percent of the fixed population are military, so Tri-care. Does that alter the calculations?

Richard Mayhew

@delosgatos: Offering market segmentation means more hookers and blow for the seller

Richard Mayhew

@CZanne: Shouldn’t matter. Very simple for an insurer once they built the network to offer a $4,000 deductible/25% coinsurance plan AND a $2,000 deductible 60% Coinsurance plan

Steeplejack (phone)

@Richard Mayhew:

Nice joke, but not really helpful for those of us not steeped in marketing-speak. Is it that a group of slightly different products gives the illusion of more choice than there actually is?

Steeplejack (phone)

@Steeplejack (phone):

ETA: and how does that advantage the seller?

Richard Mayhew

@Steeplejack (phone): It is not the illusion of choice.

Let’s go with a simple supply and demand single product market with a single price. People buy if they anticipate that the given price will leave them no worse off then not buying and most likely better off after buying. Sellers will sell when the cost of selling an extra unit is less than the price achieved.

This means (assuming regularly sloping supply and demand curves) that there are some buyers who think they are getting an absolutely amazing bargain as they value what they bought at twice the price they actually paid.

Now let’s allow the seller to introduce a second product that is fundamentally similar to the first product but it has different surface features. The price is different but the underlying cost structure is similar. It will get some people who thought they were getting an absolutely amazing deal to pay more as they are still getting a good deal. some of the consumer surplus transfers to the producer.

The ideal market from a seller’s point of view is a market where every product is uniquely priced to the point just below the buyer’s marginal rage quit/indifference/maximum willingness to pay point (think about how financial aid is used in college ) . At that point every deal that could be made is made but almost all of the surplus from the transaction goes to the seller as the buyers are fundamentally indifferent to the buy/no-buy decision.

Steeplejack (tablet)

@Richard Mayhew:

Okay, thanks. Got it.

AnonPhenom

three things BHO could initiate on his way out the door:

The existing statutory power granted by the Bayh-Dole Act (Pub. L. 96-517) allows the Director of the National Institutes of Health authority to grant new competition for unaffordable, monopoly-priced medications for drugs researched and developed with taxpayer funds in whole or in part. This deters corporations holding federally funded patented drugs from setting unreasonable prices.

Under authority from the Medicare Prescription Drug Improvement and Modernization Act of 2003, the Secretary of Health and Human Services can certify the importation of prescription drugs from other countries under specific qualifications. (This should not be “triangulated” as a bargaining chip to negotiate just certain drug prices down. It should be applied as quickly, as broadly, and as aggressively as possible to bring costs down now)

Federal Trade Commission authority to curb monopolies through prosecution of violations of the ”restraint of trade” prohibition to combat pharmaceutical companies unethical and unlawful practice known as “pay-for-delay”, whereby patent settlements are used by pharmaceutical companies to block generic drug competition for a growing number of branded drugs.

AnonPhenom

because

CZanne

@Richard Mayhew: then, um, ¯\_(ツ)_/¯? It’s also directly on the border, with multiple excellent trans-border service providers on the other side. I’m sure that’s creating an interesting insurance market, too, but not likely contributing to BCBS’s statewide policy of doubling down on bronze and leaving silver in the wind. Per high school classmates still in the area, it’s routine for those outside of the employer insurance market norms (self-employed, gig, contract) to obtain everything except extreme emergency care in Algodones/San Luis at the cash price and just pay the fine (defining extreme emergency as going to die in the next two hours. But broken bones or a hot appendix? Road trip.). I assume that’s true for Pinal, Santa Cruz, Cochise and likely for Graham, Pinal and La Paz counties. I’m not sure on the Northern counties — there’s a patchwork of services from BIAHS on the rezes, a heavy reliance on chiropractic, DIY and herbals in Mormondom, and just ignoring it as viable strategies when the closest doctor – or grocery – is 100 miles away.

Given that BCBS is now a monopoly exchange market in the 13 regions where they’ll be operating, I can’t say I’m surprised to see them skating on the equivalent of an extremely generous Gentleman’s C. My darker experiences with Arizona’s regulatory infrastructure would not permit me to fail to suspect some sort of corruption.

hilzoy

Can’t recall, but there was one county, I think in AZ, that was going to be left without any insurers on the marketplace after its existing insurers decided to pull out. I believe that it was Yuma, and that BC/BS ended up stepping in.