This is a non-ironic tweet from last night:

@bjdickmayhew fun with the AV calculator

— rebeccastob (@rebeccastob) April 14, 2016

I spent some time last night playing the the actuarial value calculator and found a corner case that has significant negative public policy problems and a probable flaw in the CMS model.

This is a hack that companies can use to spam the Exchanges in states with very light regulation. Here is the 2017 AV calculator to check my work.

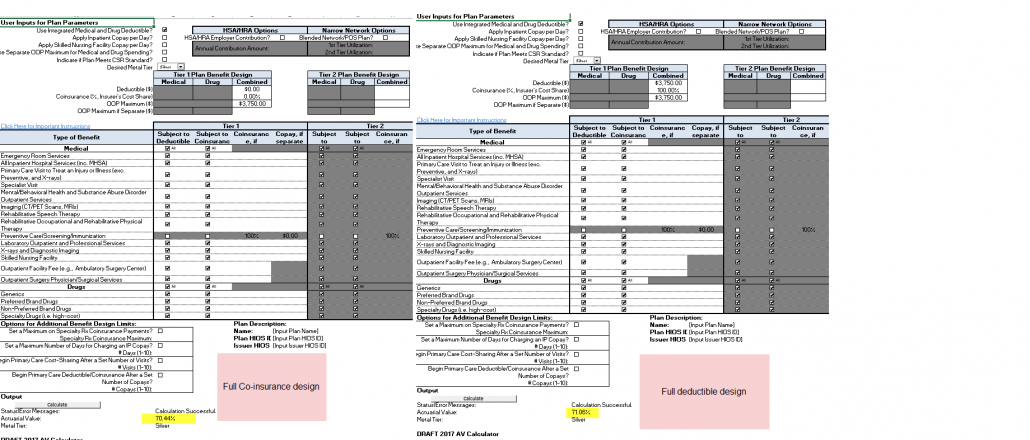

A deductible can be thought of as a first dollar 100% co-insurance where the patient is responsible for all of the contracted rate expenses. It is logically equal and it should be mathematically equal to a 100% co-insurance rate. Logically a deductible of X which is also equal to the same out of pocket maximum is the same thing as a 100% coinsurance rate with an out of pocket maximum of X.

The policy problem is the definition of substantial difference for plan differentiation allows for the addition of a plan design by a company if there is a significant difference in deductible. going from a $3,750 deductible to a $0 deductible qualifies as a significant difference. Companies can submit their first plan with a deductible only cost sharing design and then submit the same exact plan with a 100% coinsurance design to the same out of pocket maximum. For plans that are not the first or second Silver there is no value from the point of view of the company. However if this is done for the plan that is the first Silver, the cloned plan becomes the second Silver at the same price point. It is an illusion of choice.

I believe the 100% co-insurance design would significantly outsell the 100% deductible design because the current set of decision support tools prioritizes low deductible plans. This is an Search exploit as well as a Subsidy exploit.

I believe the 100% co-insurance design would significantly outsell the 100% deductible design because the current set of decision support tools prioritizes low deductible plans. This is an Search exploit as well as a Subsidy exploit.

Ambetter in Chicago actively spammed the Exchanges with functional isomorphs of their Silvers so that cost-sensitive buyers could be fully subsidized on an Ambetter product only and then pay significant incremental premiums to go to any other insurer. However there was at least some gap between the first Silver and the second Silver. This plan design strategy eliminates that gap. The AV calculator allows for this plan design strategy to occur. There is a single “Are you sure” message box to ward against data entry errors on 100% co-insurance but no hard prohibitions.

This hack would not work in all states.

California with their active purchaser model has a very high substantially different standard. A cloned plan design fails that standard miserably. Washington state only allows a maximum 50% co-insurance rate. My state’s regulators have broad discretion to laugh at us and reject one of the two plan designs. However not all states have active or empowered regulators. If the plan design meets model requirements, they will approve anything. This is a special concern for the states that have outsourced all regulatory authority for the individual market to the federal government. Those plans have to meet very minimal standards, and these plans will meet those standards.

Finally on a technical note, I think there is a problem in the AV calculator as the co-insurance design has a lower actuarial value than the full deductible design. In my opinion, the model should produce the same actuarial value with these two inputs.

Baud

Bastards!

Jake Nelson

I always felt allowing the same insurer to count as both the first and second Silver was inherently broken, and could never result in anything BUT shenanigans. I could go on at length about how this should be obvious, but I can probably leave that as an exercise for the reader.

Fix #1: Change that, so the “second Silver” for all purposes is not just plan #2, but “the Silver plan next higher in price than the first that is offered by a different insurer than the first” and insurers are considered “different” only if they do not have half or more of their ownership in common.

Fix #2: Ban deductibles entirely. Not a joke, I think they produce worse outcomes in all cases than an actuarially equivalent plan with a fixed co-insurance percentage from $0 to OOPMax.

Both require having a functional congress that can pass bills, of course.

Richard Mayhew

@Jake Nelson: Jake — #1, I am totally onboard with that.

as for #2 I disagree. Cost sharing has major distributional impacts, and killing deductibles entirely pushes more costs onto the chronically ill and less costs on the healthy.

I have some examples from the 2016 AV calculator as to what is needed to get a Silver plan with deductible only and co-insurance only plans.

Co-insurance plans are better for people with light utilization (paying 50% of the cost of an urgent care visit instead of 100% as it is under my deductible etc) But the money to make up the missing actuarial value has to come from somewhere and that is from the very sick and high cost individuals.

Jake Nelson

@Richard Mayhew: It’s coming from my perspective as chronically low-income in a family with a lot of chronically ill people (cancer, lupus, Alzheimer’s, various military-related issues, etc). I could be called chronically ill myself, probably, but my issues have generally been ones where available treatment is useless (sleep disorders, nonspecific generalized neuropathic pain that only responds to the kind of drugs they’re paranoid/terrified of giving anyone, etc). Until I got on Medicaid, the high-deductible options were basically it, and I never had the money to pay even the lowest end of it, just because it needed too much at once.

Even if you would hit the deductible easily if you got treatment, it too often costs so much you go without any treatment at all until it reaches a breaking point, where you end up spending just enough to almost hit the deductible… when it resets.

Too much of the calculations are based on either the very low end or the high end, and I’ve seen way too much of the territory somehow $1 over arbitrary thresholds where you go from heavily-subsidized to completely on your own.

I recognize much of this experience is pre-ACA (see above, finally have Medicaid), and a bit vague and personal, which doesn’t always line up entirely with a survey of the aggregate data. But it has left me EXTREMELY bitter to the concepts of deductibles, means-testing, and hard thresholds of any kind.

guachi

This entire post is like a master class in the banality of evil.

Jake Nelson

@Jake Nelson: Adding, an issue I have with a lot of research is conflating “people without a current, identified major medical issue”, “people who haven’t seen a doctor recently”, and “healthy people” as a single undifferentiated group of “healthy people”.

In my experience, there is no such thing as “healthy people”, just people who don’t know they’re sick. (Or don’t think anything can be done about it, don’t think they can afford to do anything about it, or are otherwise afraid of what would happen if they tried to do something about it…)

Not pointing that statement at you or anything, Richard, just putting it out there.

guachi

Though if my company did not support legislation allowing such shenanigans, I’d happily design plans all day long to game the system.

Richard Mayhew

@guachi: That is the thing confusing me — I can’t be the only asshole who thought this one through and tested it in the model. The same exploit exists for the 2016 AV calculator. But as far as I know, no one actually has done this yet. It is an obvious exploit and there is some asshole who will do this.

MomSense

There has to be some good Luntz type wording we can find so people will understand that regulation is how we protect people from scams, unsafe products and structures, and so on. Consumer protection doesn’t seem to do the trick.

In Maine after the LeProblem and the Republicans were elected in 2010 they got rid of “job killing regulation” and our Superintendent of the Bureau of Insurance (regulator) resigned. Then they made it possible to purchase insurance across state lines (obvs from states with little regulation). Everyone was shocked, shocked when a disreputable company received premiums but didn’t pay claims.

Even still it is a tough sell when I try to explain to people that regulation is not some nefarious liberal plot to destroy jobs, rather just making sure there are protections in place so ordinary consumers don’t get screwed.

I will say it can be confusing trying to figure out which plans on the exchange are better suited to my particular needs especially when there are so many silvers with similar premium amounts clustered together. This year I consulted with a hooman who answered the phone on the federal exchange and she was a huge help. My prescription cost went up (we are not big users of prescriptions) a bit but I can now access eye exams and other services for three out of four of us without paying it all up front. The fourth is at the age where it is covered 100%.

This same hooman also helped me pick a much better dental plan so hooray big, evil gubmint.

Gladys

I have also used the same SAV calculator. I have been very disappointed with the results too.