The Kaiser Family Foundation has put out a report

NEW: Workers’ out-of-pocket costs increasing faster than costs paid by insurers for job-based #healthinsurance https://t.co/2lIA4UviQi

— Kaiser Family Found (@KaiserFamFound) April 14, 2016

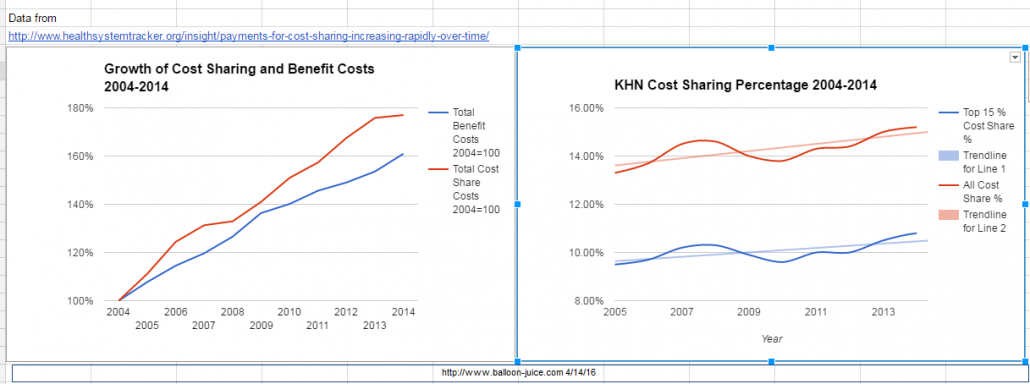

This looks like a crisis as deductibles have more than doubled. However percentages can be funny things, and thankfully the source data was in the report and I could play with it in a spreadsheet:. My big question was why did KHN break things out by type of cost sharing. So I combined cost sharing types and then got total benefit growth and total cost sharing growth using the same data but spliced a bit differently.

This is a different story.

There are two big things. First the cost of the total benefit which is cost-sharing plus what the insurer pays out has increased faster than the economy. Secondly, the actuarial value of used coverage has stayed fairly constant with a slight trend towards a higher proportion of all costs paid for by cost sharing. The red line on the first graph as it increases at a higher slope than the blue line informs the conclusion on the right hand side graph.

From here the problem is not that deductibles are too high because if we hold cost sharing percentages constant but still seeing significant cost growth deductibles versus co-insurance versus co-payments is mostly an allocation and incentive issue. The problem is that cost growth is too high and everything else flows from there. Larry Levitt made the point on the KFF chart that the interesting thing was the switch from quantity variant co-payments to total price variant co-insurance is a big deal as it does change incentives.

There are distributional concerns about cost-sharing choices. I’m probably in the minority in that I think deductibles are preferable than co-insurance and co-pays for a given percentage of cost sharing that must be borne by the entire user pool:

Deductible plans favor the sickest people as the low utilizers pay for almost all of their care via deductible cash. That means the proportion of the pool’s individual responsibility amount is borne by healthy people.

Co-pay only plans favor people who use highly concentrated cost services. A co-pay does not differentiate between a specialist visit with a contract expense of $200 and a specialist visit with a contract expense of $600. It is the same fee. So people who use very costly services but only rarely are best off. People who use a lot of fairly low costs services on a regular basis pay more proportionally.

Co-insurance only plans favor low cost utilizers. They are not paying full price via their deductible, and unlike co-pays, the individual cost per unit matters. Finally, No Use Nora is extremely valuable to the insurance company and the rest of the pool as she is fully cross subsidizing everyone else for this time period no matter how her benefits are built….

The other key insight of this exercise is that the non-covered actuarial value of a plan will get paid somehow by someone. The question is who pays and how much? If the objection to a deductible level is the size of the level, the problem is not the deductible, the problem is the low actuarial value of the plan.

The problem is not the cost sharing choices per se. The problem is medical care costs too damn much per unit of care. Almost everything else derives from that problem.

CONGRATULATIONS!

Maxed out my HSA contribution for the year; good thing I did, had a fairly serious intestinal infection. HSA now all gone. It’s April. Gone from insurance that didn’t cost much and didn’t do much of anything (Kaiser) to insurance that is unaffordable but at least gets things done. I’m still alive so I guess I know what option is the better one but damn, there is no way someone earning median income in this country can make this work.

The Ancient Randonneur

Will outcome based incentives have any effect on unit economics?

Chris

@CONGRATULATIONS!:

Also had intestinal problems for a big chunk of last year; my insurance had a $6,000 deductible because I couldn’t afford the monthly cost of any better plans (heh). I pulled through, but if I hadn’t been living rent-free at my grandmother’s for most of the year, I don’t know what the hell I would’ve done.

ruemara

I’m dealing with that now, having hit a 2k deductible on my plan. But I know I will want some one to look at my knee and other wonky parts so I may swap plans. The costs for everything medical are insane. My ultrasound was $800 for less than 30 minutes. What. The. Fuck.

dr. bloor

I don’t know about you, but I’m not planning to live long enough to see the day when medical costs are knocked down far enough to have no practical significance to the insured. A $3-6K deductible is always going to be a heavy lift for a median income worker bee, particularly when his employer is passing on an increasingly larger chunk of the monthly premiums to him on a year-over-year basis.

At some point, those folks start deferring care, and that ain’t saving anybody money.

Capri

My employer has a high deductible plan they want everyone to join. (One of 3). It’s a $4000 deductible plan, but if you enroll in it they put $1800 in a HSA for you automatically. I’m sure the reason they do this and don’t just push a $2000 deductible plan with no HSA is because a large % of their employees never reach all $1800, and they get a much lower charge for the high deductible plan.

Bill

I’d be happy with a $6,000 deductible, mine currently is $12,000. Basically I have catastrophic loss cover, but even the premium for that is abusively high.

The ACA needs to be fixed to address these issues.

Richard Mayhew

@dr. bloor:

Agreed that a $3000 deductible is a heavy lift much less a $6,600 or $12,000 deductible.

But let’s handwave that $3,000 deductible away and replace its share of the cost-sharing component of the policy with some combination of co-pays and co-insurance. The out of pocket maximum will increase but the total sum paid by the pool of people (assuming no deferred care changes in behavior) and not covered by insurance will be the same.

Switching from deductible to co-pay to co-insurance has distributional consequences BUT the underlying issue is if we have less than 100% actuarial value coverage (which we always will) the non-covered portion has to be paid for by some means.

thebok

As I know from many around me: people are putting off care (or foregoing it entirely) because of high co-pays and high deductibles and that will make the costs higher as people get sicker. At some point the system will implode.

Bill

@Richard Mayhew:

Yes, the question of course is who is bearing the cost but also how and when they are bearing it. In a co-pay scenario, people can often afford – for instance – $50 out of pocket to see the doctor for a sore throat that’s stubbornly hanging on. When faced with a high deductible policy though they look at that same doctor visit as a $300 bill they just can’t afford. In the end this may be bad for everyone, as the high deductible policy incentivises behavior that can lead to more serious problems and overall higher costs for both insureds and insurers.

Lee

Quick(?) question.

During our weekly BBQ & BS session at lunch I was tasked to ask this question in a health insurance related thread:

In our area (DFW suburb) there has been an explosion of new Urgent Care and ER clinics (more ER recently than the other). Is there something in the ACA that triggered this? Is this happening everywhere? It seems to be happening quite a bit around Texas, but around here it is crazy.

Richard Mayhew

@Bill: That $50 co-pay only works to pick up a small chunk of the cost-share % because the deductible is picking up a good proportion of the cost share %.

If there is no deductible either the PCP co-pay goes to $125 OR inpatient co-pays go to $1,000+ per day

gene108

When are the pitchforks and torches coming out for the providers, who are the beneficiaries of runaway medical spending?

*****************************************

Richard, quick question, our company’s insurance plan is coming up for renewal. In the process of doing due diligence, I meet with insurance brokers (or they have their secretary cold-call me to the point, I say “fuck it, I’ll set up a meeting, with your boss (so you’ll stop calling)”.

One I met with yesterday said Obamacare is circling the drain. The reasons he gave are (1) cost sharing is too high for many users, (2) the risk-adjustment payments insurers received will by ending by 2017, thus causing premiums to get jacked up, and (3) insurers are leaving the individual market in droves.

Wondering what your thoughts are on his assessment

gene108

@Bill:

A lot of insurance premium pricing is based on expected behavior based on who pays the first dollar for a service.

Insurance companies model behavior and figure, if you have a low co-pay, people will use services more and the insurance company will be on the hook for the first dollar paid, as the co-pay only covers a small part of the encounter fee.

But in the end getting our health care system fixed comes from getting the provider side of things to be less expensive, which will have its own set of winners and losers.

Richard Mayhew

@gene108: What state?

Overall, that is bullshit, but in some states there may be some truth to it.

1) This is a problem for people making over 200% FPL and can’t afford Gold plans

2)Reinsurance and risk corridors do leave at the end of this year, but risk adjustment is a permanent program. 2b) Subsidies eat most of the risk of premium increases for subsidized indivudals (holding income constant) so for subsidized population NBD. For off-Exchange buyers and ppl above 400% FPL this is an issue.

3) Some insurers are leaving and some are entering

gene108

@Capri:

Last year we had a 15% premium increase because “trend”. The year before we had a 22.5% increase due to some bad claims.

What would you have an employer do, as they are charged more and more for providing healthcare?

Everyone is in a no-win situation, with regards to U.S. healthcare.

gene108

@Richard Mayhew:

I’m in NJ, broker’s out of PA.

That was my reaction. I really wanted to talk to him about the need for single payer and how he should Feel the Bern, but I had another meeting that popped up, I had to go to, so I didn’t have time to sit and chat.

That’s what I meant. Forget what it exactly it’s called. I just think of it as the extra tax we pay for the good of the country.

Bill

@gene108:

This is true. I’m just sick of the cost of our current system so often falling to the people least able to pay.

Bill

@Richard Mayhew:

It can, depending on the plan.

But even the scenario you describe is more palatable, and manageable, for everyday costs than “Don’t bother calling the insurer until you’ve spent ten grand on health costs this year.” Again. Timing matters.

SarahT

@Lee: Same here in NYC. Seems like a new Urgent Care opens in our ‘hood every month. Could understand it if we were in a part of town w/out hospital access, but we’re not. I don’t get it.

kdaug

@dr. bloor:

There’s the rub, Doc. How long can you afford to live?

Ella in New Mexico

In other countries that have “insurance” as part of national healthcare, there are deductibles and co-pays, too.

It’s just that the governments in those countries have laws that regulate insurance and other healthcare businesses in order to protect their citizens from what we refuse to protect our own citizens from. (Although in other countries, I’d argue that it’s not real “insurance” in which you pay a company to take care of you in a disaster and you both bet you’ll never use the insurance for said disaster.)

Was it Hilary or Kay who a while back posted the informative chart comparing the out-of-pocket and premium costs for people living in europe and other modern countries who have a health insurance model of national health care? It showed average out of pocket costs of $250-500 dollars world wide. I thought I had downloaded it but can’t find it anywhere.

Mnemosyne

So here’s a potentially dumb question. Let’s say I have an individual policy that covers only me. PPACA says that I can’t be charged more than $6,000-ish out of pocket every year (it seems to change by $20 or so every year). Does my deductible count towards that OOP cost? In other words, can the insurance company give me an annual deductible that’s more than the PPACA OOP limit?

Mnemosyne

Also, I think we do have a conflict in our system between people who are basically healthy and people with chronic illnesses. Right now, our system is set up with the premise that most people are basically healthy and need to be de-incentivized from overusing healthcare. The problem with that model is that having even a minor chronic condition will blow up into a large expense very quickly.

So how does, say, Switzerland handle people with chronic health issues like diabetes?

Bill

Why is this true? I don’t understand why generally healthy person should be discouraged from seeing a doctor?

Mnemosyne

@Bill:

Basically, I think our system assumes that most people are hypochondriacs who will go to the doctor for fun.

Just Some Fuckhead

@Lee: http://mobile.nytimes.com/comments/2014/07/10/business/race-is-on-to-profit-from-rise-of-urgent-care.html

Lee

@Just Some Fuckhead:

Outstanding article.

Thanks!!

Bill

@Mnemosyne: But we can agree that’s not true, right?

a hip hop artist from Idaho (fka Bella Q)

@Bill: We can agree, but will the system? Probably not.

Brachiator

@Just Some Fuckhead: I wondered about urgent care outfits also. A number have been popping up in Southern California. Thanks for the article.

amygdala

@Bill:

There’s an alarming amount of health care that isn’t clearly helpful and incurs not just the upfront cost of a blood test, scan or whatever that won’t add anything, but the back-end cost, including complications, of the subsequent evaluation.

There’s a good evidence base for some cancer screening, but not all. And then there are the abnormalities picked up on studies ordered for other reasons. A situation I came up against a lot was the incidental thyroid cyst or nodule seen when someone with a proven or suspected stroke got imaging of vessels in the neck. That pretty much obligates blood tests and a thyroid ultrasound, sometimes repeated over months or even years. In years of doing that, never did it turn out to be thyroid cancer. On top of all the cost, there’s a patient understandably stressing out over something else potentially wrong: “Gee, doc, first a stroke, and now something’s wrong with my thyroid?!”

I think we have an inordinate amount of faith in technology in this country, compared to at least some of our peer countries. I also think that American individualism makes broad coverage difficult. I’m always struck, when talking to Canadians and Brits, of not hearing “why should *I* have to pay for someone else’s smoking/eating/drinking/unsafe sex, etc.” The idea that they’re all in it together and my taxes cover my fellow citizens even if I do live to a ripe old age and die quietly in my sleep (God willing) is baked in somehow. It’s not here and some Americans are delusional enough to think that their current excellent health will forever transcend the ravages of time or the idiot who doesn’t look before plowing into an intersection as he or she (or you or I) step off the curb.

Having said all of that, sky-high co-pays discourage people from getting care they need. And as our favorite insurance wonk points out, we need to figure out how to fix that.

Richard Mayhew

@Mnemosyne: Yep, out of pocket max (assume in network) is deductible + coinsurance + copays