@joshschultzdc @larry_levitt @LHPro_Health @insureblog @sangerkatz @LouiseNorris Is there any benefit to “loss leaders” in insurance market?

— Charles Gaba (@charles_gaba) April 2, 2016

It was a bet on churn.

Given certain assumptions, it was not a crazy bet for some insurers to make in the Fall of 2012 when plan architecture for Exchange launch began.

There were a few assumptions that needed to be made for a loss leader penetration pricing strategy to be a viable strategy. The first is the actuaries had a good hold on what the illness profile would look like. The pricing could be under the actuarial fair pricing but there would be no massive negative surprises. This feel for the population needed to be fine grained as it was assumed people who signed up in the first month or two of the initial open enrollment period would have a very different claims profile than people who signed up with nineteen minutes left before the final deadline.

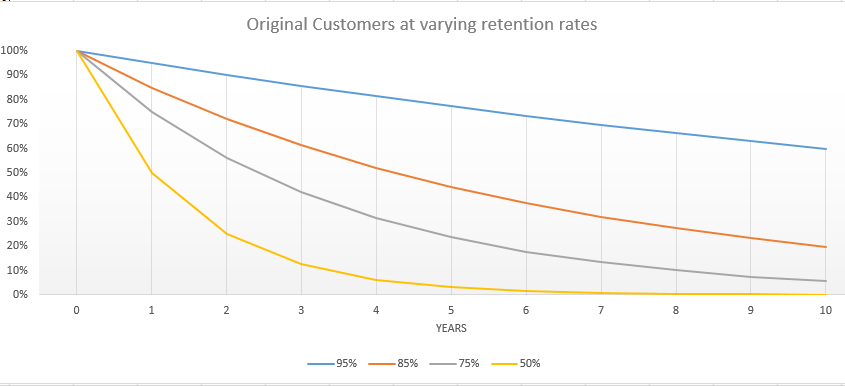

The second major bet was that the membership would be relatively sticky. The pre-PPACA individual market was a high churn market. A typical year would see well over half the individuals on a policy leave the policy. This means two things. First insurers had small windows to collect premiums for any major medical events. Secondly, insurers had fairly shallow data sets. The PPACA subsidy system takes away one of the major drivers of dropping policies because they cost too much. The mandate also makes running naked less attractive. There was a bet that the hassle of switching insurers in Year 2 to save a few bucks a month would not be worth it.

If churn was fairly low, the future year customer acquisition costs would be fairly low even as premiums rise to slightly above actuarially fair levels to make up for the initial losses. Longer average duration of stays would also allow insurers to create big, rich data sets that they could use for risk adjustment revenue maximization as well as pro-active prospective chronic condition management. If the deep data set could allow for earlier interventions on chronic conditions that cost the insurer less than the risk adjustment payment bump for that condition, a sick individual could become a net profit center when their premiums are combined with risk adjustment payments.

These assumptions are highly sensitive to churn.

And they failed miserably. At best the actuaries were not allowed to be right. Products were priced significantly under expected medical expenses.

As @sangerkatz says, insurer finances would be better if they hadn’t set ACA premiums 15% below @USCBO projections. https://t.co/nykW6aVIP8

— Larry Levitt (@larry_levitt) March 31, 2016

More importantly, we are seeing the individual markets to be extremely flexible and not sticky. In 2015, we saw a 15% switch rate plus membership growth:

Roughly a third of all covered lives that had a 2014 policy and wanted a 2015 policy went back on line to look at their options. Half of that population switched. Switchers tend to be healthier on average than non-switchers, so a 15% switch rate from high cost/low value plans to low cost/higher value plans means the plans that lost membership lost a lot of their profit margin. This is market discipline in action.

Furthermore, roughly a quarter of individuals who started 2015 on Exchange did not finish the year with an on-Exchange policy. Attrition is to be expected as the Individual Market has always been a holding tank until something better comes along for a large proportion of the market.

So between switchers and leavers, insurance companies are facing 40% churn and the additional covered lives brings down the average length of membership at a particular company even more.

Betting on stickiness which is the fundamental bet on a loss leadership strategy in order to buy membership and buy good risk adjustment data is not an inherently crazy bet. It is just a bet that failed miserably on the Exchange markets.

japa21

I think part of the reason for lack of stickiness is that people who went on the exchanges already had that experience and found it wasn’t that horrible and did so again. In the past, buying individual policies was much more time and energy consuming, frequently including having to sit through sales pitches.

Another problem was simply that a lot of companies counted on getting money to cover their losses, something that the GOP worked hard to keep from happening. I am cynical enough to believe they did that with the whole purpose of either making companies get out of the exchange market or to make sure premiums went up a great deal, thus making the ACA a failure.

Do you have any figures on Medicare and Medicare Advantage plans on how much churn there is there. It is a different ball game there, I realize. I have to make a decision soon as to whether to go traditional Medicare B and D or do a Medicare Advantage which cost the same, has drug coverage but has more initial out of pocket expenses, though there is a limit, unlike regular Medicare. But with the Advantage plan I can’t do a Medicare supplement package.

My thought is, since I am pretty healthy and have few expenses currently, to go Medicare Advantage now and then reconsider during the open enrollment period later in the year.

PaulWartenberg2016

so how do we fix this?

different-church-lady

I’m not a policy wonk. I know very close to nothing about the mechanics of the insurance industry. I can’t make heads or tails out of most all of this post.

All I know is I get a horrible knot in the pit of my stomach when someone uses a gambling analogy to describe something that’s linked to a thing I am obligated by law to spend a tremendous amount of money on and has a huge impact on my well-being.

Mike J

@PaulWartenberg2016: Fix what? Companies making bad business decisions? Let them lose money.

El Caganer

Well, I’m a net profit center, and damn proud of it.

Richard Mayhew

@Mike J: Yep, bad judgement by insurers is not a systemic policy problem…

Just less hookers and blow for the C-level at the companies that thought the market would be way stickier than it actually was.

O. Felix Culpa

OT, but a medical insurance-related question. My sister called me yesterday in a panic. Her college senior son had an outpatient cyst removal procedure done last week in New Jersey, where he’s studying. My nephew asked and the surgeon said he was in network (United Healthcare), but turns out he’s not. And of course the hospital the surgeon worked in is out of network too. The surgeon said the procedure was “precertified” with the insurance company, but I’m not sure what that means or how it helps with the out of network situation, if at all.

To top it off, my nephew went afterwards to a second surgeon, who said that the cysts were not fully removed. More tests in process. My sister has a high-deductible plan and has paid $4k upfront and is facing at least $22k more in upcoming bills (no idea yet what the final total will be), for a doctor who misrepresented his insurance status AND may not have done the job properly.

What recourse does she have? I suggested, at minimum, that my nephew cancel his $900 follow-up consult with this doctor, since he’d already seen the second surgeon post-op and more tests are forthcoming. Beyond that, any thoughts on how she can address these issues? Many thanks!

Richard Mayhew

@O. Felix Culpa: Get everything in writing ASAP

and call the New Jersey attorney General’s office with documentaiton… follow-up with a conversation with UHC where everything is in writing and all documentation is read to your sister with regard to pre-authorization.

japa21

@O. Felix Culpa: I can’t totally blame the doctor. If he was asked if he is in network for UHC, he was probably honest when he said ye. UHC, like many of the large companies, has many, many plans, and they don’t necessarily include every doc in every plan.

That does not excuse him from finding out more about the policy. Another mistake many people make is they ask “Do you accept this insurance?” The answer is almost always yes, because the provider will accept the insurance even if they are out of network.

As to the precertification, that is based upon medical necessity not coverage. IOW, the person approving the surgery will not base it upon whether or not the surgeon or hospital is in-network. A problem is all the precertification is done between the insurance company and the doctor’s office. The patient will get a letter confirming the certification but it will not mention coverage or if the provider is in-net or not.

And they all have a disclaimer that certification is no guarantee of payment.

Eric U.

it’s really hard for a patient to know that their procedure was really pre-authorized or not. Not sure I would trust a practitioner, I would like to hear it from their billing people.

O. Felix Culpa

@Richard Mayhew: @japa21:

Thanks for your replies! I’ll pass that info on to my sister. To me, it’s inexcusable that the doctor did not confirm whether my nephew was in network under his plan. That is routine with most doctors and specialists I’ve seen, especially given how complicated things are.

ETA: This is the downside of being a relatively healthy family: not knowing the potential pitfalls in dealing with insurance and the medical system. Plus having a 20-year-old out of state managing the process, even though he did his best.

Thus far, UHC has not been helpful in responding to my sister’s questions. Even worse, the rep told my sister yesterday that there’s another $100k bill in the pipeline – not yet posted – which makes no sense for a brief outpatient procedure. We’re hoping that’s a mistake.

? Martin

So, I know the inside story of such an example – CoOpportunity. Their problem was that they underestimated the number of people that would flock to their price point. Some of that was due to WellMark declining to be on the exchanges in the first year. But CoOpportunity, being one of the experimental co-ops was running off a limited amount of federal loans for their reserves, which they blew through in no time at all when they had subscribers an order of magnitude in excess of what they had planned/budgeted. When they returned to HHS for more money – they would have needed more money than HHS had be be appropriated for the entire co-op program. And with no risk corridors, they were pretty much fucked with insufficient reserves, no ability to raise rates (either to grow their reserves or more importantly just to limit the number of policyholders), and no ability to go back to the Feds for a larger loan.

I know that their risk pool was younger and healthier than they had modeled, so that part was good. The pool was just so much larger than they had expected, that they had no way to get through that long period where newly insured members catch up on all of their neglected medical needs before they’ve had time to pay premiums while receiving fewer services in return. Based on the Medicare data I’ve seen (different demographic so likely a very different scale, but it proves the behavior) that takes about 3 years to fully play out.

And that is one particularly tricky aspect of guarantees. We now only recognize two ways to control for demand – highly elastic pricing, like Uber, Priceline, etc. and now Disneyland – and what we increasingly call ‘discrimination’ – arbitrarily deciding to stop providing the service. When you have a guarantee, like the exchange, and you don’t have the ability to quickly adjust rates to control for demand, then you need a quota system or some such. ACA didn’t really want to have those kinds of mechanisms in place, so it really put a lot of burden on the insurers to price the product not just for sustainability but also for population control. Insurance does scale well, but it does not scale quickly.

This is also the problem we have in higher education. Since we cannot use tuition cost to control for the size of our entering class (universities also do not scale quickly – lots of physical infrastructure involved in our current business model) we need to use other measures that increasingly are getting labeled as ‘discrimination’. That’s an accurate term – it’s what we’re doing – we are picking some students who get to come along some criteria and some that don’t along other criteria. Hopefully the criteria are fair, but not everyone will agree on that.