The Federal Trade Commission (FTC) was in the news earlier this week. They, in conjunction with the Commonwealth of Pennsylvania, are filing suit to stop a hospital chain merger in the middle of that state.

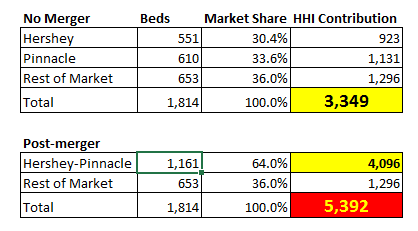

The Federal Trade Commission has authorized an action to block Penn State Hershey Medical Center’s (Hershey) proposed merger with PinnacleHealth System, alleging that the combination of the two health care providers would substantially reduce competition in the area surrounding Harrisburg, Pennsylvania, and lead to reduced quality and higher health care costs for the area’s employers and residents….the merged entity would control approximately 64 percent of this market, likely leading to increased healthcare costs and reduced quality of care for more than 500,000 local residents and patients….Hershey is a 551 bed…Pinnacle is a not-for-profit three hospital system…combined total 610 beds….

1,161 beds is not a huge hospital system. Two hospitals that I can see from the lunch room window have more beds that the four hospitals in question. However the question is not about absolute size, but relative size and market power.

If we use beds in service as a reasonable proxy for market share in the market region, Central Pennsylvania is already a concentrated market. A merger would take a concentrated and minimally competitive market and make it far worse. HHI is a measure of market concentration, a larger number means less competitive (10,000 is pure monopoly).

I am making a worst case assumption that Rest of Market is a single provider, so the HHI Index value is a maximum number, if there are multiple independent hospitals, the HHI will decrease.

The FTC uses the HHI index as a fast guide to their analysis for future actions. Their guidelines are here. The most relevant part is on horizontal mergers paragraph C:

The Agency regards markets in this region to be highly concentrated. Mergers producing an increase in the HHI of less than 50 points, even in highly concentrated markets post-merger, are unlikely to have adverse competitive consequences and ordinarily require no further analysis. Mergers producing an increase in the HHI of more than 50 points in highly concentrated markets post-merger potentially raise significant competitive concerns, depending on the factors set forth in Sections 2-5 of the Guidelines. Where the post-merger HHI exceeds 1800, it will be presumed that mergers producing an increase in the HHI of more than 100 points are likely to create or enhance market power or facilitate its exercise. The presumption may be overcome by a showing that factors set forth in Sections 2-5 of the Guidelines make itunlikely that the merger will create or enhance market power or facilitate its exercise, in light of market concentration and market shares

The FTC’s job is to minimize the accumulation of hookers and blow by market moving entities at the expense of the public. Mergers in already non-competitive markets to make the market is even less competitive are attempts to extract social surplus from the public and transfer it to the merged entity’s primary stakeholders in the form of hookers and blow. Hospitals are already concentrated market movers.

Cutler and Morton in 2014 found the following regarding hospital concentration:

More populous areas are less concentrated on average. Even still, concentration is pervasive. Nearly half (n = 150) of hospital markets in the United States are highly concentrated, another third (n = 98) are moderately concentrated, and the remaining one-sixth (n = 58) are unconcentrated. No hospital markets are considered highly competitive.[my emphasis]

The FTC can be a significant cost control lever. An aggressive FTC that cracks down on almost all hospital mergers as a default response would increase competition. There is some theoretical bipartisan support to aggressive anti-trust merger review and potentially a coalition of wonks that would support actual trust and monopoly busting via the courts. The question is whether or not the FTC in 2017 will have high level political support to engage in default opposition to most insurer and provider mergers in most market segments?

That is the political question. I am not too optimistic about that answer as hospitals and more importantly doctors are some of the most trusted individuals and entities in the American public discourse. A doctor crying on camera that a merger disapproval will not let her treat her patients as well as she wants to is a powerful image that half a dozen policy nerds can’t credibly counter-act. The fate of the Cadillac tax shows the limits of wonk power to change policy when that policy change enrages significant elements of both political parties coalitions. Yet, an aggressive FTC is one of the few “easy” or at least non-legislative routes to containing healthcare costs.

Patricia Kayden

“A doctor crying on camera that a merger disapproval will not let her treat her patients as well as she wants”

Would love to hear the reasoning behind the doctor’s claim since that sounds like an iffy claim in the first place. Plus merging hospitals sounds like a bad idea for the public since less hospitals may mean higher prices/less options for patients.

Good on the FTC for doing its job.

Unsympathetic

Reimbursement for patients hasn’t been “I charge what I want” for decades.. CMS sets the dollar amount for everything [with allowances for regional price changes.. eg, NYC gets more for the same procedure than Hershey] and the only debate is the percentage split between insurer and hospital. Billing is an entirely different discussion.

Hospitals are usually [if not always] the largest employer in a region. Have those hospital employees have been getting raises over the last few years?

This seems to me like the FTC intervened on behalf of the insurer, to keep the insurers getting their percent and stopping PSU from acquiring more power. I don’t know enough about that area to have a thought as to who actually benefits by keeping insurers powerful in Hershey.

But don’t kid yourself into thinking there’s some process by which those “low costs” are going to appear for patients.

Richard Mayhew

@Patricia Kayden: Oh, it is a bullshit claim in most circumstances, but it looks great on TV.

Richard Mayhew

@Unsympathetic: CMS sets fee schedules for Medicare Fee for Service, but hospitals have quite a bit of power to negotiate Medicare Advantage, Commercial, Exchange, CHIP and Medicaid Managed Care rates. Consolidated hospital systems tend to get higher rates than fragmented markets.

So unless your model has case mix adjusted utilization dropping massively in consolidated systems (hint, utilization tends to be indifferent or goes up with consolidation) more money to hospitals means more money paid for premiums.

p.a.

What about inefficiencies thru duplication? Are these proposed mergers ‘paper’ only? Or do they include reductions enhancing efficiency: 2 area MRI units instead of 5, where 5 is considered excessive by whoever is supposed to make those decisions?

mattH

@Unsympathetic:

The ACA at least gave us some degree of control over spending with insurers, which is something we don’t have with hospitals. Allowing greater control of pricing at the point of service will not hold in medical inflation like we’d like.

burnspbesq

Where was the FTC when Catholic and non-Catholic systems were “merging” and ALL the post-merger entities adopted the legacy Catholic systems’ restrictions on what reproductive health services the entities would provide? I’m just as Catholic as the next Catholic, but that was (and is, because it still happens) infuriating and unacceptable.

mclaren

Once again, Richard Mayhew is lying to you. He claims that “an aggressive FTC is one of the few “easy” or at least non-legislative routes to containing healthcare costs.” But the reality turns out to be just the opposite.

The easiest non-legislative route to containing healthcare costs is to leverage economies to scale to reduce medical costs. Let’s take some hypothetical examples: the current electronic record-keeping system in the U.S. health care system is heavily Balkanized, with the different computer systems of various parts of the health care system unable to communicate with one another. This requires massive amounts of data re-entry as hospital records move from one part of the health care system to another — for example, when a patient goes from an imaging lab, to a pathology lab that does blood work, to a general M.D., to a specialist like an oncologist. In each case, data must be reformatted or manually re-entered, which not only drives us costs (due to Baumol’s Cost Disease) but also introduces multiple errors (because human re-keying data tend to make mistakes).

If all hospitals and all imaging labs and all pathology labs and all doctors and all specialists were to use the same software for keeping medical records so that information could be moved around transparently, this would reduce costs. Merging hospitals represents an important step in this process.

Another even more important step in reducing health care costs is to leverage economies of scale in medical procedures. If one hospital could specialize in, say, open heart procedures, while another hospital specialized in, say, dialysis, this would eliminate duplication of effort and cut costs.

But the key to slashing costs by economies of scale involves nationalized single-payer health care.

The larger the hospitals and the imaging labs and the pathology labs, the lower their units costs can go when the government sets fixed prices. Smaller labs and smaller hospitals may not be able to meet the fixed prices mandated by a nationalized single-payer health care system, and they’ll go out of business. That’s good, because it means lower costs overall.

But Richard Mayhew is trying to tell us that the current Balkanized highly fragmented wildly overpriced system is actually good because it increases “competition.” But what we see when we look at the rest of the world’s health care systems is that “competition” is a shitty way to contain health care costs. Instead, nationalized single-payer health care is by far the best way to reduce health care costs. Mayhew is trying to distract us from this reality with the shiny object of “health care competition,” which turns out to be a bogus scam.

P.a. makes this point by raising the quesiton “What about inefficiencies through duplication?”

Don’t ask those kinds of questions, folks — you’ll reveal Mayhew’s con job.

Richard Mayhew

@mclaren: do you have evidence that monopoly providers are a net public good? Especially as single payer needs 218-60-1-5. In 2017 there is no plausible single payer coalition.

Where are your cites?